Authors:

Carlos Giraldo – Latin American Reserve Fund | FLAR.

Iader Giraldo – Latin American Reserve Fund | FLAR.

Jose E. Gomez-Gonzalez – Lehman College, City University of New York; and, Visiting Professor (Summer School), Universidad de La Sabana.

Jorge M. Uribe – Open University of Catalonia York.

Several studies have shown that exaggerated and sustained credit growth is one of the main causes of financial crises in both developed (Schularick and Taylor, 2012) and emerging economies (Amador-Torres et al., 2013). Recognition of this has led central banks in various countries to monitor credit behavior and take measures such as increases in policy interest rates and reserve requirements at times when they consider that aggregate credit is growing at higher than acceptable rates.

In small, open economies, such as most countries in Latin America and the Caribbean (LAC), credit growth is closely related to the behavior of capital flows. Capital inflow booms lead to abnormal credit growth in these countries and significantly increase the probability of banking crises, as shown by Caballero (2016). For this reason, during the last two decades, macroeconomic policymakers in some of these countries have implemented prudential measures that seek to correct the potentially destabilizing macroeconomic imbalances generated by such capital booms and that go beyond the scope of traditional financial stability policy measures that seek to preserve the individual stability of financial intermediaries. This set of policy measures has been generically referred to as macroprudential measures.

Although there is a considerable variety of policies that fall under these measures, many of them are aimed at restricting or limiting the speed of short-term capital inflows that may be subject to sudden capital reversals in times of high financial stress. Among the best known and most widely implemented are foreign currency credit deposits and short-term capital investments. Countries such as Brazil, Colombia, and Chile, among many others, have implemented this type of measures in times of high capital inflows and appreciation of local currencies against the dollar.

In early 2007, in an international context of low interest rates and high risk appetite, capital inflows to LAC countries increased substantially. Consistent with this, asset prices such as housing and bonds increased while local currencies appreciated considerably against the dollar. Some countries imposed macroprudential measures, mainly deposits on foreign indebtedness and portfolio capital inflows, seeking to limit the magnitude of the boom and its impact on credit growth and the financial vulnerability of local agents. At the same time, central banks took the measures available to them to moderate credit growth rates in local currency.

The policy challenges were great. Interest rate increases by the region’s central banks, which sought to moderate local currency credit growth, encouraged the acceleration of foreign capital inflows due to the permanence of low interest rates in developed economies. While deposits helped to contain such capital inflows, external agents and local financial intermediaries devised ways to overtake imposed measures, for example, by replicating foreign currency credit through a synthetic involving local currency credit and an exchange rate swap. These synthetics were not limited by traditional implemented measures.

In the midst of this situation, the Banco de la República (Colombia’s central bank) announced on Sunday, May 6, 2007 a measure that sought to restrict the growth of credit risk exposure of Colombian financial intermediaries with local agents and foreign financial entities. It also sought to restrict the ability of the Colombian real sector to take speculative positions with local agents that could exacerbate liquidity problems and pressures on the exchange rate. The measure, known as Gross Leverage Position (PBA) consisted of a maximum limit of 500% of the gross position ratio in foreign exchange derivatives to technical equity of Colombian financial entities. The intention of those who designed the policy was to reduce the risk of excessive exposure of local agents to foreign currency indebtedness through derivative transactions.

The PBA was at the time a unique and original macroprudential measure implemented only in Colombia. So far, only South Korea has implemented a similar measure. In our recent paper «Banks’ Leverage in Foreign Exchange Derivatives in Times of Crises: A Tale of Two Countries», we use synthetic control methods following the seminal work of Abadie and Gardeazabal (2003) and Abadie et al. (2010) to assess the causal effect of the PBA on financial stability in Colombia

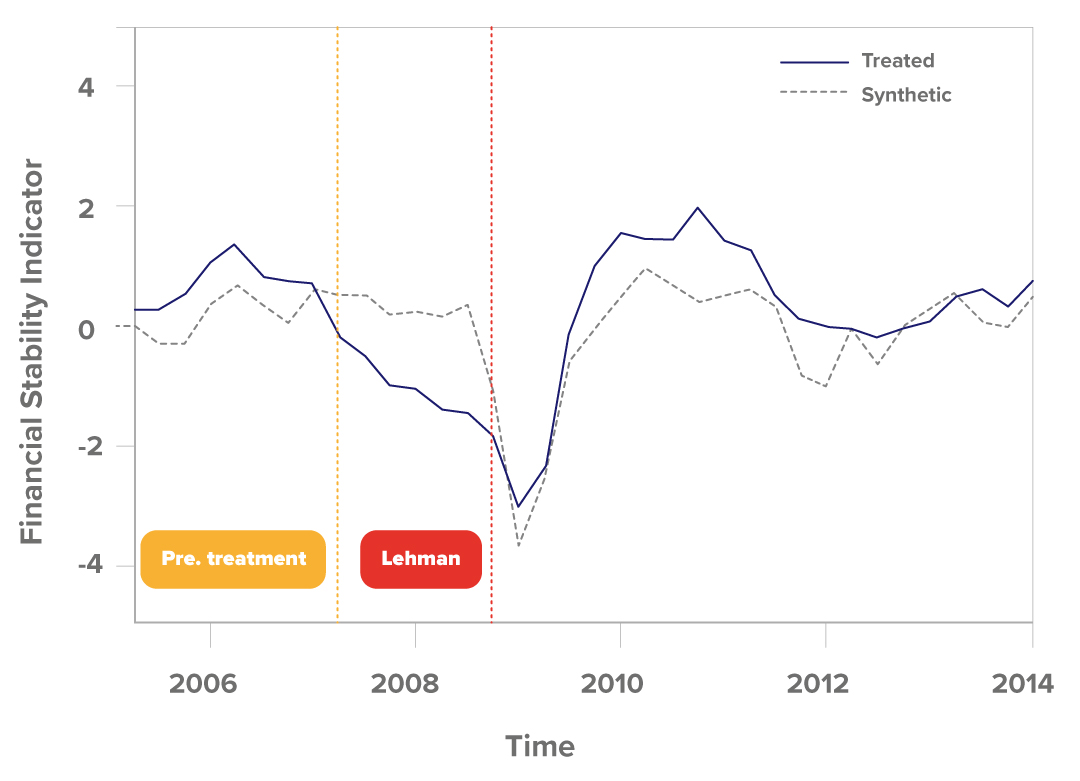

Figure 1 Observed (treated) versus synthetic Colombia

Figure 1 shows the effect of the application of the PBA on the financial stability index. The actual and counterfactual values of this index are plotted. The solid line represents the behavior over time of the index for Colombia (treated). The dotted line represents the behavior of the index for synthetic Colombia (control). Two moments in time stand out, namely the date when the PBA was implemented (quarter corresponding to May 6, 2007) and the date of Lehman Brothers’ default in September 2008. Higher (lower) values of the index correspond to situations of greater (lesser) financial stability. According to the results, the PBA had an impact on financial stability in Colombia. However, the impact was not homogeneous over time. When the policy measure was adopted, before the onset of the global financial crisis, the PBA was detrimental to the overall financial stability of the Colombian financial sector. This seemingly counterintuitive result can be explained by the fact that this macroprudential policy limits the ability of banks to grant foreign currency loans to firms. In fact, firms that had high levels of foreign currency debt may have found it more difficult to refinance loans and may have had to pay higher interest rates for new loans issued. This, in fact, may have had a negative impact on financial stability.

However, shortly after the bankruptcy of Lehman Brothers, the effect of the PBA on Colombia’s financial stability was reversed. Liquidity became scarce during the global financial crisis. The PBA had a preemptive effect, limiting the exposure of the country’s banks and companies to foreign currency denominated debt before this occurred. Therefore, these companies and banks were less exposed to developments in international financial markets during the global financial crisis. This insulation effect produced by the PBA was beneficial in safeguarding the stability of the Colombian financial system during times of severe financial stress in global financial markets.

These results suggest that the PBA is a valuable policy measure as part of the macroprudential policy toolbox available to monetary authorities in order to safeguard macroeconomic and financial stability in the face of strong capital inflows and accelerated domestic credit growth. Although this policy tool could entail costs at the beginning of its implementation, there are subsequent benefits that significantly contribute to macroeconomic and financial stability in times of crisis.

References

Abadie, A., & Gardeazabal, J. (2003). The economic costs of conflict: A case study of the Basque Country. American economic review, 93(1), 113-132.

Abadie, A., Diamond, A., & Hainmueller, J. (2010). Synthetic control methods for comparative case studies: Estimating the effect of California’s tobacco control program. Journal of the American statistical Association, 105(490), 493-505.

Amador-Torres, J.S., Gomez-Gonzalez, J.E., and Murcia Pabon, A. (2013). “Loan growth and bank risk: new evidence,” Financial Markets and Portfolio Management 27:365–379.

Caballero, J. (2016). “Do Surges in International Capital Inflows Influence the Likelihood of Banking Crises?” Economic Journal 126: 281-316.

Schularick, M., Taylor, A.M. (2012). “Credit Booms Gone Bust: Monetary Policy, Leverage Cycles, and Financial Crises, 1870-2008,” American Economic Review 102: 1029-1061.