Authors:

Carlos Giraldo, Latin America Reserve Fund, Bogotá, Colombia – cgiraldo@flar.net

Iader Giraldo, Latin America Reserve Fund, Bogotá, Colombia – igiraldo@flar.net

Jose E. Gomez-Gonzalez, Department of Finance, Information Systems, and Economics, City University of New York – Lehman College, Bronx, NY, USA. | Visiting Professor, Escuela Internacional de Ciencias Económicas y Administrativas, Universidad de La Sabana, Chía, Colombia. – jose.gomezgonzalez@lehman.cuny.edu

Jorge M. Uribe, Faculty of Economics and Business, Universitat Oberta de Catalunya, Barcelona, Spain. – juribeg@uoc.edu

A fundamental tenet of contemporary economic theory underscores the beneficial role of finance in fostering economic growth. Despite the well-established advantages associated with the development of credit markets and their positive impact on long-term economic prosperity, it is imperative to recognize that an unrestrained surge in loan activity may yield adverse consequences for both the financial system and the broader economy.

The annals of financial history, notably exemplified by the Global Financial Crisis (GFC), offer a poignant illustration of the perils associated with excessive credit expansion. Numerous instances of financial crises have been foreshadowed by periods characterized by abnormal credit growth, giving rise to the formation of asset price bubbles. This deleterious scenario is likely to materialize when, during periods of economic expansion, entities such as banks, firms, and households systematically underestimate risk. In consequence, their actions may augment the likelihood of encountering financial distress in the future.

This phenomenon is often attributed to myopic behavior exhibited by private agents. Alternatively, other scholars emphasize the pivotal role played by asymmetric information and financial frictions in credit markets. Irrespective of the underlying catalyst, the mitigation of excessive credit growth has emerged as a pivotal objective for central banks and macro-prudential policymakers worldwide. Emerging market economies have implemented a repertoire of measures aimed at curbing unwarranted credit expansion, thereby safeguarding future financial stability. An essential query, however, pertains to the strategic considerations surrounding the intervention to restrain excessive credit growth. Crucially, determining the threshold that characterizes credit growth as excessive and devising timely mechanisms for its identification constitute formidable challenges. Notably, the immediacy with which credit growth unfolds eludes swift observation by policymakers. Consequently, the development of early warning indicators assumes paramount significance to proactively identify and address burgeoning instances of excessive credit expansion.

Early warning systems represent a crucial asset for regulatory bodies and financial system overseers. While on-site monitoring stands out as a premier means through which authorities can glean both quantitative and qualitative insights into the fiscal well-being of the entities under scrutiny, the execution of such monitoring at a high frequency can incur substantial costs. Moreover, an additional concern arises in the form of potential perceptual biases on the part of those conducting the monitoring.

In our most recent study, to be published in the coming weeks, we leverage weekly datasets pertaining to loan growth in the Colombian context. Employing a two-step machine-learning methodology, we systematically craft a daily indicator encapsulating the dynamics of credit growth. This approach not only allows for a granular assessment of credit expansion daily but also facilitates the identification of periods characterized by excessive credit growth.

Concretely, in the first step, we use Random Forests (RF) for constructing a daily indicator of credit growth, which is originally sampled on a weekly basis. Specifically, we identify the missing dates in the raw credit indicator and employ RF to fill these gaps, harnessing the information contained in our high frequency indicators which include various spreads, overnight interbank interest rates, and stock market returns. Subsequently, we use quantile random forest, a fusion of quantile regression and RF, to identify periods of excessive credit creation, which are of concern for regulators. We specifically focus on the credit growth quantiles above 95%, which correspond with scenarios of rapid credit growth and likely predict future scenarios of financial and macroeconomic stability.

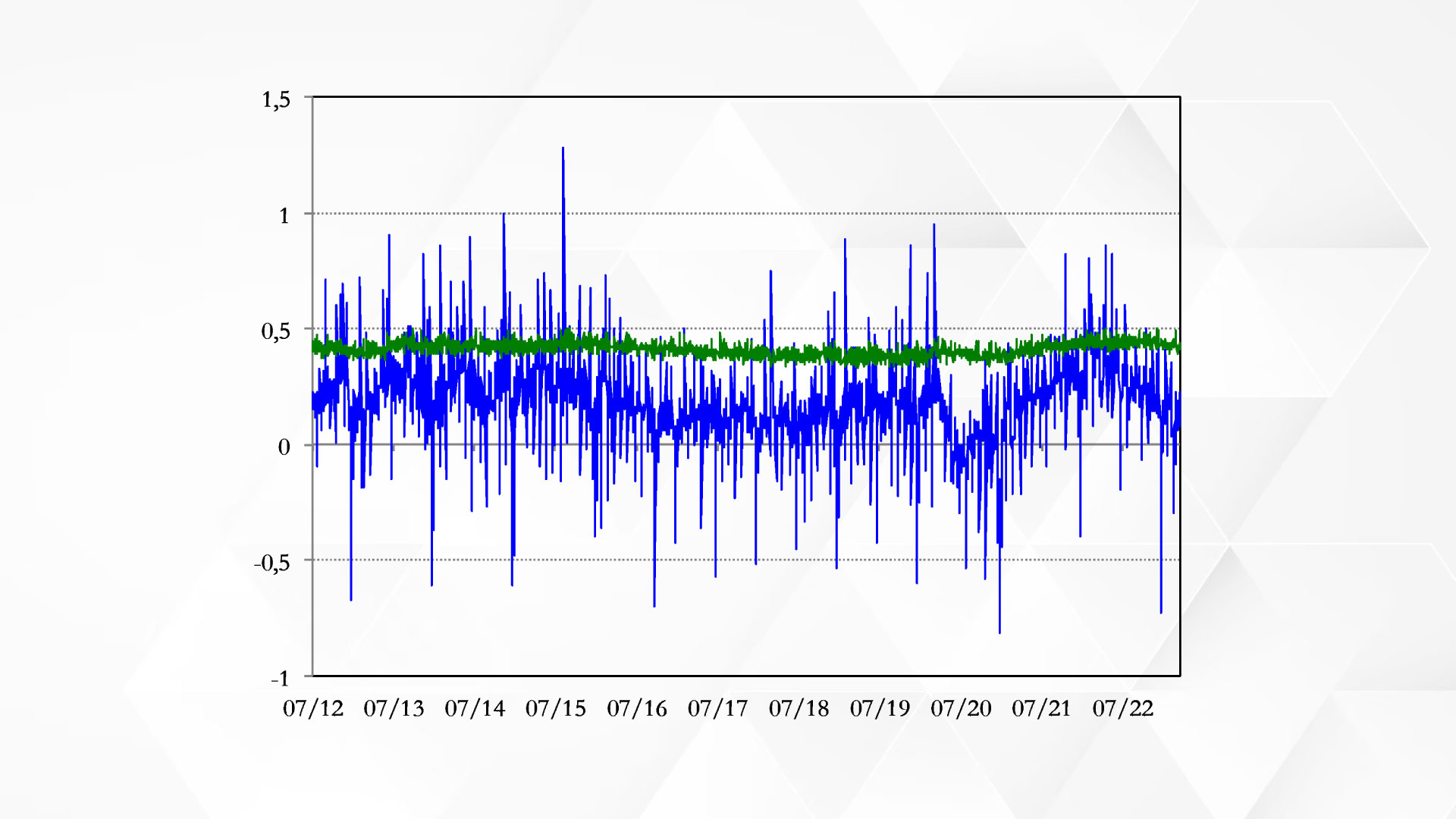

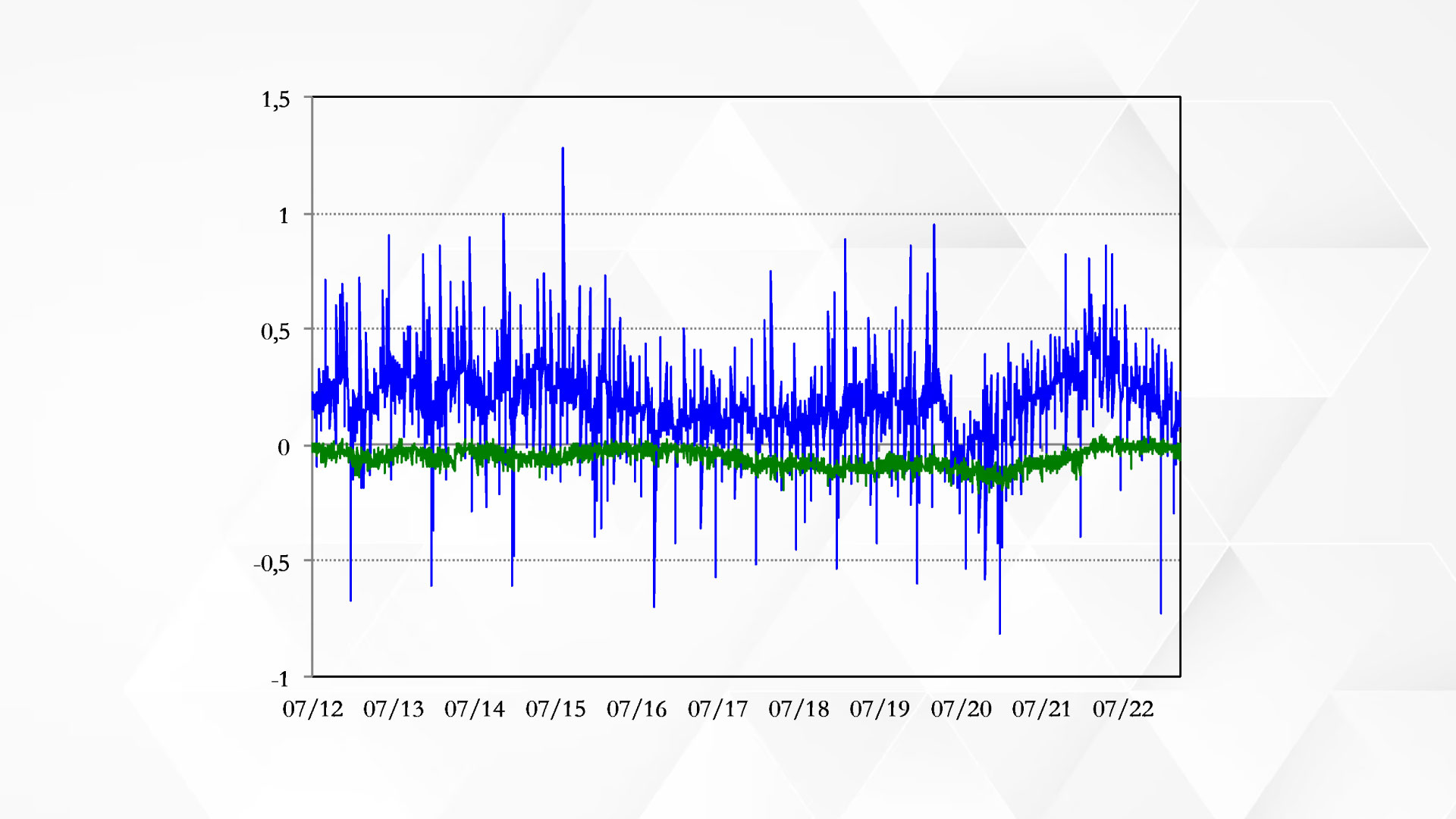

Figure 1 unveils the principal findings of our study, illustrating the series encompassing the high (95th) and low (5th) quantiles of daily credit growth juxtaposed against the overall daily credit growth trajectory. The blue curve in the graph depicts the daily credit growth series, while the green curve represents the high quantiles (left panel) and low quantiles (right panel) of daily credit growth.

Figure 1. High (95th) and low (5th) quantiles of credit growth versus credit growth

Panel A.

Quantile 95% of credit growth

Panel B.

Quantile 5% of credit growth

Several noteworthy outcomes merit attention. Firstly, both high and low credit growth quantiles exhibit temporal variability, highlighting the influence of macroeconomic and financial cycles in identifying instances of exceptionally high or low credit growth. Consequently, the practice of establishing ad hoc definitions for such extremes, as commonly done by central bankers, is less advisable. Our model provides an endogenous and precise means of identifying the significance of high and low credit growth for any given day, facilitating the implementation of macro-prudential policies by central bankers.

Secondly, instances of credit growth surpassing or falling below a certain threshold signify abnormally high or low values of daily credit growth. Notably, these periods are not randomly distributed over time; clusters are discernible. Specifically, elevated credit growth days were concentrated between 2012 and early 2015, marked by high international oil prices and significant capital inflows to Colombia, a major oil-producing nation. Another period of abnormally high credit growth occurred during the Covid-19 pandemic, correlating with a substantial reduction in Colombia’s policy interest rate and government measures to enhance credit availability. Policymakers are thus urged to exercise vigilant credit growth monitoring during commodity price surges.

Thirdly, it is crucial to observe that periods of abnormally low credit growth are more prone to occur after phases characterized by high credit growth. This pattern aligns with predictions from financial cycle studies, indicating that prolonged periods of abnormally high credit growth adversely impact the overall health of banks and financial institutions. These scenarios erode confidence and hinder credit extension immediately thereafter.

Our study presents a two-step machine-learning approach to generate a daily indicator for credit expansion in emerging market economies, surpassing traditional data’s limitations. The proposed tool offers a granular, real-time assessment of credit expansion and can enable proactive intervention by policymakers and financial authorities while mitigating risks associated with excessive credit growth. This research makes a significant contribution to the field of financial stability in emerging markets by providing a high-frequency, data-driven approach to credit monitoring, empowering policymakers to safeguard financial stability.