Authors1:

Christian Alcarraz, FLAR, Bogotá, Colombia. – calcarraz@flar.net

Carlos Giraldo, FLAR, Bogotá, Colombia. – cgiraldo@flar.net

Andrea Villarreal, FLAR, Bogotá, Colombia. – avillarreal@flar.net

Liz Villegas , FLAR, Bogotá, Colombia. – lvillegas@flar.net

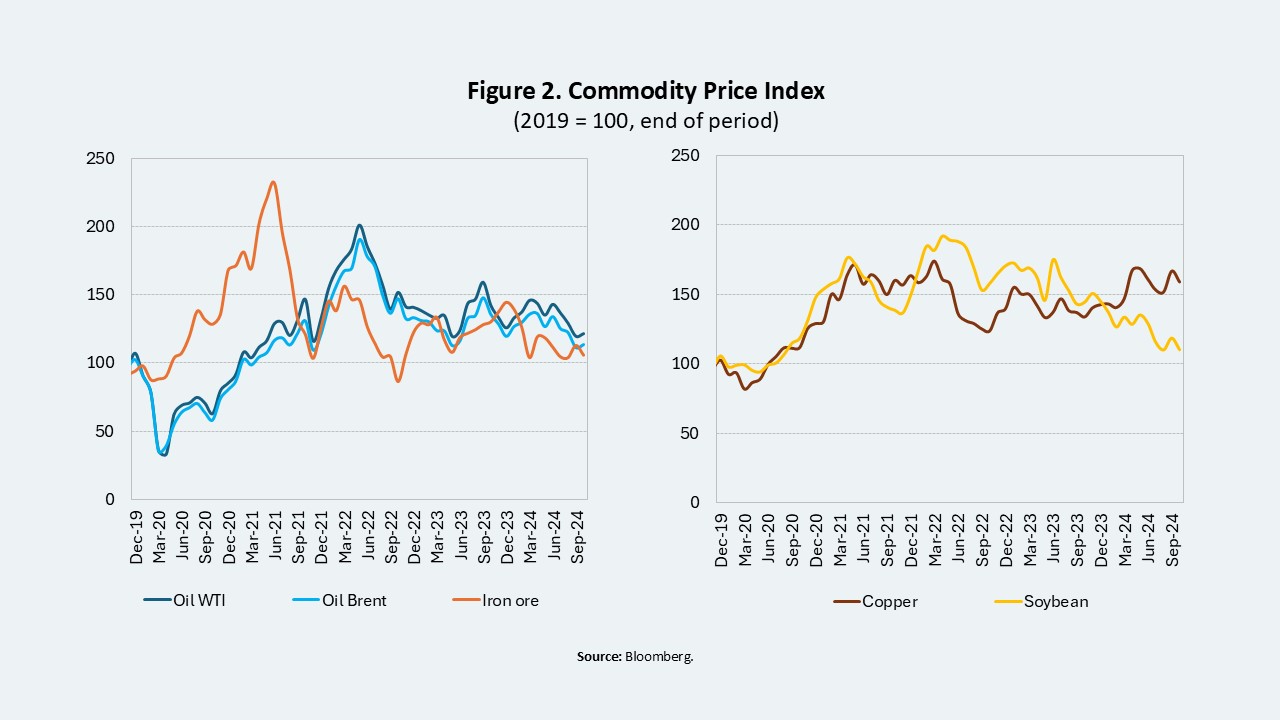

Throughout the year, the global economy has experienced a slight deceleration in growth compared to 2023, accompanied by inflation rates aligning more closely with target levels. This trend has enabled central banks in the Eurozone and the United States to initiate reductions in interest rates. For Latin America, this development has led to a decline in the prices of most commodities—although they remain elevated—while external financing costs have gradually decreased, particularly in the second half of the year.

The U.S. economy grew at an annual rate approaching 3%, demonstrating resilience despite a high-interest-rate environment. This strong performance was driven by robust consumer spending and increased public expenditure. In contrast, the Eurozone exhibited signs of fragility, with growth falling below 1%, primarily due to weakening private sector spending. Meanwhile, China reported growth below its 5% government target, hindered by subdued domestic demand and a persistent real estate crisis.

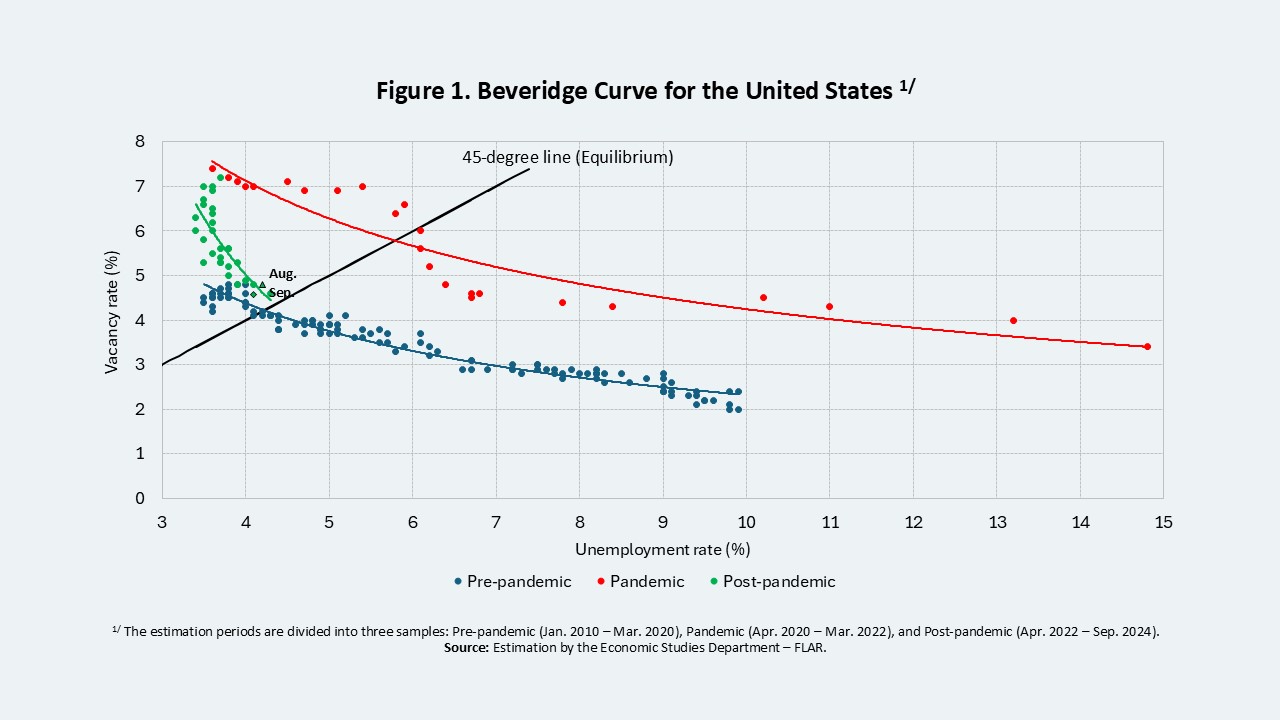

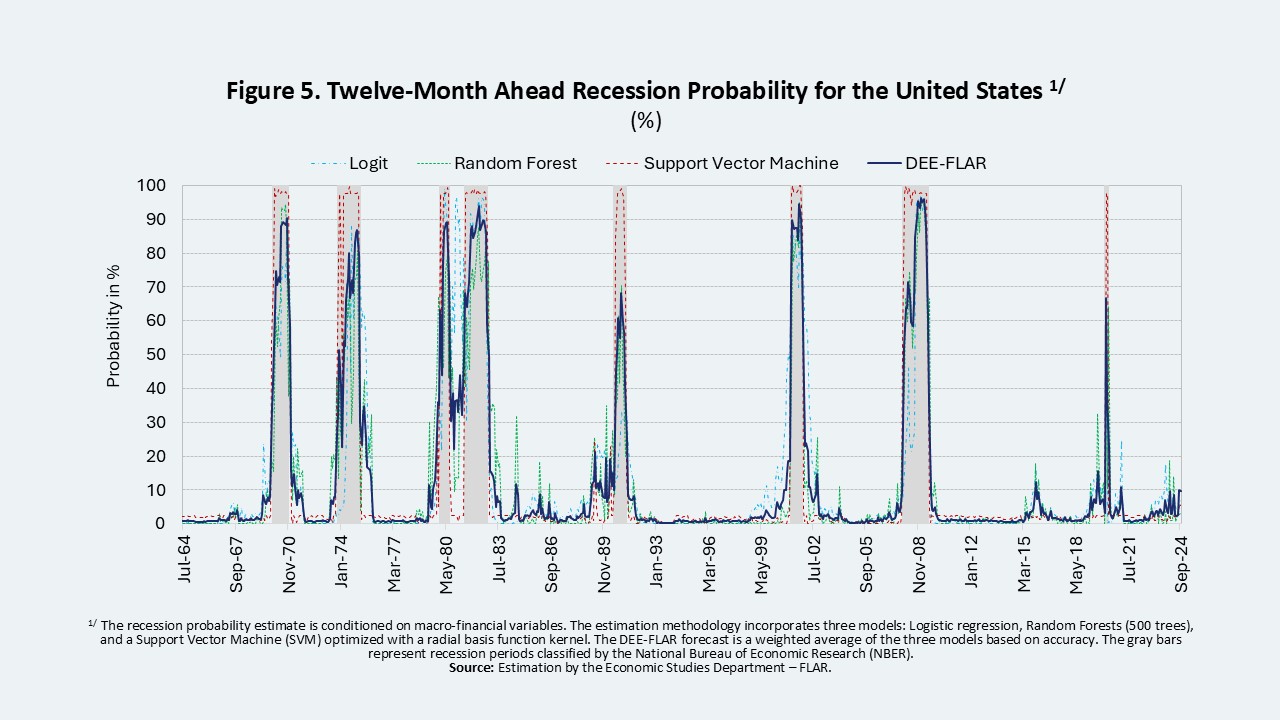

Labor markets in the U.S., Eurozone, and China maintained low unemployment rates, albeit with reduced dynamism. In the U.S. and Eurozone, unemployment rates edged higher, and job vacancies declined. In the U.S., the Beveridge curve suggests that the level of vacancies remains sufficiently elevated to prevent a significant short-term rise in unemployment (Figure 1). This indicates that while the U.S. labor market has lost some momentum, it continues to display resilience. Moreover, wage growth has sustained household consumption, mitigating part of the impact of elevated interest rates.

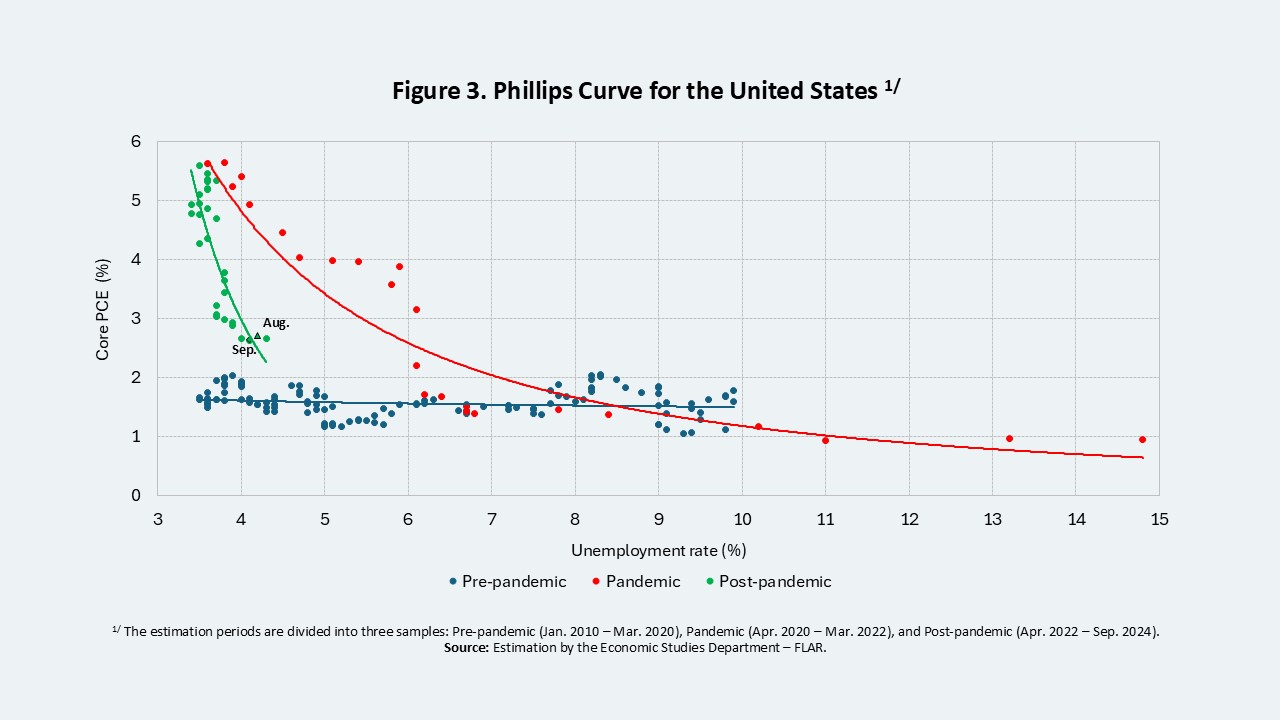

Consumer inflation and the annual variation of core CPI continued to decline across the three economies, although in the U.S. and Eurozone, these metrics remain above pre-pandemic levels. The deceleration in service prices has slowed the pace of disinflation, particularly in the U.S. However, the current slope of the Phillips curve for the U.S. economy indicates that a significant rise in unemployment would not be required to reach the inflation target (Figure 3). In contrast, consumer inflation in China remained low, hovering around 0%.

With declining inflation, major central banks have begun reducing their policy rates. The European Central Bank has led the easing cycle with three consecutive 25-basis-point cuts to its policy rate. Similarly, the Federal Reserve initiated its rate reductions with a 50-basis-point cut, followed by a 25-basis-point reduction. Meanwhile, the People’s Bank of China lowered its 1- and 5-year prime rates to stimulate aggregate demand.

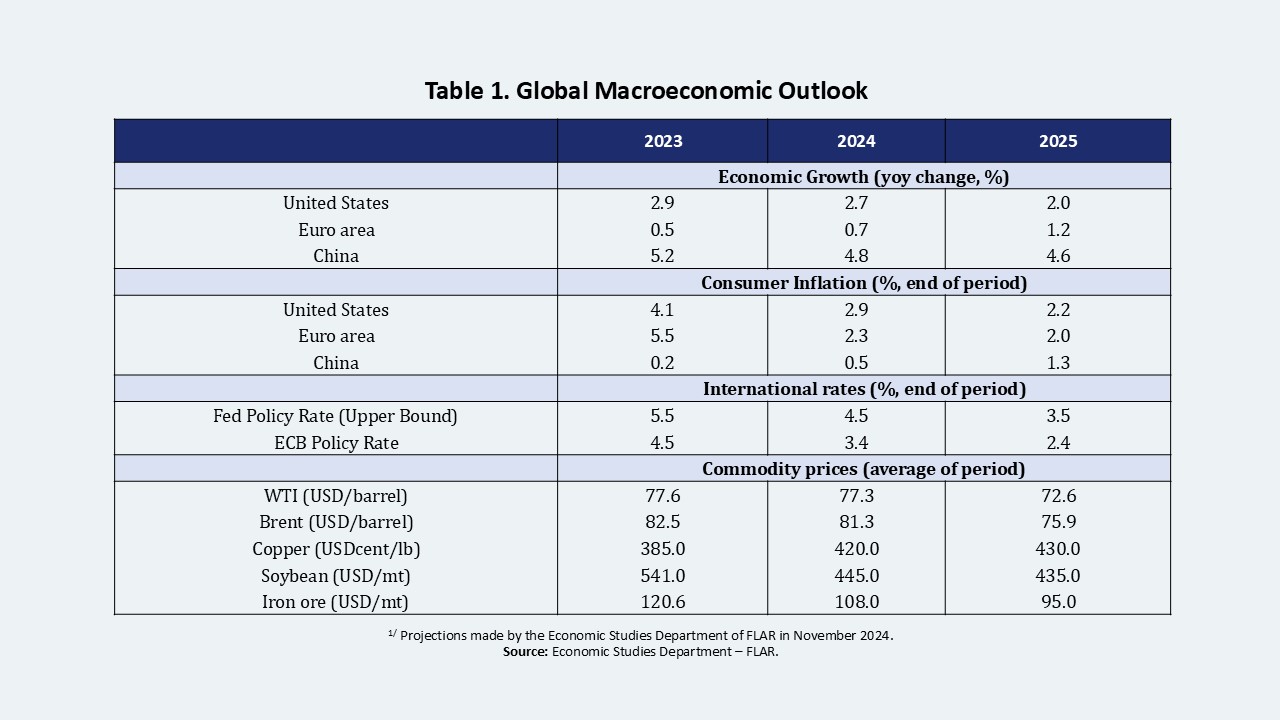

China’s economy is expected to grow below 5%, driven by weak domestic demand and the fragility of the real estate sector. In contrast, the Eurozone is projected to experience a slight acceleration in GDP, explained by a recovery in household consumption within a context of lower interest rates and improved private investment performance.

The low growth across these three economic areas would explain a decline in most commodity prices in 2025 (Table 1), assuming geopolitical conflicts remain at their current scale. Conversely, copper prices are anticipated to rise due to its intensive use in energy transition technologies .

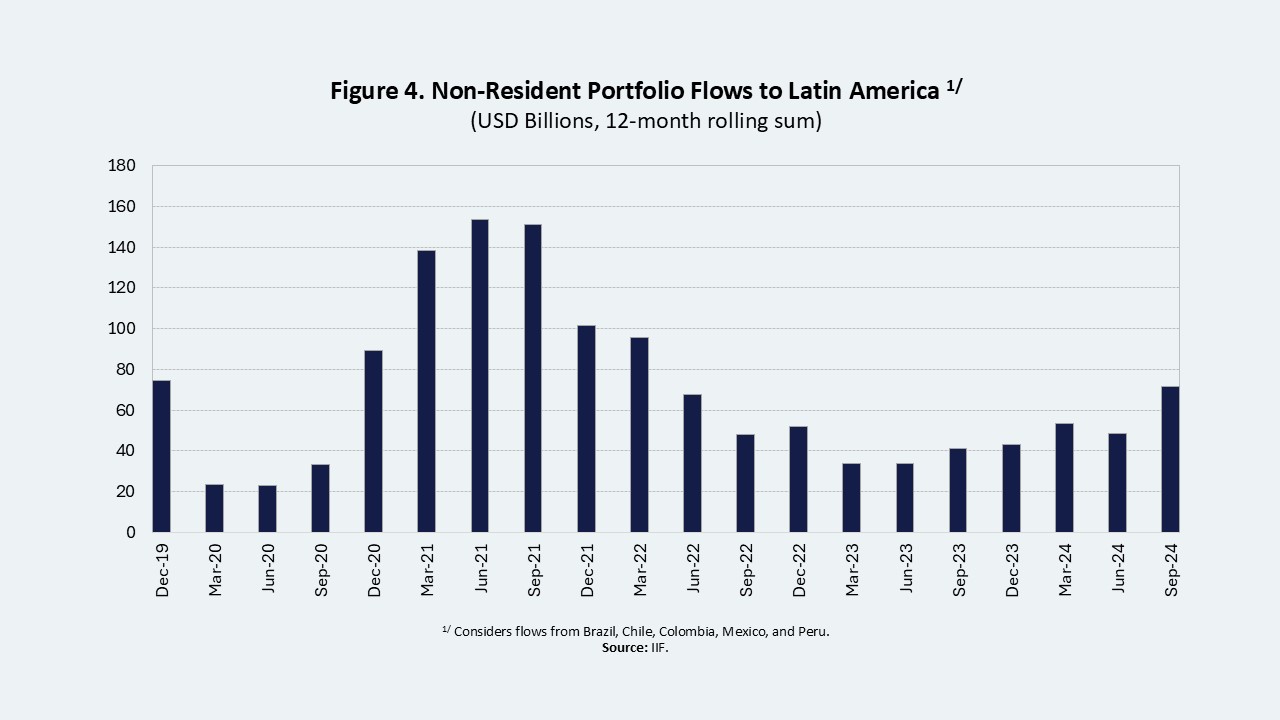

Furthermore, the disinflation process is expected to deepen, accompanied by continued monetary easing (Table 1). Specifically, the Federal Reserve’s policy rate is projected to gradually decline throughout 2025, with a cumulative reduction of 100 basis points, reaching 3.5% by the end of the year (Table 1). Assuming geopolitical tensions and conflicts remain at their current scale, these lower international interest rates are likely to encourage greater capital inflows into the region. However, the disinflationary process could be disrupted or reversed by potential shocks of various types, which would, in turn, halt or reverse the decline in international interest rates.

The greatest source of global uncertainty in our projections arises from the policies of the new U.S. administration (e.g., trade, fiscal, migration, and regulatory policies) and their potential impact on trade, financial, and migratory flows to emerging economies and the region. Geopolitical risks also contribute significantly to this uncertainty.

In summary, the outlook for the U.S., Eurozone, and China collectively points to slower growth, continued disinflation, and lower interest rates. These developments have mixed implications for Latin America, affecting various components of the external accounts in the balance of payments, including prices, volumes, and interest rates.