Authors:

Camilo Contreras – Senior economist – FLAR.

Carlos Giraldo – Chief economist – FLAR.

Iader Giraldo – Principal economic researcher – FLAR.

Viviana Monroy – Deputy director of economics studies – FLAR.

Andrés Valqui – Professional economist – FLAR.

Liz Villegas – Professional economist – FLAR.

As of the second quarter of 2023, figures indicate that the Latin American economy has remained resilient in the face of the postpandemic shocks and the high levels of uncertainty we are witnessing. The results are better than expected a few months ago. Gross domestic product (GDP) growth is falling but remains higher than before the pandemic. Inflation continues to decline in most countries and, on average, it is below 7%.

The balance of payments’ current account deficit is beginning to decline due to lower domestic aggregate demand. According to the performance of their aggregate indicators, financial systems have remained resilient. However, macroeconomic and financial instability risks are present due to external and internal factors. The fiscal deficit is gradually increasing, as are public debt levels.

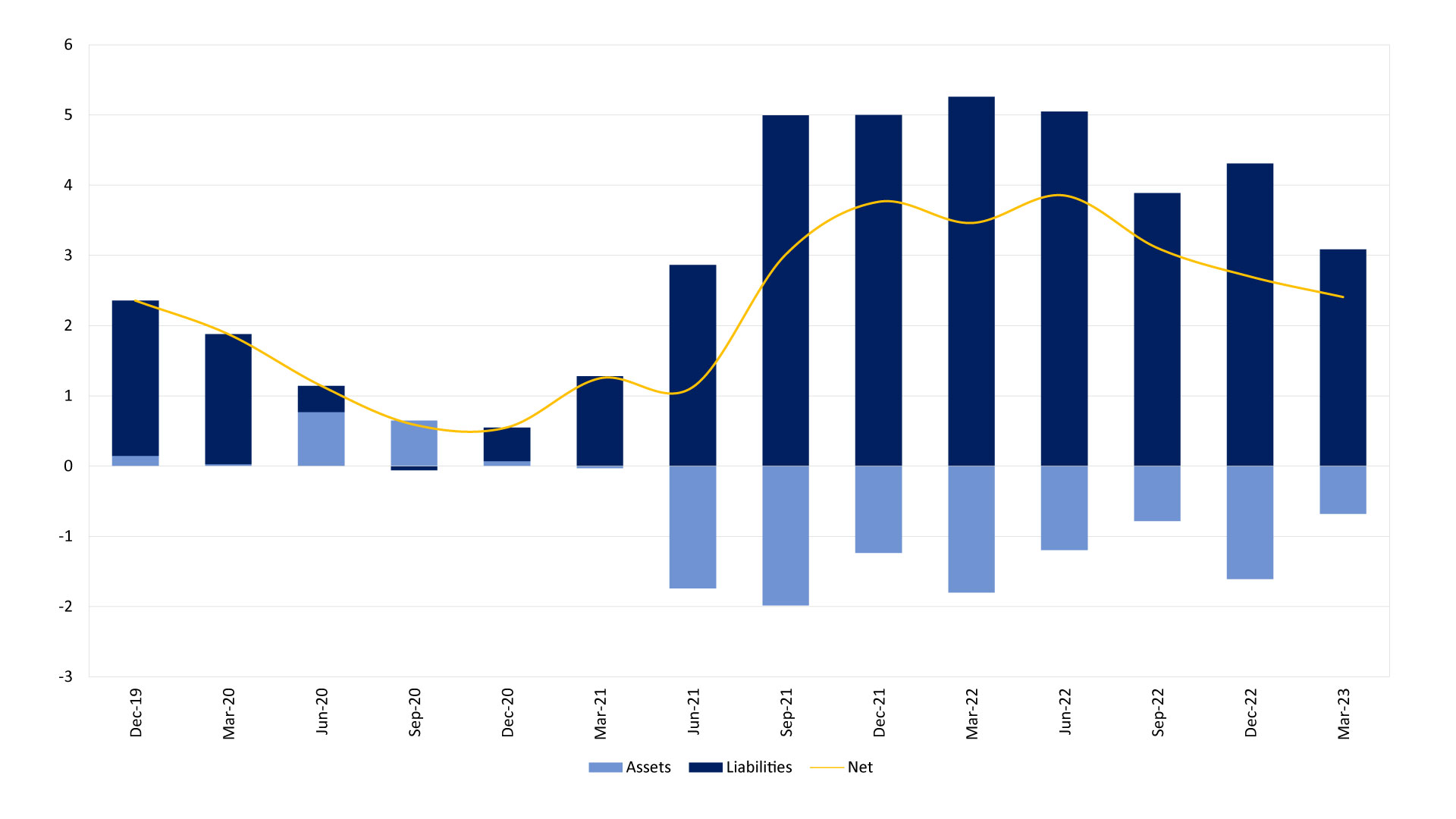

Economic growth in the region has been falling slower than expected, leading to an upward correction of GDP growth projections for 2023 (Figure 1). External savings, mainly foreign direct investment (FDI), have been the region’s largest source of financing growth (Figure 2).

Figure 1: Annual Economic Growth in Latin America (%)

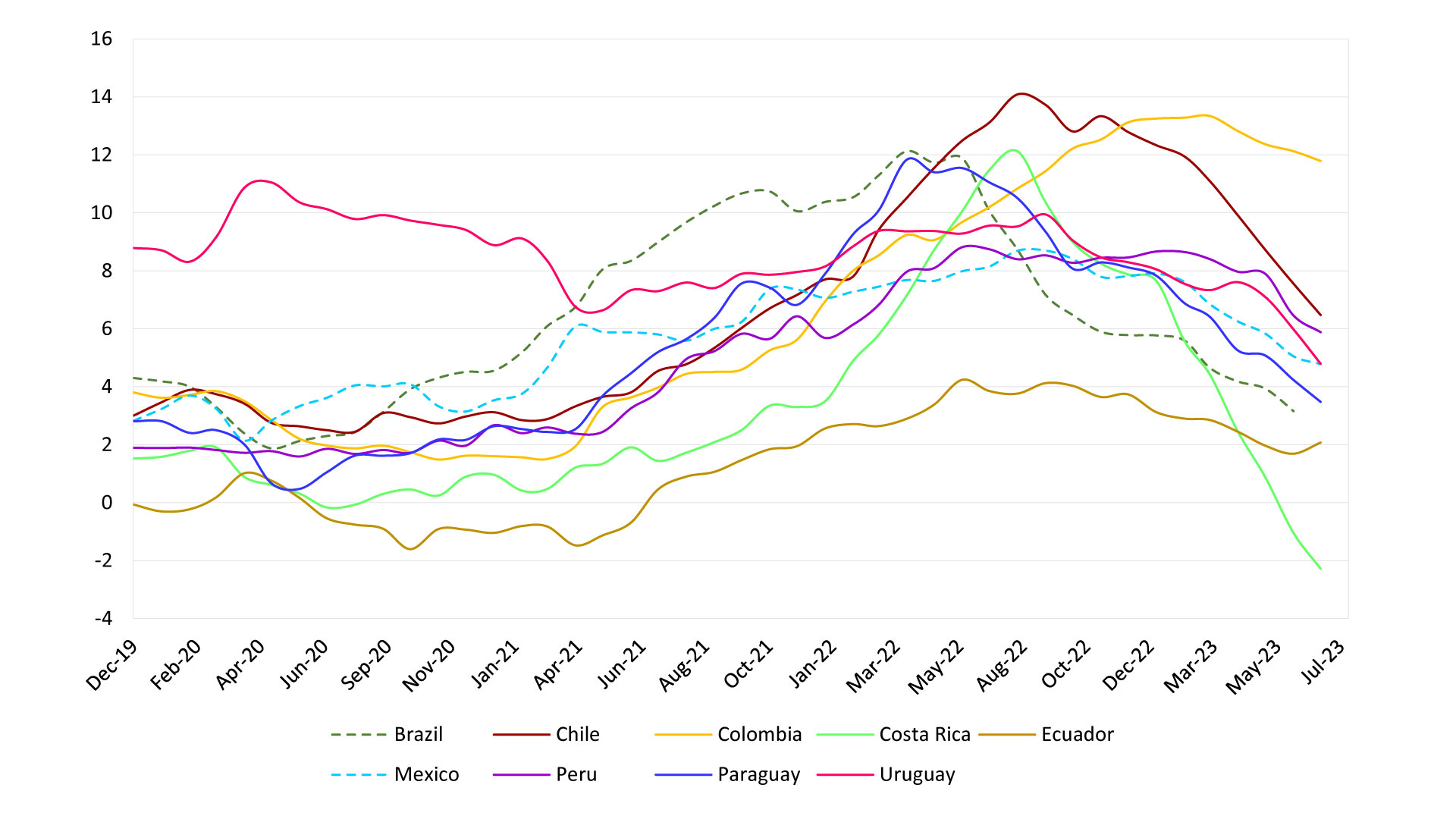

The region’s governments have also met their debt placements in the international sovereign bond markets. The latter is evidence of the greater appetite for the region’s assets, which has been reflected in a lower embig spread for most countries. With this decline, countries such as Chile reached prepandemic levels, and others such as Brazil and Paraguay came closer to this benchmark level after the increase they experienced in 2022.

The deficit in the current account of the region’s balance of payments as a percentage of GDP is beginning to fall, even though the prices of the region’s main export commodities have declined, and the trade balance of Latin American countries has presented heterogeneous behavior in recent quarters.

Figure 2: Decomposition of the financial account for Latin America1/ (% GDP)

Source: Own elaboration based on national sources

1/The sample includes Brazil, Chile, Colombia, Mexico, Peru and Uruguay. Based on PPP.

In connection with the external sector scenario, most of the region’s currencies have appreciated sharply in recent months, while central banks’ international reserves have increased or remained stable.

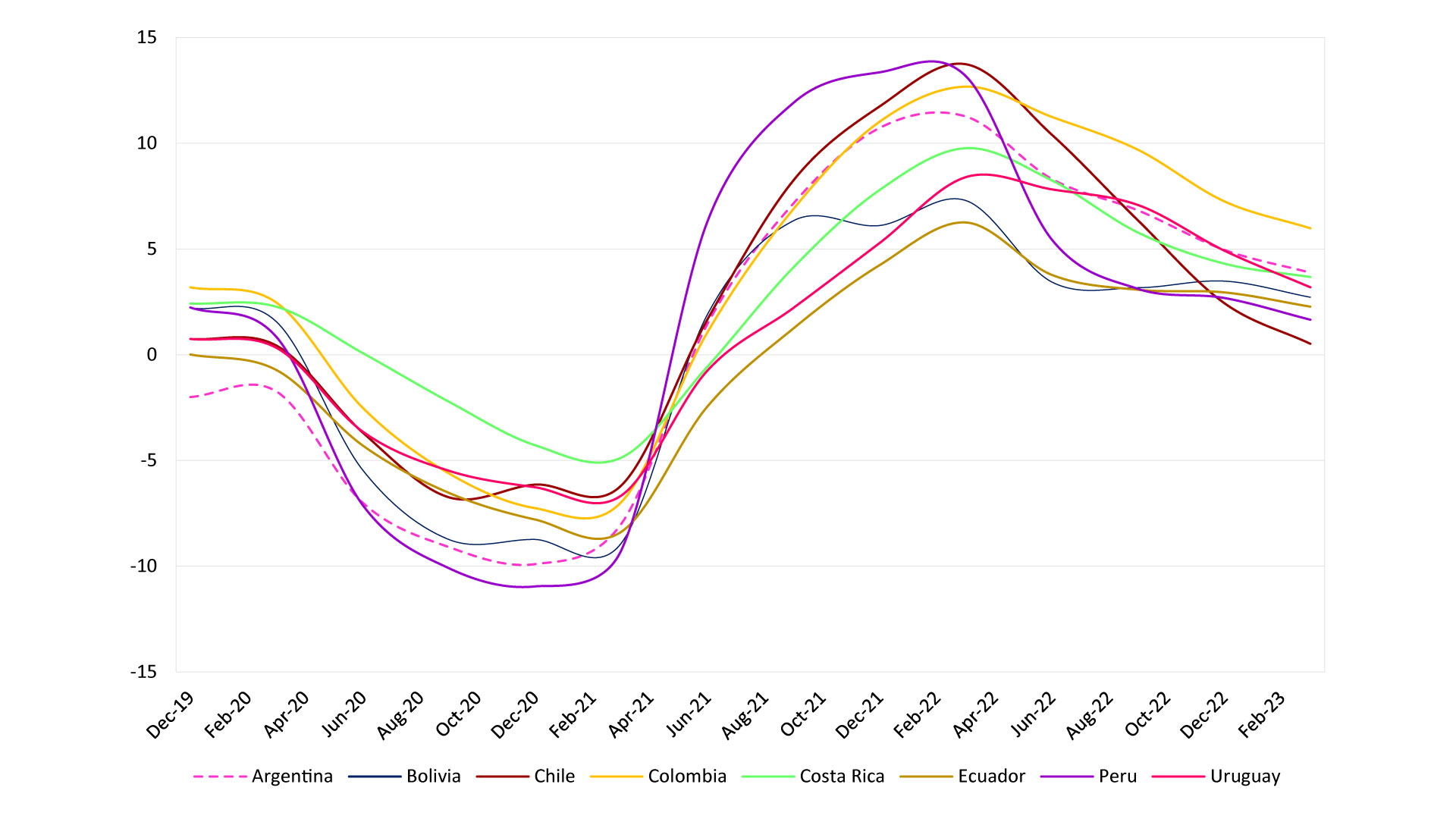

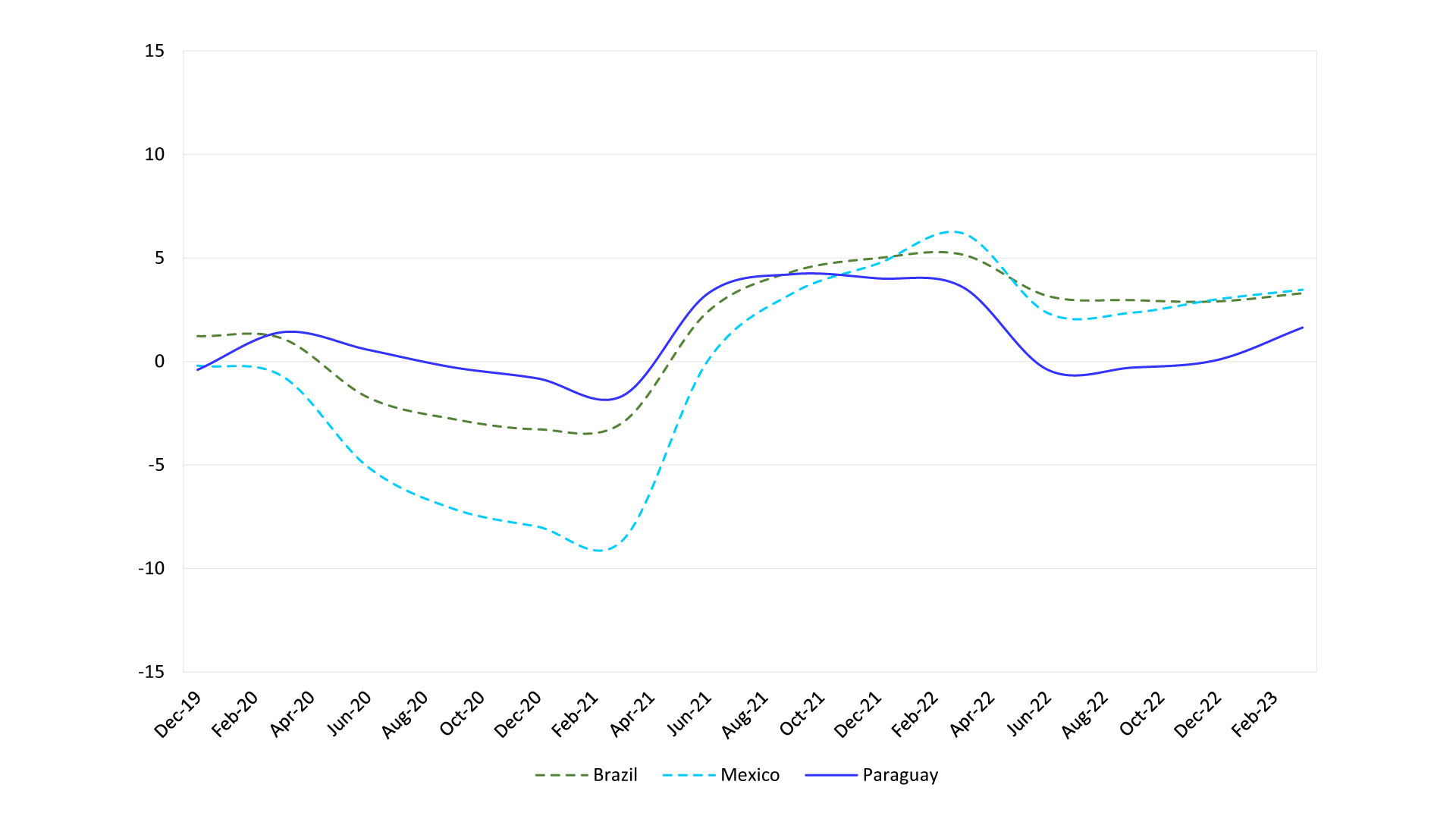

Inflation has been on a downward trend in three-quarters of the countries in the sample; however, it has not yet reached the target levels set by the economic authorities in most countries (Figure 3). Inflation expectations continue to fall, which, together with the slowdown in inflationary pressures, has led most central banks in the region to pause in terms of raising their monetary policy rates and, in some cases, even begin to reduce their monetary policy interest rates from historically high levels.

Figure 3: Consumption inflation Latin America (%)

Source: Own elaboration based on national sources

Financial systems remained resilient despite higher global and local interest rates and falling economic and credit growth in most economies. In most countries, solvency, defaulting, and profitability continued to perform better than the last decade’s average, despite a slight deterioration of certain indicators (for example, defaulting) as recently presented in some countries.

On the fiscal front, the outlook is more challenging; the fiscal deficit is gradually increasing due to factors such as deteriorating revenue collection, strong spending demand for social programs and mitigating the effects of weather-related factors, and higher interest payments on debt. All these phenomena result in an increase in public debt and less fiscal space for most of the countries in the region, which calls for a more significant effort from this perspective to consolidate a sustainable debt trajectory.

To date, the region remains resilient in a context of high global uncertainty, but several external and internal macroeconomic and financial instability risks are present. Among these main risks are lower global demand, a longer than expected prolongation of international interest rates in the event of slow convergence to inflation targets, a disproportionate impact of the El Niño phenomenon on economic activity in several countries, disruptions in public order due to political and social instability, and limited fiscal space that reduces the maneuverability of governments and weakens the sustainability of public debt.

Against this backdrop, the challenges ahead for the different Latin American countries, although heterogeneous, are significant for keeping the region resilient. Coordinating fiscal and monetary policies is essential to achieve price stability, fiscal sustainability, financial stability, and sustained economic growth.