Authors:

Carlos Giraldo, Latin American Reserve Fund. – cgiraldo@flar.net

Iader Giraldo, Latin American Reserve Fund. – igiraldo@flar.net

Jose E. Gomez-Gonzalez, Department of Finance, Information Systems, and Economics, City University of New York – Lehman College – jose.gomezgonzalez@lehman.cuny.edu

Jorge M. Uribe, Faculty of Economics and Business, Universitat Oberta de Catalunya – juribeg@uoc.edu

In our deeply interconnected global financial landscape, the decisions made by central banks wield significant influence that extends far beyond the confines of national borders. Specifically, monetary policy exerts considerable influence over both local and global financial markets, affecting critical factors like interest rates and credit availability. These financial dynamics, in turn, ripple through the broader real economy.

The extensive literature on the bank lending channel and the risk-taking channel of monetary policy has consistently demonstrated banks’ pivotal role and financial characteristics in transmitting the monetary policies of local central banks. However, less attention has been directed towards investigating the existence of an international bank lending channel. This shift in focus has mainly been a response to the rise of global banks. Recent empirical studies have unveiled that globally active U.S. banks serve as active conduits for transmitting monetary policy shocks to other nations. Their strategic responses to these shocks have discernible implications, notably in the distribution of bank claims between the United States and foreign countries.

Limited attention has been devoted to examining how U.S. monetary policy shocks are transmitted to countries where the presence of global U.S. banks is minimal or non-existent. There are compelling reasons to suspect that U.S. monetary policy shocks also exert an influence on bank lending in these cases, particularly when considering small, open, emerging market economies like those In Latin America. To begin, this is because central banks in these countries often react to shifts in U.S. policy interest rates (Huertas, 2022). Consequently, U.S. monetary policy shocks can influence local bank lending channels. Furthermore, alterations in U.S. interest rates impact worldwide capital flows, subsequently influencing exchange rates and asset prices, such as housing prices. These, in turn, have implications for the propensity to engage in borrowing and lending within credit markets.

In our forthcoming paper, we investigate the propagation of U.S. monetary policy shocks to bank lending within five of the largest Latin American nations (Brazil, Chile, Colombia, Mexico, and Peru). Notably, the presence of large international banks, particularly those from the United States, is limited in these five countries. That is, their financial systems are primarily comprised of domestic banks. We utilize annual balance sheet data encompassing all banks operating in these five countries, spanning from 2000 to 2021. We utilize the recently developed measure of U.S. monetary policy shocks introduced by Bu et al. (2021).

Table 1 presents descriptive statistics of the bank-specific variables utilized in this study. It is evident that the average annual growth rate of gross loans in the five countries is notably robust, consistently exceeding 10% across the board. Furthermore, substantial disparities are observable, with Mexican banks exhibiting a gross loan growth rate more than double that of their Colombian counterparts. The control variables display significant heterogeneity as well. On average, Chilean banks appear larger but less solvent compared to their counterparts in other countries. Conversely, Colombian banks exhibit notably lower liquidity levels compared to their peers in the dataset.

Table 1. Descriptive Statistics of Bank-Specific Variables by Country 2000-2020

| Variable | Mean | Standard Deviation | Minimum | Maximum |

| Brazil | ||||

| LoanGrowth | 17.37% | 87.28% | -98.29% | 1802.78% |

| Solvency | 13.79% | 13.87% | 0.16% | 96.68% |

| Liquidity | 70.25% | 564.74% | 0.02% | 11456.13% |

| Size | 8.84 | 1.86 | 5.03 | 13.24 |

| Chile | ||||

| LoanGrowth | 20.72% | 94.52% | -40.39% | 1325.07% |

| Solvency | 9.29% | 5.06% | 3.8% | 47.3% |

| Liquidity | 38.18% | 25.07% | 6.36% | 173.02% |

| Size | 9.24 | 1.39 | 5.24 | 11.43 |

| Colombia | ||||

| LoanGrowth | 10.40% | 23.82% | -47.45% | 195.27% |

| Solvency | 12.42% | 5.27% | 5.70% | 46.91% |

| Liquidity | 27.51% | 13.35% | 0.27% | 93.04% |

| Size | 8.12 | 1.73 | 3.93 | 11.22 |

| Mexico | ||||

| LoanGrowth | 28.38% | 242.70% | -40.39% | 4382.30% |

| Solvency | 14.97% | 13.69% | 1.14% | 98.30% |

| Liquidity | 971.13% | 10225.82% | -24.33% | 172197.60% |

| Size | 8.43 | 1.95 | 2.19 | 11.86 |

| Peru | ||||

| LoanGrowth | 16.51% | 58.50% | -42.56 | 979.83 |

| Solvency | 14.83% | 10.04% | 2.11% | 100% |

| Liquidity | 168.08% | 730.93% | 2.39% | 8795.45% |

| Size | 7.49 | 1.72 | 2.16 | 11.09 |

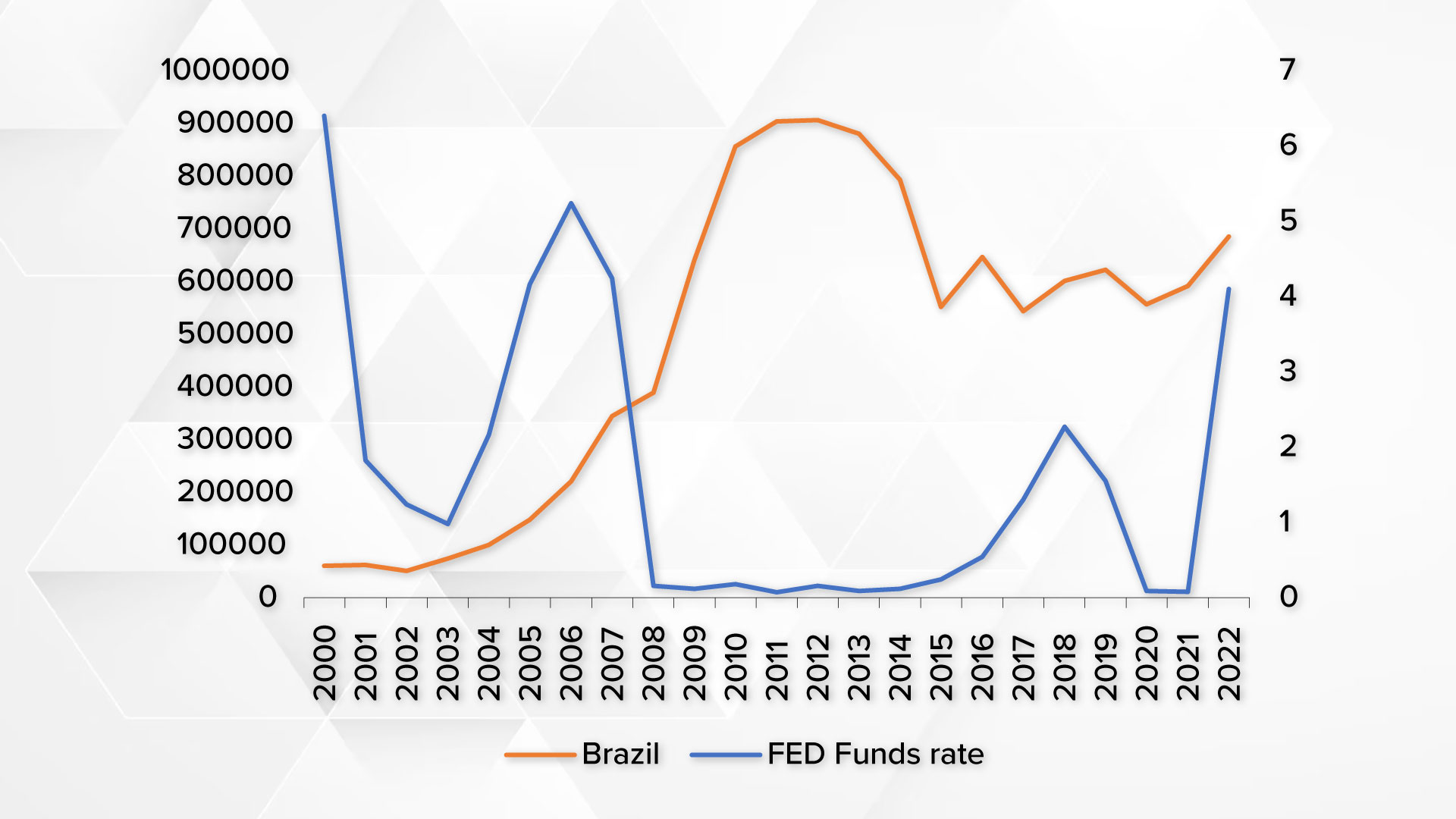

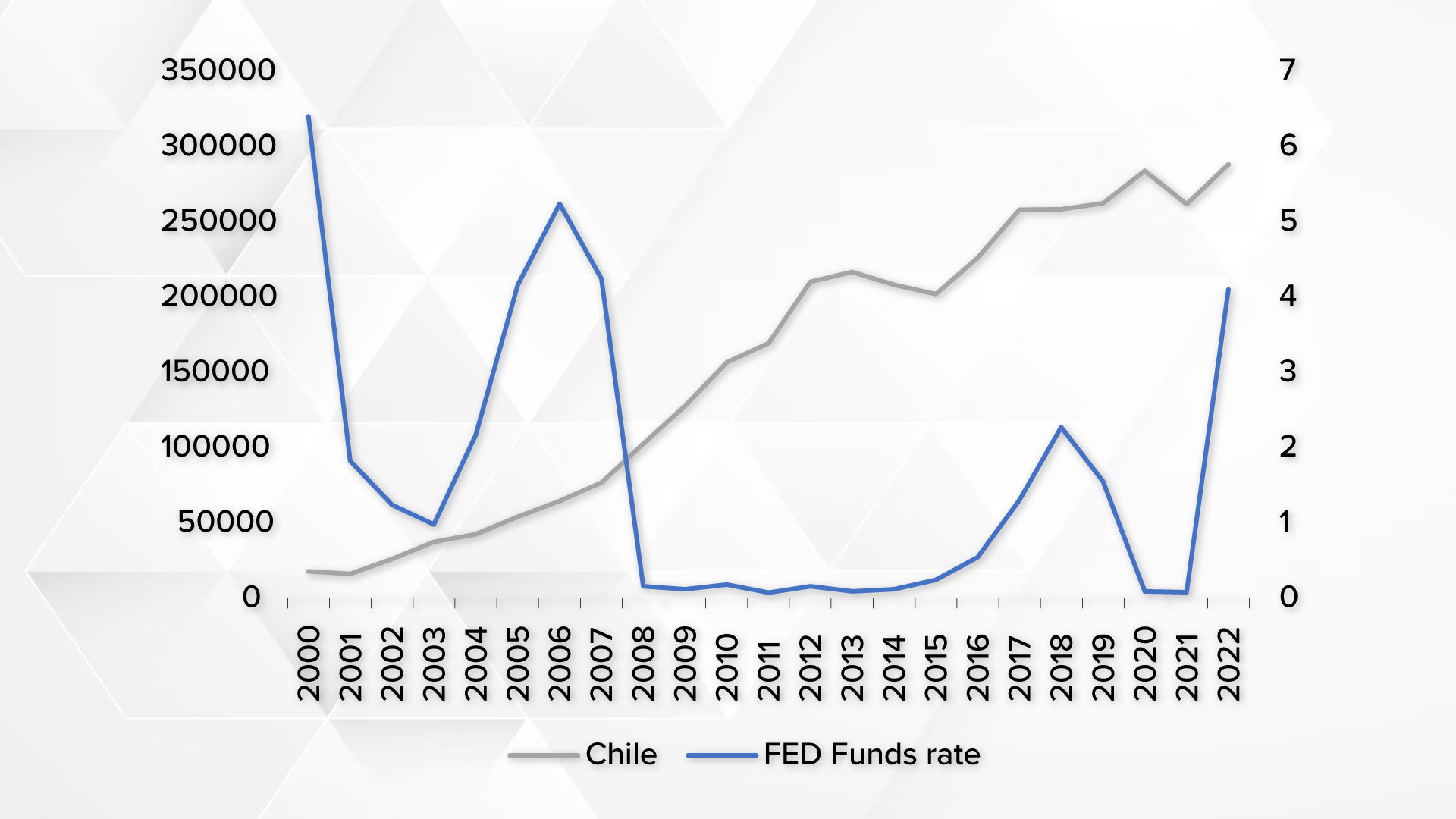

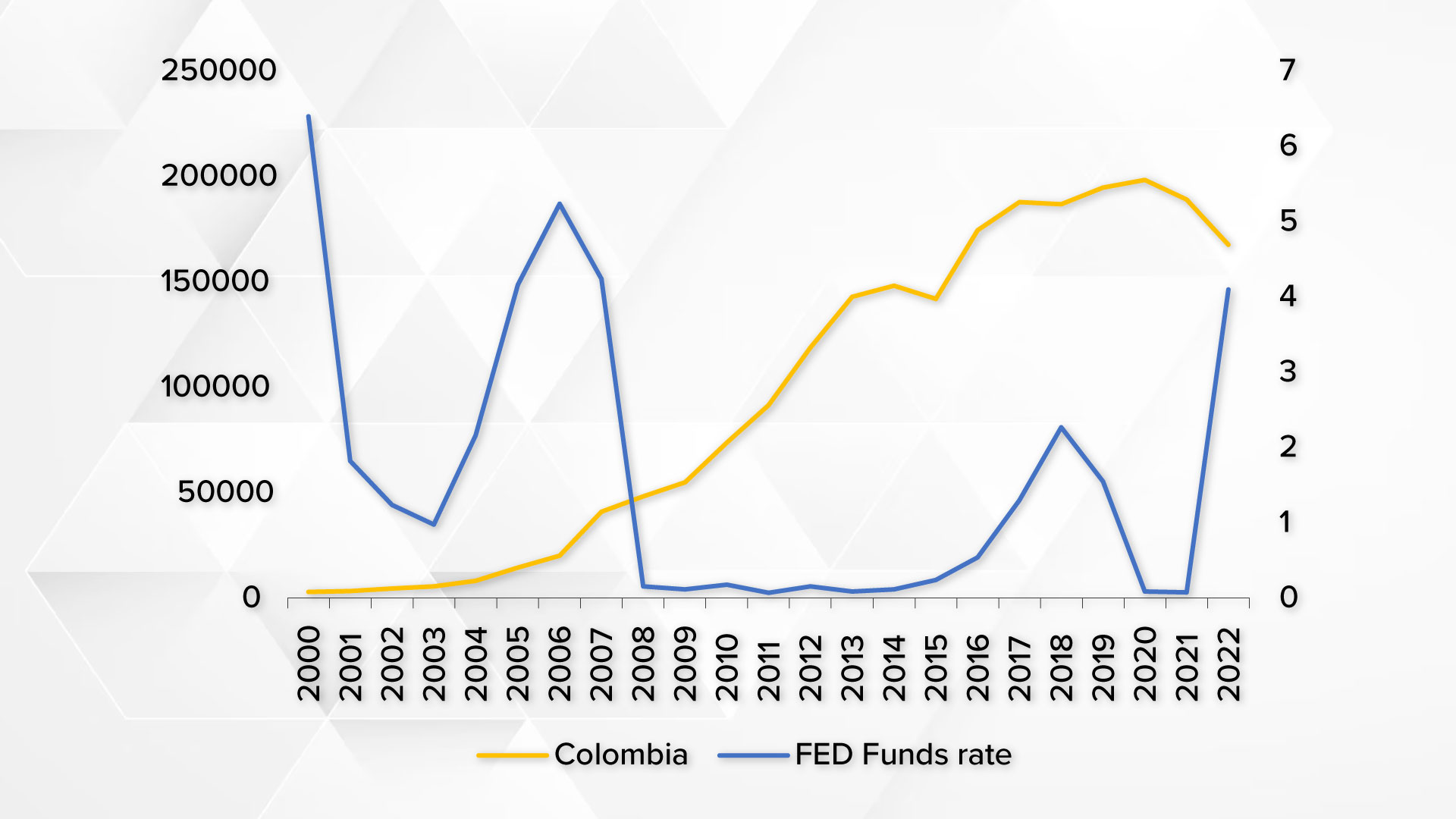

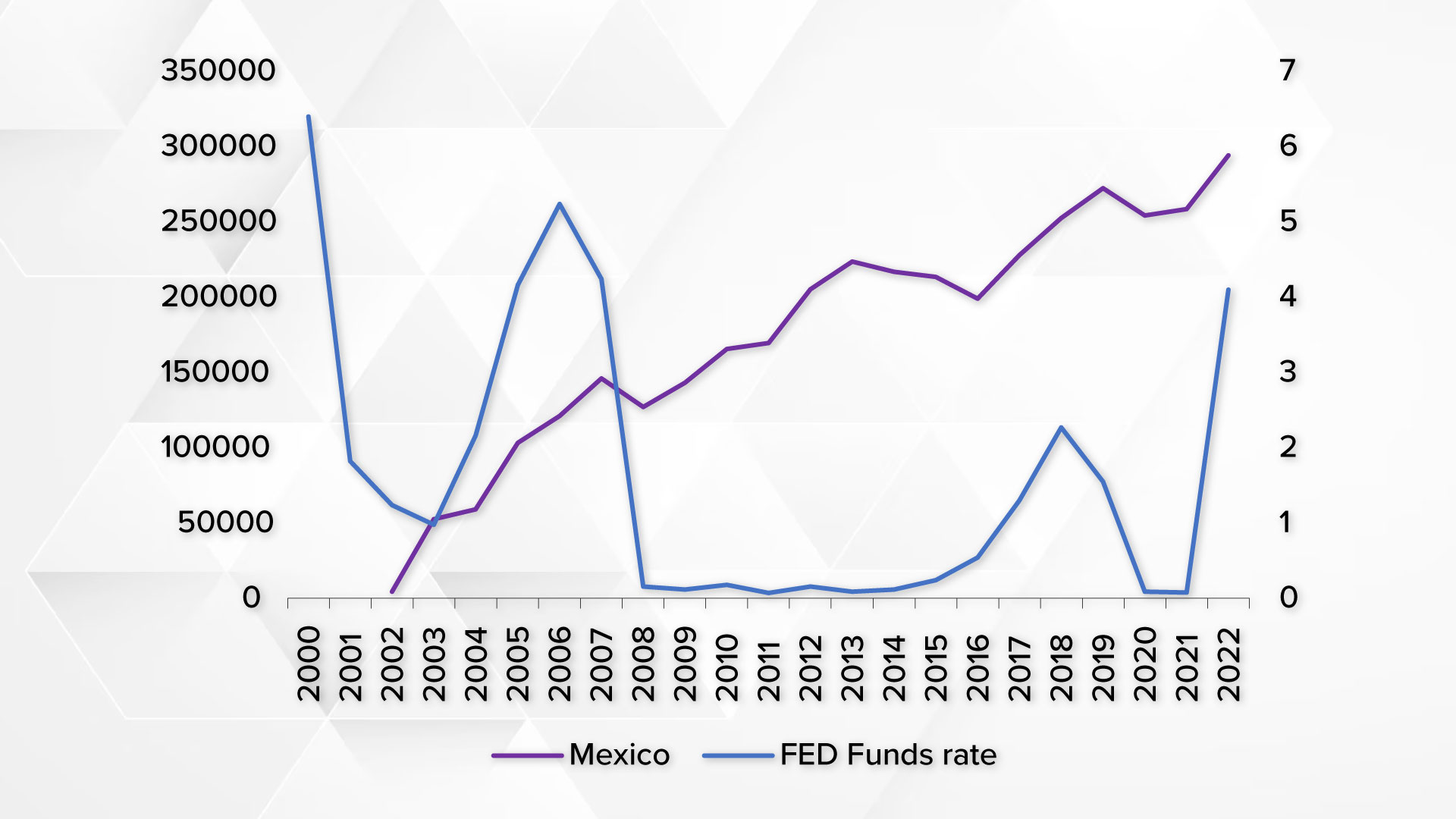

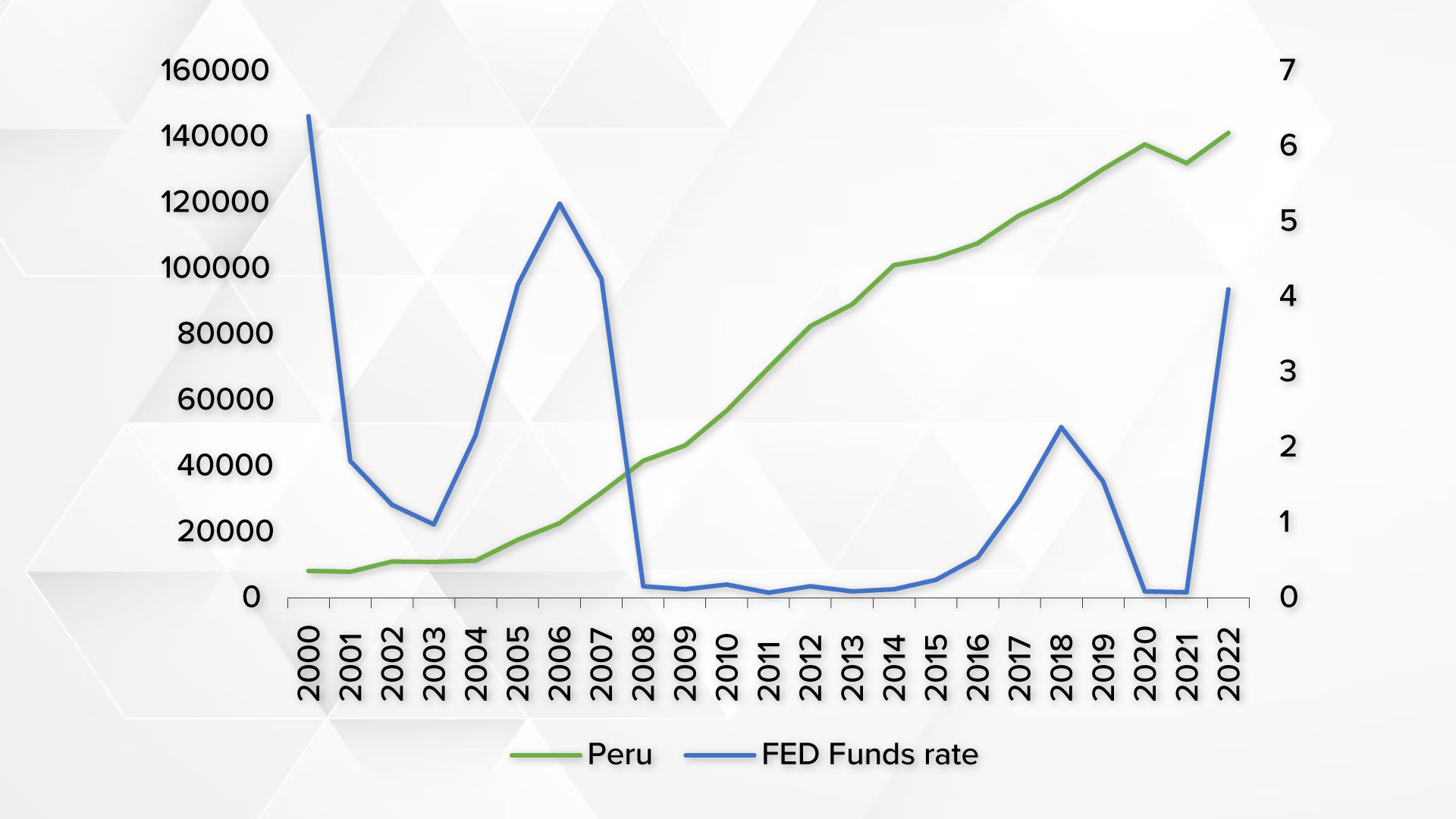

Initial analyses revealed a negative correlation between loan growth rates in the five countries and the Fed Fund Rate, with the correlation being most pronounced (in absolute terms) for Brazil, Chile, and Colombia (see Figure 1). These results present compelling evidence that suggests a connection between U.S. monetary policy and bank loans in Latin American countries. However, traditional monetary theory argues that only unanticipated monetary shocks have an impact on loan growth rates.

Figure 1. Total Loans by Country and the Fed Funds Rate

Our results, based on the banks’ microdata and a dynamic panel-data estimation, indicate the existence of an international bank lending channel extending from the U.S. to the five major Latin American countries. Specifically, on average, a one-percentage-point increase in the Fed funds rate leads to an 80.6 basis-point reduction in the growth rate of loans extended by banks. Parallel to findings in studies concerning the conventional local bank lending channel, liquidity, and solvency emerge as pertinent factors elucidating disparities in bank lending practices across Latin American banks. As anticipated, banks with greater liquidity and solvency profiles tend to exhibit higher rates of loan supply growth. This effect is slightly more pronounced when country-specific effect variables are incorporated.

Our findings demonstrate the presence of an international bank lending channel, even in countries where the presence of U.S. banks is minimal, leading to constrained cross-border bank lending activities. Although the examination of transmission channels falls beyond the purview of this paper, it is plausible that these channels could be linked to the reactions of local commercial banks to U.S. monetary policy innovations. Upon the emergence of a positive U.S. monetary policy shock, local bankers develop expectations that their domestic central banks will react in a commensurate manner. Consequently, they anticipate and respond to these expectations by restraining lending activities. Crucially, our chosen shock measure is entirely exogenous to other relevant factors in the global economy, allowing us to address the direct transmission through the bank-lending channel, devoid of the influence of financial and real uncertainty shocks.

References

Bu, C., Rogers, J. and Wu, W. (2021). A unified measure of Fed monetary policy shocks. Journal of Monetary Economics 118: 331-349.

Huertas, G. (2022). Why Follow the Fed? Monetary Policy in Times of U.S. Tightening. IMF Working Paper WP/22/243.