Authors:

Robert Barro, Paul M. Warburg Professor of Economics, Harvard University.

Francesco Bianchi, Louis J. Maccini Professor of Economics and Department Chair Johns Hopkins University.

Carlos Giraldo, Chief economist – FLAR.

Iader Giraldo, Principal economic researcher – FLAR.

Fiscal policy can significantly impact the rate of inflation in Latin American countries. Governments in the region have historically implemented procyclical fiscal policies, increasing spending and borrowing during periods of economic growth and tightening policies during recessions. This approach has contributed to volatility in inflation rates and economic instability. The literature has documented how the tendency of governments in developing countries, including those in Latin America, to engage in expansionary fiscal policies during periods of economic prosperity, has been a major driver of debt crises and macroeconomic volatility in these regions (Kaminsky et al., 2004).

One of the key factors driving this procyclical behavior is the limited fiscal space available to policymakers in emerging and developing countries. When times are favorable and international capital is readily available, governments tend to engage in high spending and borrowing, which can lead to inflationary pressures. During economic downturns, these governments are often forced to implement austerity measures and contractionary fiscal policies, further exacerbating the negative impact on economic growth (Kaminsky et al., 2004). This pattern of fiscal mismanagement has been a recurring theme in the economic history of Latin America, contributing to the region’s “lost decade” due to unsustainable levels of public debt (Lemaire, 2020).

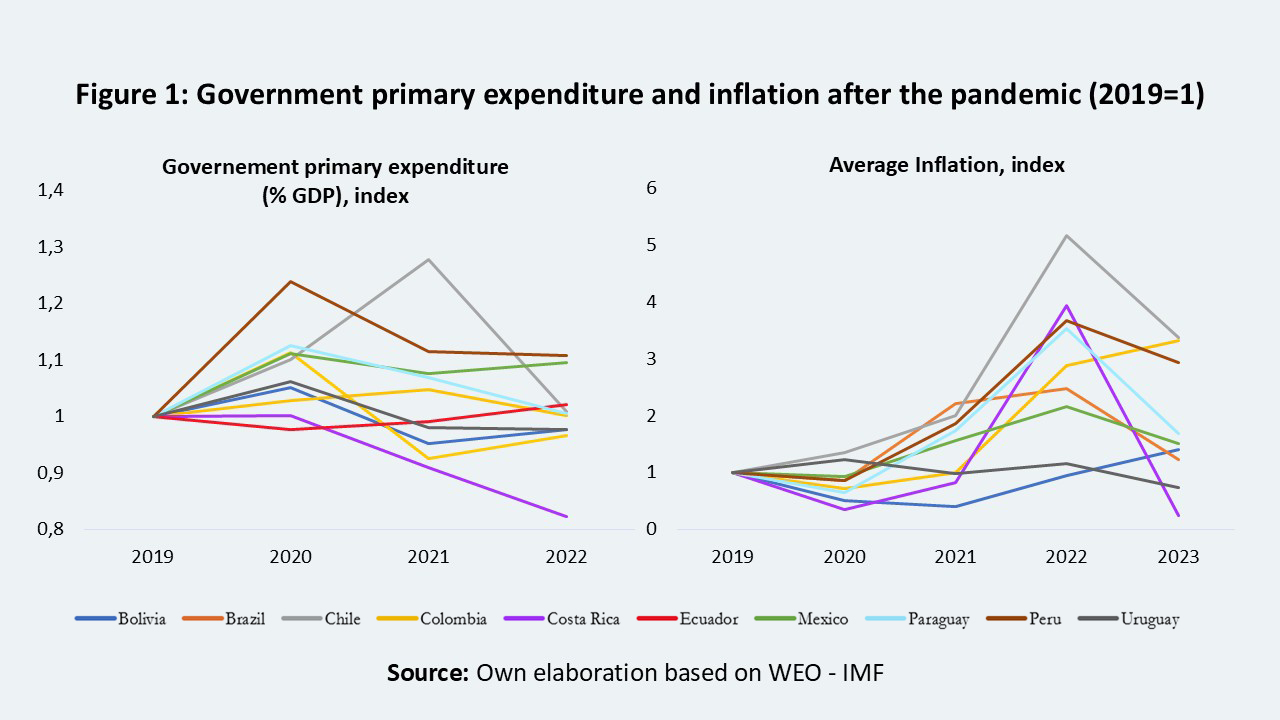

The recent rise in inflation after the COVID-19 crisis calls attention to understanding the impact of fiscal policy on price dynamics in Latin America. Governments in the region have been forced to balance the need for fiscal stimulus to support economic recovery with the risk of fueling inflation (Figure 1). Our current research assesses the interplay between fiscal policy and inflation in selected Latin American countries during the pandemic. Following Barro and Bianchi (2024) and based on the fiscal theory of the price level (FTPL), we analyze the impact of extraordinary COVID-19-related spending and debt on inflation in the region’s economies.

During the COVID-19 pandemic, numerous Latin American countries increased their deficit-financed government spending. This surge in fiscal interventions was generally seen as not being supported by immediate tax hikes or future spending cuts, which, according to the Fiscal Theory of the Price Level (FTPL), can result in rising inflation rates. Our analysis indicates that the fiscal response to the crisis notably impacted inflation in some countries of the region, especially in countries with existing fiscal vulnerabilities.

However, the impact of fiscal policy on inflation in Latin America could extend beyond the COVID-19 crisis. This might be due to the unique dynamics of fiscal policy in the region. Given the procyclical nature of fiscal policy in the region, there have been other specific times when the impact of fiscal policy on inflation was more pronounced, driven by factors such as commodity booms, political cycles, or favorable international environment (Kaminsky et al., 2004).

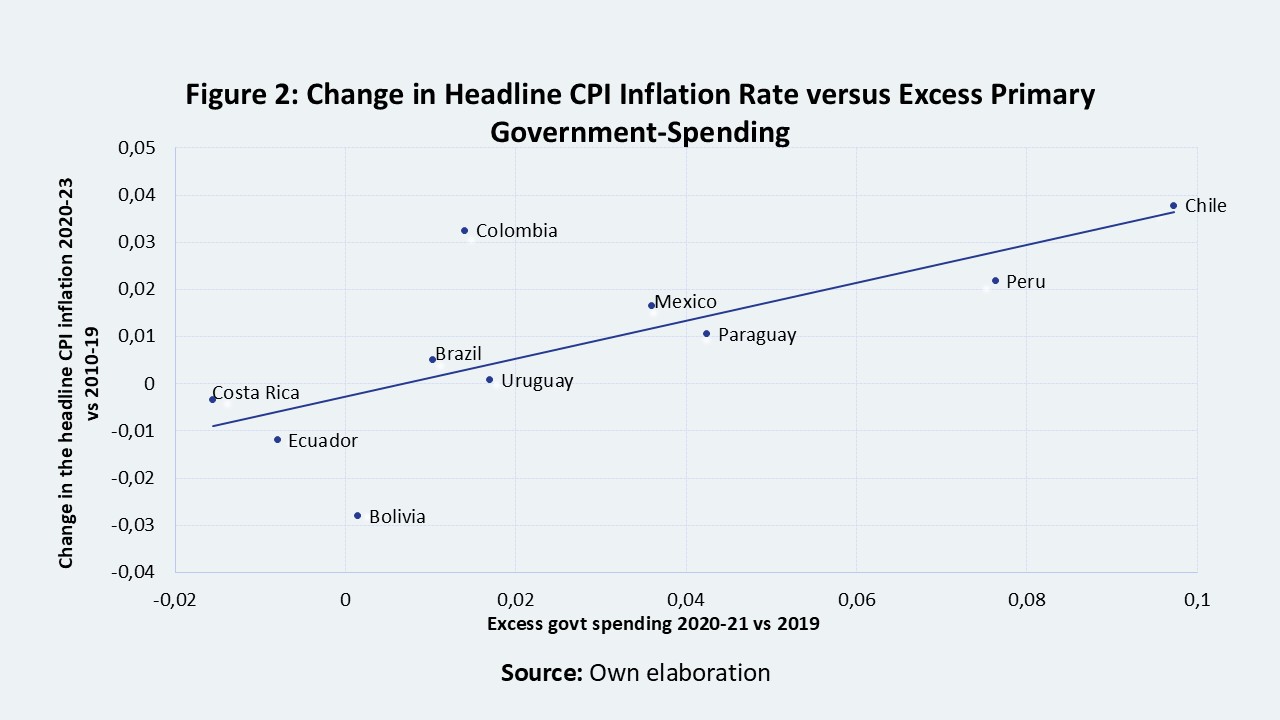

In this sense, our preliminary results show the impact of fiscal policy on inflation levels in some regions’ economies (Figure 2). The fiscal theory of the price level provides a valuable framework for understanding the relationship between fiscal policy and inflation in Latin American countries, though the specific mechanisms and magnitude of this relationship may vary over time. Additionally, it highlights the importance of fiscal discipline and the need for countercyclical fiscal policies to mitigate the inflationary impact of government spending and borrowing. A sound fiscal approach meant to avoid spurs of inflation would require building fiscal space during expansions.

A consistent policy mix combining fiscal prudence and monetary consolidation could be crucial for tackling inflation and ensuring sustainable economic growth in Latin American countries in the near future. Implementing a balanced approach that incorporates both fiscal discipline and clear monetary policies can be instrumental in addressing the region’s inflationary challenges and promoting long-term economic stability. This coordinated effort between fiscal and monetary authorities can help Latin American economies navigate the current economic environment and position them for sustained equitable development.

Policymakers in the region must carefully balance fiscal discipline with the need to support economic growth and address inflationary pressures. They should understand the importance of financial stability and sound public finances in achieving macroeconomic stability and reducing the impact of crises. By adopting a more countercyclical approach to fiscal policy, Latin American countries can better insulate their economies from external shocks and promote structural policies to drive economic growth.

References

Barro, R. J., & Bianchi, F. (2024). Fiscal Influences on Inflation in OECD Countries, 2020-2023. NBER Working Paper.

Kaminsky, G., Reinhart, C., and Végh, C. (2004). When it Rains, it Pours: Procyclical Capital Flows and Macroeconomic Policies. National Bureau of Economic Research – Macroeconomics Annual 2004, Volume 19. https://doi.org/10.3386/w10780

Lemaire, T. (2020). Fiscal Consolidations and Informality in Latin America and the Caribbean. In T. Lemaire, SSRN Electronic Journal. RELX Group (Netherlands). https://doi.org/10.2139/ssrn.3581672