Authors:

Robert Barro, Paul M. Warburg Professor of Economics, Harvard University.

Francesco Bianchi, Louis J. Maccini Professor of Economics and Department Chair Johns Hopkins University.

Carlos Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – cgiraldo@flar.net

Iader Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – igiraldo@flar.net

The COVID-19 pandemic marked a turning point in global macroeconomic dynamics, reviving debates around the fiscal origins of inflation. While inflation had remained subdued in many advanced economies for decades, the massive fiscal responses to the pandemic, combined with supply chain disruptions and commodity price shocks, triggered a sharp and persistent rise in prices. This phenomenon has prompted renewed interest in the fiscal theory of the price level (FTPL), which posits that inflation can emerge from unsustainable fiscal trajectories, particularly when monetary policy accommodates fiscal expansion.

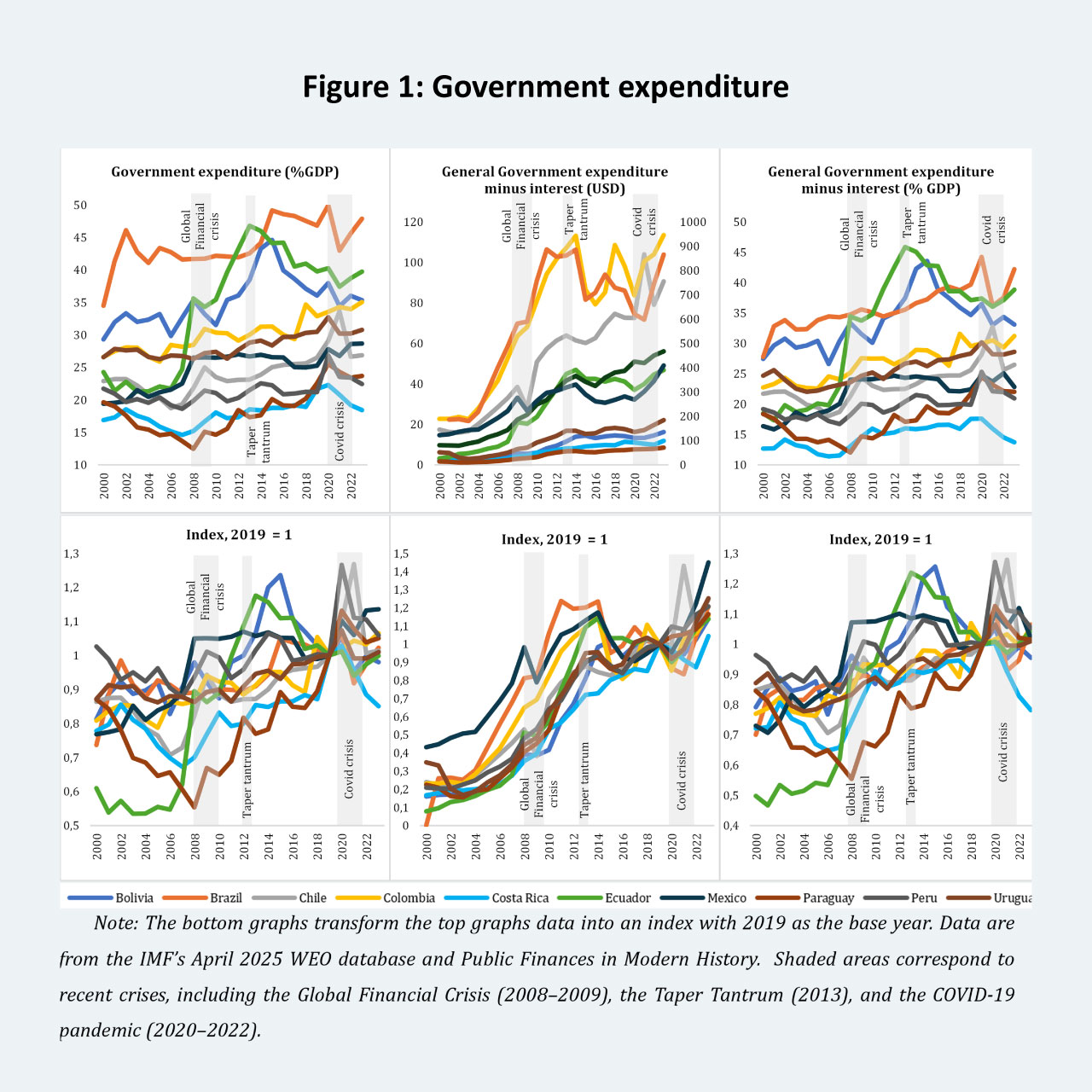

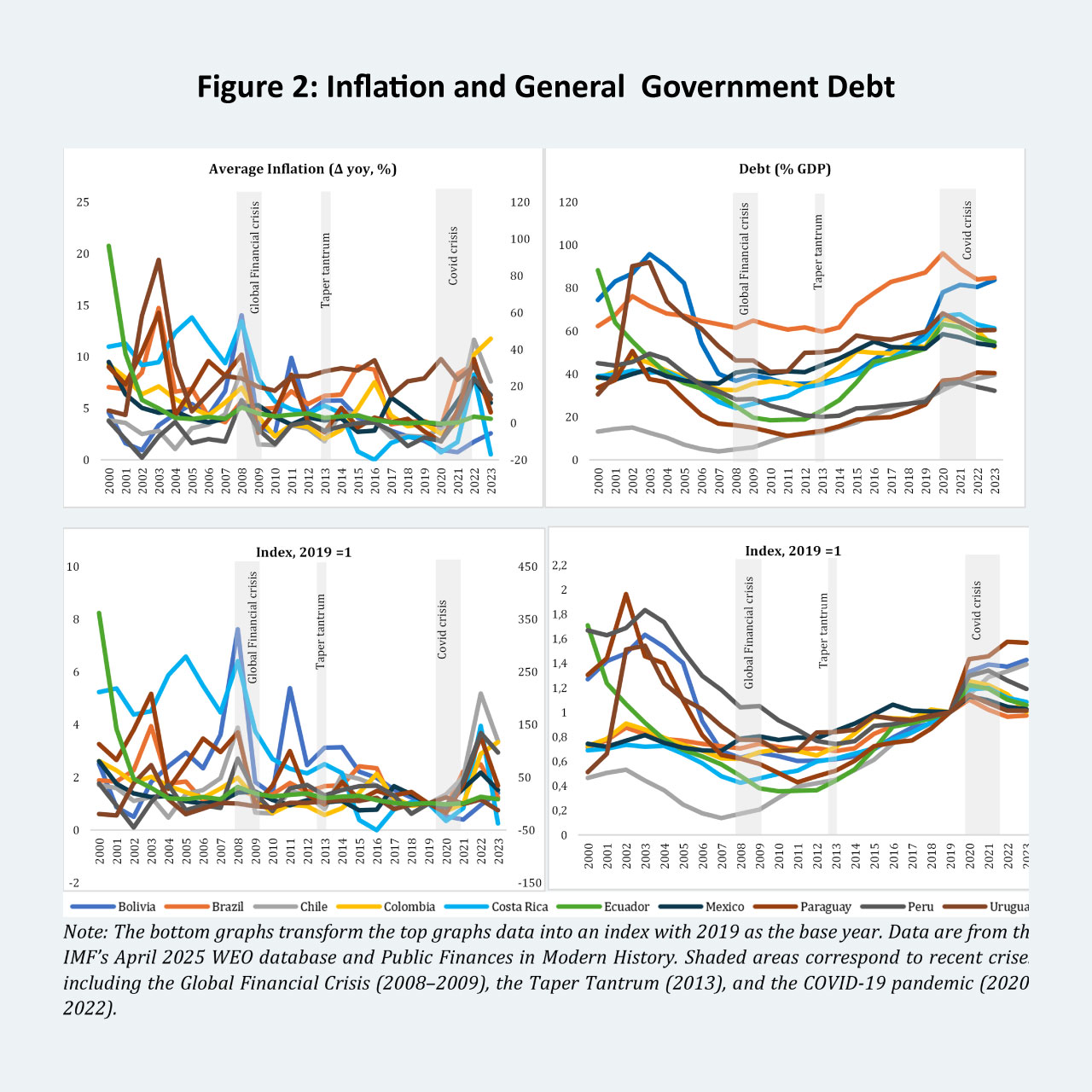

In our recent working paper, Inflation as a Fiscal Phenomenon: Evidence from Latin America, we analyze the effects of fiscal stimulus on inflation across a wider range of Latin American economies. We focus on Bolivia, Brazil, Chile, Colombia, Costa Rica, Ecuador, Mexico, Paraguay, Peru, and Uruguay over the period from 2002 to 2023. Our findings confirm that fiscal policy played a central role in shaping inflation dynamics in the region. The FTPL provides the conceptual foundation for this analysis. According to this theory, the price level adjusts to ensure that the real value of government debt equals the present discounted value of expected future primary surpluses. When governments increase spending without a corresponding plan to raise future revenues or cut expenditures, the resulting fiscal imbalance must be resolved through higher inflation, which erodes the real value of outstanding debt.

In our paper, we present a comprehensive empirical investigation into the inflationary consequences of fiscal expansions in Latin America, focusing on the period from 2020 to 2023, particularly in the post-pandemic context. Our analysis builds on and extends the theoretical framework developed by Barro and Bianchi (2025). To test the predictions of this framework, we employ both cross-sectional and dynamic panel regression techniques. Our cross-sectional regressions are based on the composite spending variable introduced in Barro and Bianchi (2025), which adjusts the size of the fiscal stimulus for the size and maturity of public debt. This approach allows us to isolate the inflationary effects of government spending from other macroeconomic influences and to assess the persistence of these effects over time.

Our baseline cross-sectional regressions reveal a strong and statistically significant relationship between the composite spending variable and both headline and core inflation. These results suggest that countries that undertook larger fiscal expansions experienced more pronounced inflationary pressures. In this respect, our findings are consistent with those reported by Barro and Bianchi (2025). However, our results diverge from Barro and Bianchi (2025) in terms of the role played by outstanding debt and its duration. When these two variables are held constant at their sample means, the model’s explanatory power increases. This suggests that, for the specific subset of Latin American countries considered in our analysis, the size and duration of outstanding debt may play a less prominent role in guiding central bank decisions regarding inflation control.

One possible interpretation is that LATAM countries are more concerned with the reputational consequences of allowing inflation to persist at elevated levels over time. Alternatively, the share of debt denominated in domestic versus foreign currency may be more relevant for these countries than for the broader OECD sample examined by Barro and Bianchi (2025). In both cases, these findings suggest structural differences in how fiscal policy affects inflation across regions. It is therefore worthwhile to investigate whether the strong relationship between inflation and fiscal spending persists in other periods and under different macroeconomic conditions.

To further explore the connection between inflation and spending, we estimate a series of dynamic panel models that incorporate lagged inflation terms, fiscal variables, and a rich set of macroeconomic controls. These models confirm that fiscal expansions have a persistent and positive effect on inflation, even after accounting for real GDP growth, commodity price shocks, and geopolitical disruptions such as the war in Ukraine. Interestingly, we find that real economic activity exerts a negative influence on inflation, suggesting the presence of stagflation dynamics in several countries. Moreover, energy and non-energy commodity prices emerge as significant drivers of inflation, consistent with the structural dependence of Latin American economies on commodity exports.

The key insight from our analysis is that the inflationary impact of fiscal policy in Latin America remains robust even when we do not adjust for debt maturity and size, suggesting an important departure from the findings in OECD countries. This divergence may reflect reputational concerns and historical experiences with inflation in the region, which heighten the sensitivity of inflation expectations to fiscal shocks. In particular, countries with a legacy of debt monetization and limited monetary independence appear more vulnerable to inflationary pressures arising from fiscal expansions.

Taken together, our findings carry several important implications for both fiscal and monetary policy in Latin America. They underscore the need for institutional strengthening, strategic coordination, and enhanced resilience to external shocks to mitigate inflationary risks and promote macroeconomic stability.

First, there is a clear imperative to strengthen fiscal institutions. Anchoring inflation expectations requires governments to commit to credible and transparent fiscal frameworks that ensure long-term sustainability. This involves adopting rules-based fiscal policies, establishing independent fiscal councils, and improving budgetary transparency. Such institutional reforms can enhance fiscal credibility and reduce the likelihood that spending shocks translate into inflationary pressures.

Second, improving debt management practices is essential. Extending the maturity profile of public debt and diversifying the investor base can help reduce the short-term inflationary impact of fiscal expansions. Longer maturities provide governments with more time to adjust to fiscal shocks, while a broader investor base can enhance market confidence and reduce reliance on inflationary financing.

Third, effective coordination between fiscal and monetary authorities is crucial. Central banks must remain vigilant against the risk of fiscal dominance, where monetary policy becomes subordinated to the financing needs of the government. Preserving central bank independence and ensuring clear, consistent communication between institutions are key to maintaining price stability and preventing inflation from becoming entrenched.

Finally, Latin American economies must build greater resilience to external shocks. Given the region’s exposure to volatile commodity prices and global financial conditions, macroeconomic frameworks should incorporate robust buffers. These may include stabilization funds, countercyclical fiscal rules, and flexible exchange rate regimes. Such tools can help absorb external shocks without resorting to inflationary measures, thereby preserving macroeconomic stability in turbulent times.

Taken together, these policy recommendations highlight the importance of institutional quality, strategic foresight, and coordinated action in managing the complex interplay between fiscal policy and inflation in Latin America.

References

Barro, R. J. and F. Bianchi (2025). Fiscal influences on inflation in OECD countries, 2020– 2023. The Economic Journal, ueaf066.