Authors:

Carlos Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – cgiraldo@flar.net

Iader Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – igiraldo@flar.net

José E. Gómez-González, Department of Finance, Information Systems, and Economics, City University of New York – Lehman College, Bronx, NY, 10468, USA. Email: – jose.gomezgonzalez@lehman.cuny.edu

Jorge M. Uribe, Serra Húnter Fellow, Faculty of Economics and Business and IREA-Riskcenter, Universitat de Barcelona (UB), Barcelona, Spain, Email: – jorge.uribe@ub.edu

The relationship between government expenditure and financial stability is complex. Fiscal expenditure, when carefully designed and implemented, can stabilize financial systems, while poorly planned or unsustainable expenditure may lead to financial instability. At its core, the impact of government spending on financial stability depends on three key factors: the scale and structure of expenditures, their allocation across sectors, and the sustainability of fiscal policies (Borio et al., 2023).

As highlighted by Panizza and Presbitero (2014) the adverse impact of public debt on economic outcomes (among which we could include financial stability) could be more pronounced if it diminishes the efficiency of public expenditures, heightens uncertainty, or fosters expectations of future financial repression. Additionally, increased sovereign risk can raise real interest rates, thereby reducing private investment. All these aspects of public debt and spending risk make a country’s financial system more vulnerable to systemic shocks.

Furthermore, the interplay between the banking sector and public finances underscores the critical role of fiscal policy in maintaining financial stability. Banks are primary lenders to governments, and governments often act as the ultimate backstop for the financial system during times of financial distress. This creates a feedback loop where instability in the banking sector can exacerbate fiscal risks, and fiscal weaknesses can, in turn, destabilize the financial system (Reinhart and Rogoff, 2009). A strong fiscal position is necessary for governments to mitigate financial instability, even in the absence of direct public sector borrowing crises. By having sufficient fiscal space, governments can break the cycle of financial contagion and reduce the likelihood of a financial crisis. This fiscal flexibility is vital for enabling government support in times of crisis, such as through lender-of-last-resort interventions or direct assistance to struggling banks (Laeven and Valencia, 2018).

The relationship between increased R&D expenditure and the resilience of the financial system to macroeconomic shocks—i.e., financial stability—has received surprisingly little attention in the literatures on innovation, economics, or finance. This oversight is notable because higher levels of spending on R&D are expected to enhance financial stability by fostering sustained growth, increased productivity, and improved export quality. Conversely, public R&D expenditure, as part of total government expenditure, could undermine financial resilience by contributing to unsustainable debt levels, widening spreads, and increasing the risk of sovereign default. Thus, the relationship between the two variables is not obvious.

While the effects of different investment styles (e.g., value versus growth) on the level of corporate R&D have been explored in the literature (e.g., Sayili et al., 2017), research examining the impact of R&D on financial stability remains scarce.

In our most recent research, which will be published in the coming days, we examine the relationship between a country’s level of investment in research and development (R&D) and financial stability. We provide the first empirical assessment of this relationship, focusing specifically on the effects of expenditure on R&D activities and its impact on financial stability. This question is particularly critical given the short- and medium-term tensions between reducing government spending to promote immediate financial stability and maintaining robust long-term growth and productivity prospects, which are also crucial for future macroeconomic performance.

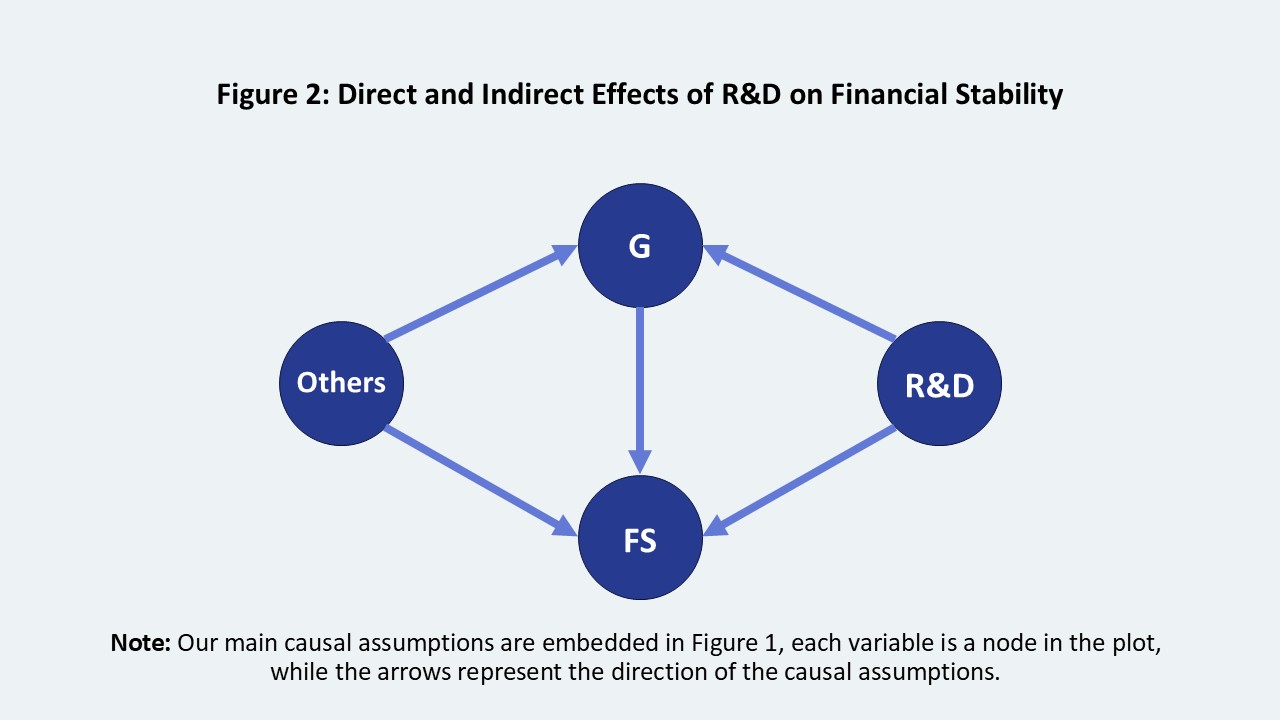

Using causal mediation analysis (Figure 2), with data from 2000 to 2022, covering 44 countries1, we evaluate both the direct impact of R&D spending on financial stability and the indirect effects mediated through government expenditure. We found that while total R&D spending, including public and private contributions, directly and significantly enhances financial stability, an increase in total public expenditure—arising from higher R&D investment while holding other components of government spending constant—counterbalances this positive effect. Thus, when both direct and indirect pathways are considered, the overall causal impact is insignificant.

Our findings emphasize the importance of a balanced fiscal strategy that reconciles the urgency of short-term fiscal consolidation with the pursuit of long-term economic growth and productivity. Namely, these findings highlight the need for policymakers to prioritize R&D investment while carefully managing other areas of public spending to safeguard financial stability.

They also underscore the critical role of private R&D investment for financial stability. A strategic fiscal framework is essential to balance innovation-driven investments with fiscal discipline, supporting long-term economic resilience and growth.

Our contribution is relevant in the current context, where in many countries, fiscal rules have either been suspended or their enforcement delayed, facilitating the stabilization of macroeconomic and social conditions. Although fiscal sustainability is widely recognized as a cornerstone of macroeconomic stability, there is ongoing debate about the most effective strategies to achieve it. Traditional approaches often emphasize the importance of containing government expenditure to prevent fiscal imbalances from reaching unsustainable levels.

However, emerging research challenges this perspective underscoring the pivotal role of institutional strength and economic structure in shaping a country’s fiscal outlook and recognizing that the composition of public spending may be more critical than its overall level.

Overall, the results highlight the importance of expenditure-neutral fiscal policies. Increasing R&D spending without accompanying reductions in other areas can exacerbate fiscal imbalances and undermine financial stability. In summary, our findings suggest that the effectiveness of R&D investment in promoting financial stability depends on maintaining fiscal discipline.

References

Borio, C. E., Farag, M., & Zampolli, F. (2023). Tackling the fiscal policy-financial stability nexus. Bank for International Settlements, Monetary and Economic Department.

Laeven, L., & Valencia, F. (2018). Systemic banking crises revisited. IMF WP/18/206, International Monetary Fund.

Panizza, U., & Presbitero, A. F. (2014). Public debt and economic growth: is there a causal effect?. Journal of Macroeconomics, 41, 21-41.

Reinhart, C. M., & Rogoff, K. S. (2009). The aftermath of financial crises. American Economic Review, 99(2), 466-472.

Sayili, K., Yilmaz, G., Dyer, D., & Küllü, A. M. (2017). Style investing and firm innovation. Journal of Financial Stability, 32, 17-29.