Authors:

Adriana Arreaza – Director of Macroeconomic Studies – CAF – Latin American Development Bank

Carlos Giraldo – Chief Economist – FLAR – Latin American Reserve Fund

We would like to thank Liz Villegas, Professional Economist, FLAR Economic Studies Directorate, for the compilation and processing of the statistical data used in the blog.

Latin America’s financial system has shown great strength throughout the pandemic, surprising several analysts, who perceived considerable risks suggesting that this real shock would result in financial shock. However, amid tightening global financial conditions, the outlook ahead is challenging.

This blog analyzes the main reasons behind the performance of the financial systems of four of the region’s major economies (Chile, Colombia, Mexico and Peru) since the onset of the pandemic, as well as future risks and challenges. In part, it includes elements of the discussions held during the recent webinar organized by FLAR and CAF on May 2, 2022 (Resilience of the Latin American financial system during the pandemic).

Factors that explain resilience

The factors that explain the good performance of the financial system in the aforementioned economies include the following five internal and external reasons. First, the banking system was in good shape before the pandemic, partly because of the strength of the supervision and regulation inherited from the banking crises of previous decades.

Second, regulatory and supervisory entities showed significant flexibility during the health crisis. Understanding the extraordinary nature of the situation, these entities allowed the adoption of transitional measures aimed at relaxing regulatory and supervisory standards to reduce the strain on the banking system.

Third, the agile monetary response enabled the provision of sufficient liquidity for the financial systems and ensured the smooth operation of the payment system, which facilitated a local environment with extremely low interest rates. In turn, government-provided guarantees also contributed to maintaining the countercyclical behavior of credit activity in several countries.

Fourth, ample international liquidity, led by the U.S. Federal Reserve’s monetary policy, prevented local financial systems from facing pressures as a result of external flows or foreign exchange problems. This happened because the crisis was global in nature and involved the major developed economies.

Fifth, the crisis was caused by a global, real exogenous shock triggered by a public health issue and not by a macro-financial shock, as frequently experienced in the region. This has allowed a quicker recovery of economic activity, even if it has been heterogeneous depending on each of the economy’s initial conditions and public health, economic and financial responses.

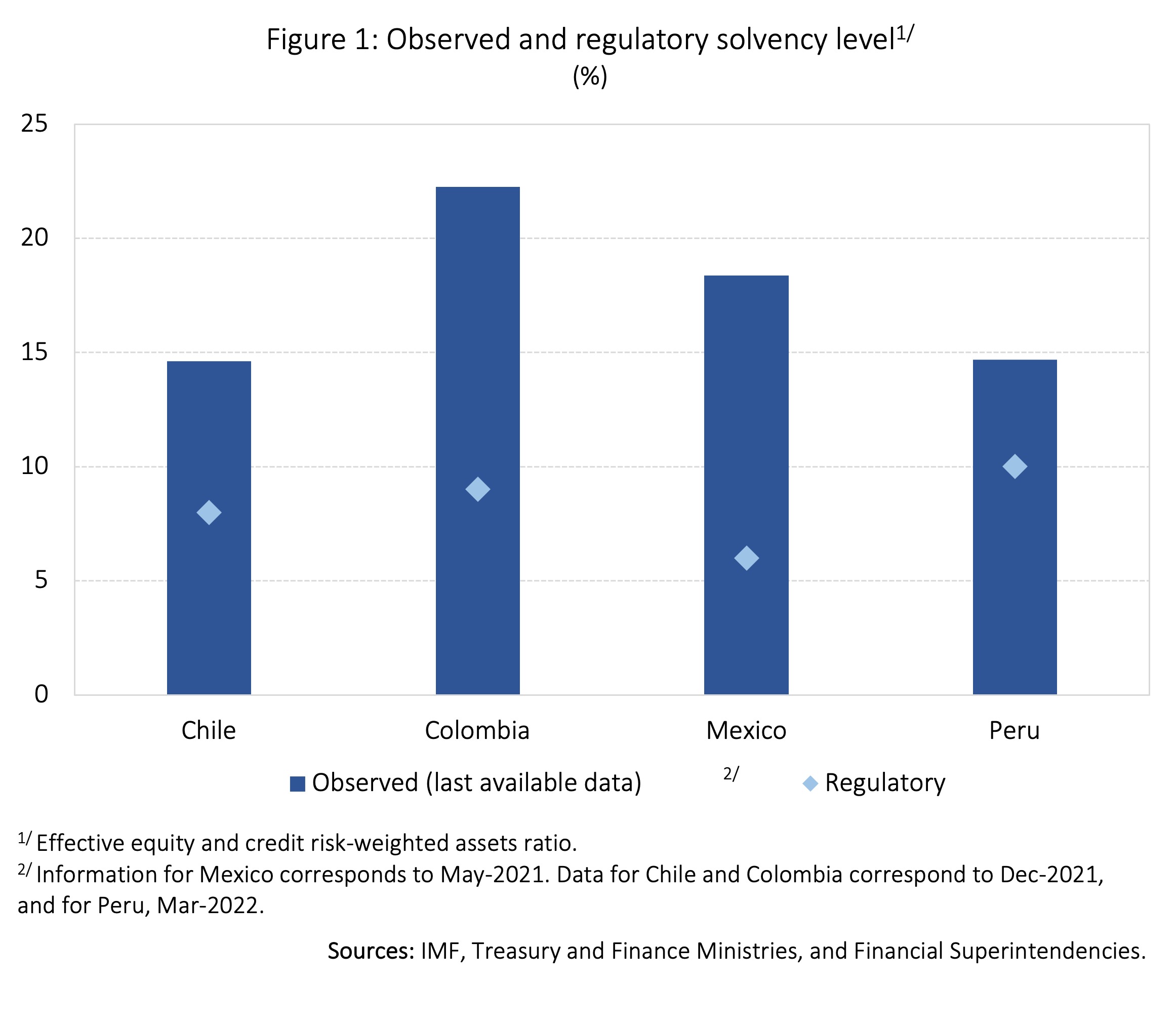

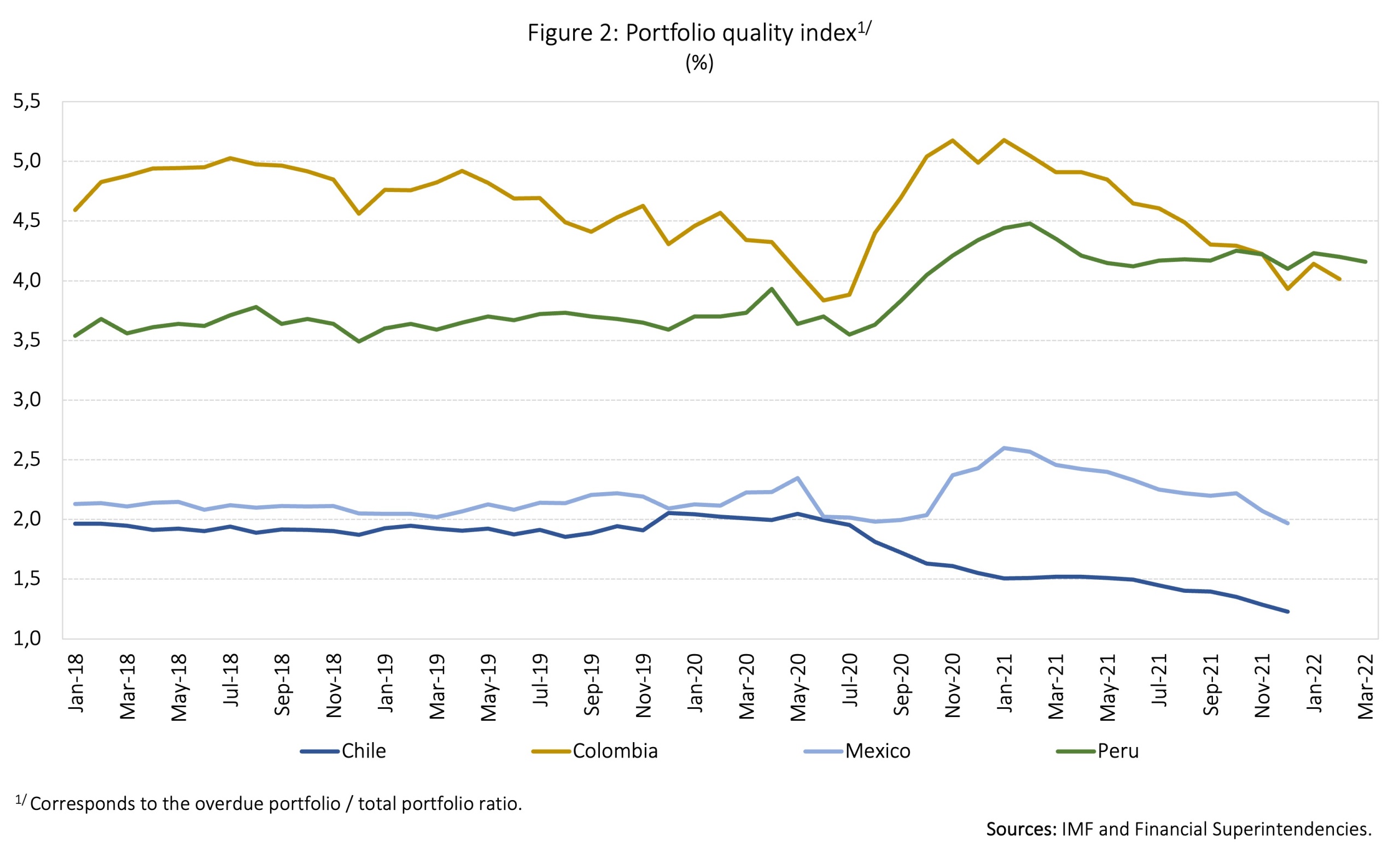

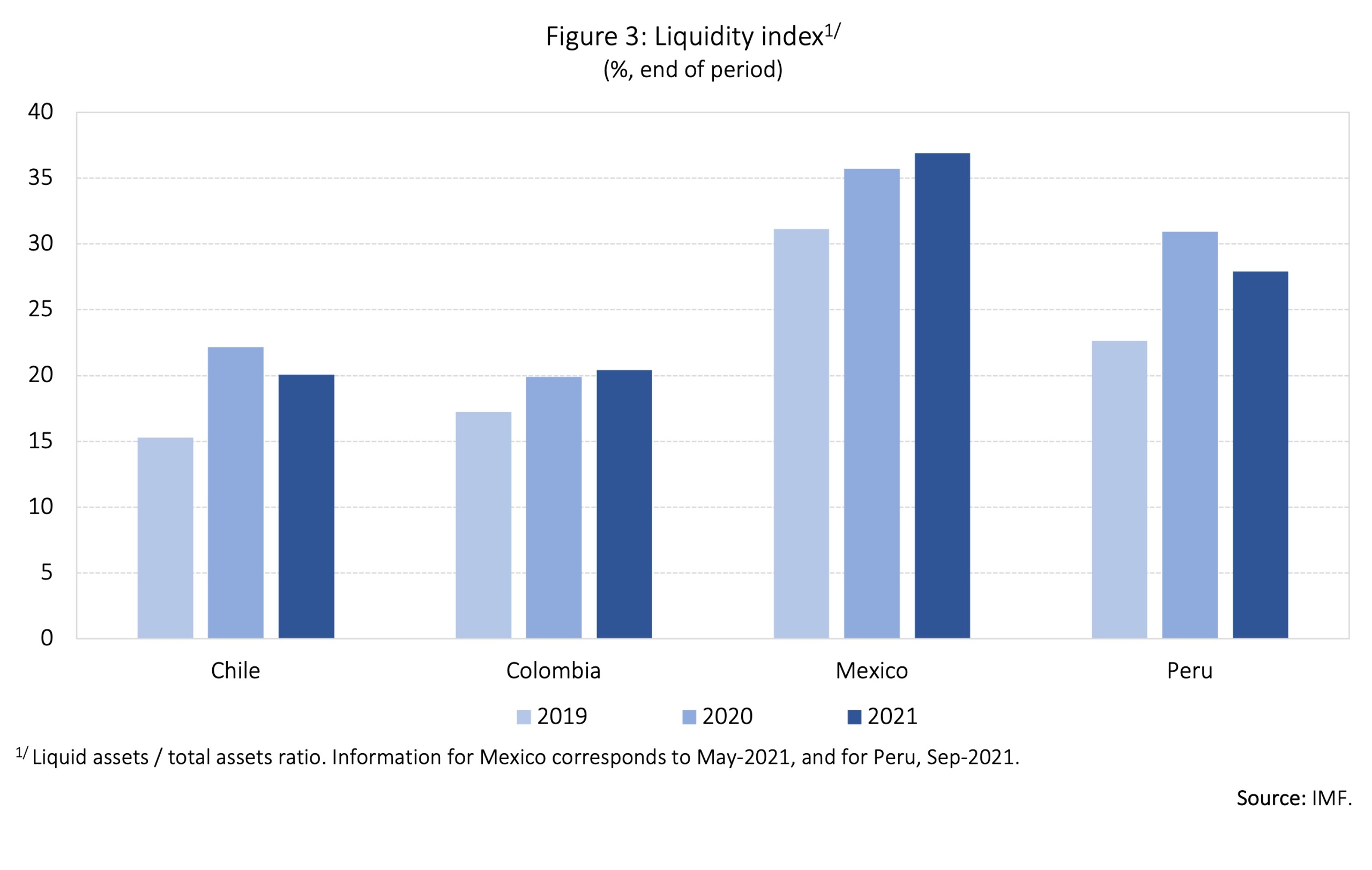

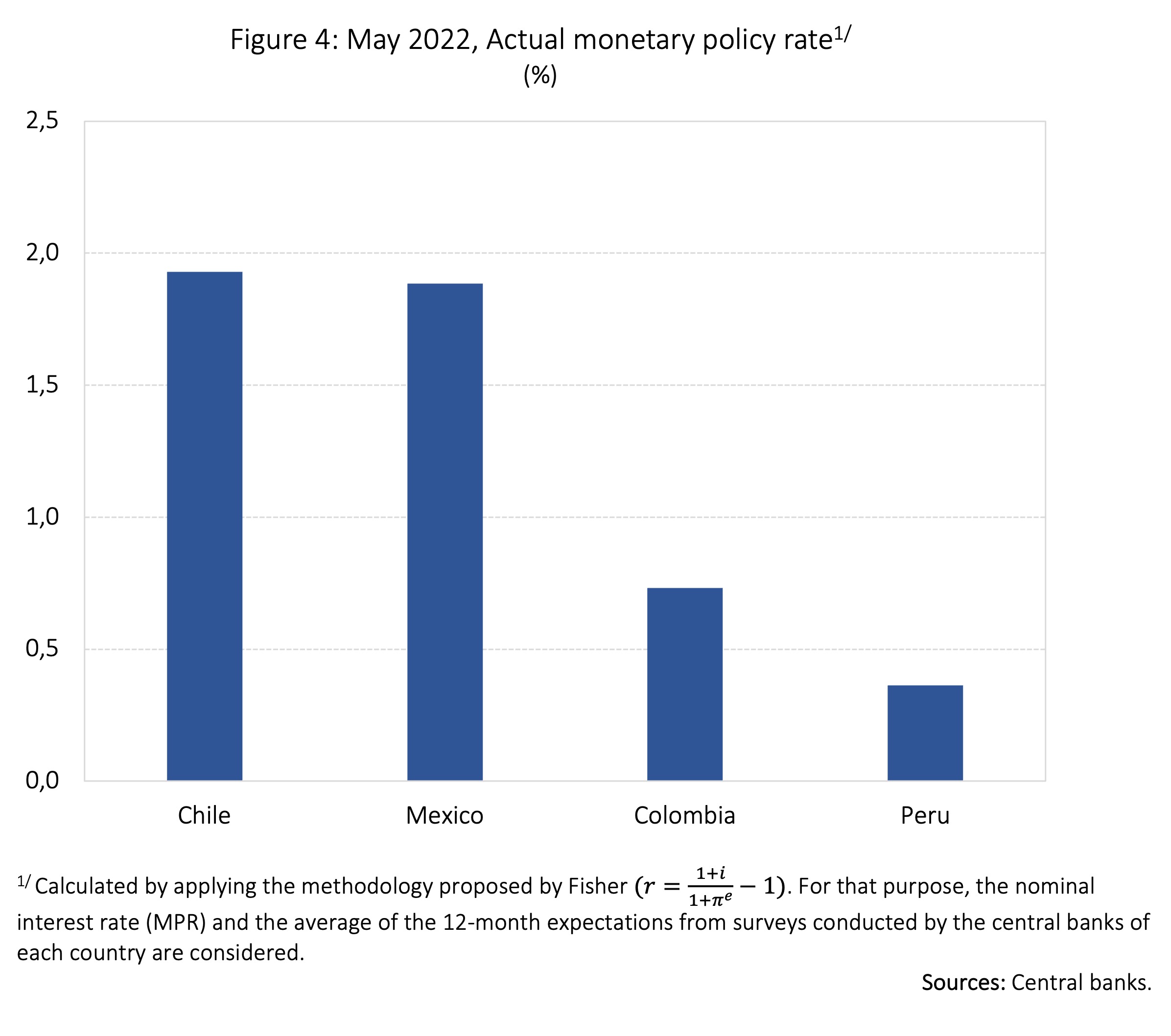

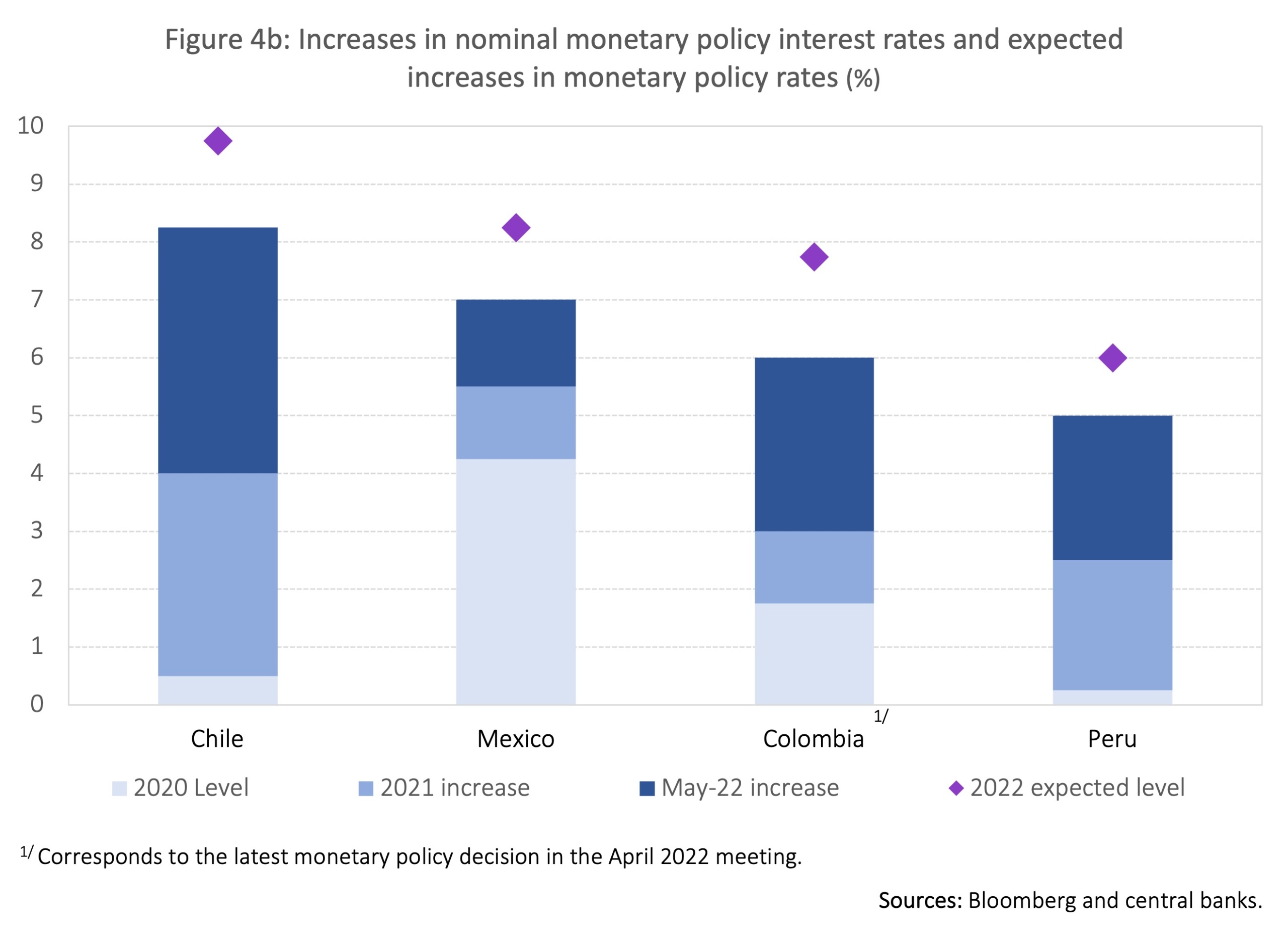

In line with the above, the main indicators of the banking systems of the four countries in question remain at proper levels. In particular, solvency indicators remain above their regulatory levels (Figure 1), portfolio quality indicators also suggest a relatively modest deterioration despite some natural hike throughout the pandemic (Figure 2), and the liquidity of the banking system is adequate (Figure 3) in the context of ample liquidity and low real monetary policy interest rates (Figure 4).

The health of the system prevails even after months of dismantling a significant part of the extraordinary measures implemented during the first stage of the pandemic, which has given way to a new cycle of credit activity. However, the time elapsed after the lifting of these measures is short for a comprehensive evaluation.

Foreseeable risks and challenges are important

Moving forward, the risks and challenges to the stability of the financial system of the four economies analyzed are not fewer than those faced during the pandemic.

External factors include, among others, a stronger and faster than anticipated rise in international interest rates, which may lead to sudden capital outflow episodes and instability in the financial sectors. In particular, the effect may be greater on the financial systems of countries with greater needs for fiscal and external financing.

Since the onset of the pandemic, international monetary policy has been widely flexible in both advanced and emerging economies. However, this is changing due to the pressure emerging from inflation and the tightening of the financial conditions in the United States. Particularly, the Federal Reserve is taking a further tightening stance in recent months, both in terms of its policy rate and its balance sheet.

The war in Ukraine is creating additional pressure on inflation. The persistence or escalation of the war could lead to sudden and unexpected increases in the cost of international and local financing (base rate and risk premium) in a volatile environment in international markets. This, in turn, could lead to further adjustments in access to financing and in economic activity, as well as to the deterioration of local financial markets.

A substantial risk comes from the possible persistence of high and volatile inflation that would put pressure on further interest rate hikes by the central banks, which would in turn affect economic growth. An economic slowdown in the context of increasing financing costs increases financial burdens on households and businesses, impacting financial stability.

An additional idiosyncratic risk comes from the uncertainty that emerges from the effects of social nonconformism due to low growth and job creation, which already existing before the pandemic in most Latin American countries.

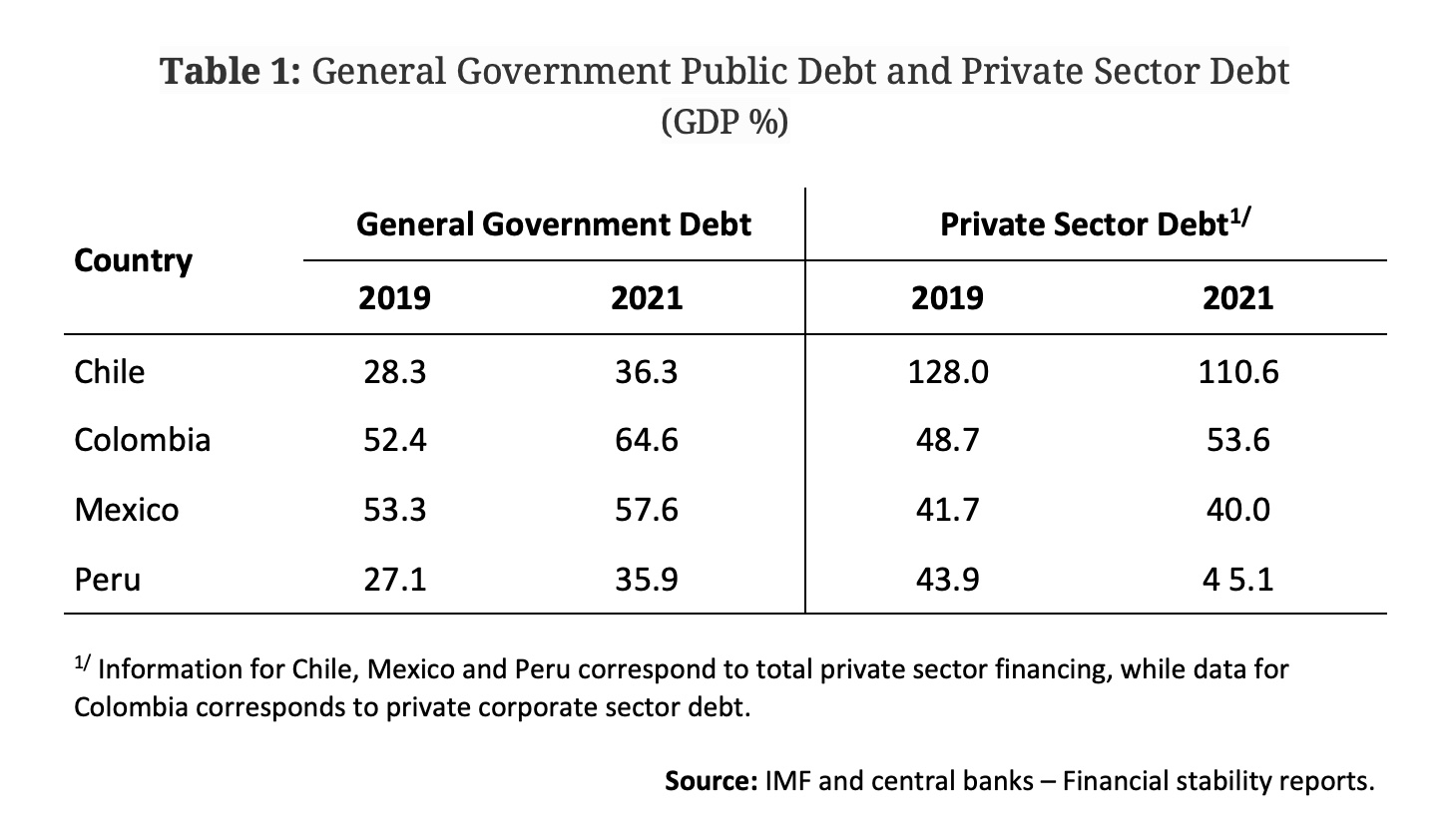

The current credit cycle in the region is based on, a higher than pre-pandemic level of, public indebtedness in every country (Table 1). In some countries, this comes in addition to an increase in private sector indebtedness, as is the case in Colombia and, to a lesser extent, Peru (Table 1). In contrast, private indebtedness has fallen in Chile and Mexico. These two countries, respectively, show the highest and the lowest indebtedness levels as a percentage of GDP within the sample. The need for deleveraging tends to weigh on demand from the most indebted sectors, creating additional risks for economic growth and for banking systems.

In short, the current state of the financial system has shown the results of decades of responsible macroeconomic and financial policy. It is also the result of the characteristics of the shock that has been experienced. The region’s financial systems are preserving their soundness, and credit conditions are still favorable. However, it is no time for self-complacency because changing global and domestic conditions impose challenges and risks to financial stability.