Authors 1/:

Carlos Giraldo, Director of Economic Studies – FLAR – cgiraldo@flar.net

Iader Giraldo, Principal Economic Researcher – FLAR – igiraldo@flar.net

Liz Villegas, Professional Economist – FLAR – lvillegas@flar.net

To date, in 2024, the economy of Latin America has continued its macroeconomic adjustment process; the GDP growth is lower than that in 2023, which is accompanied by a decline in the current account deficit of the balance of payments and inflation1. Similarly, in the context of tighter international financial conditions, the fiscal sector is characterized by higher public debt than that observed during the pre-pandemic period.

Both external and internal factors explain the lower level of economic activity. On the external side, total goods exports grow at low rates and heterogeneously among the region’s economies2, despite their recovery from the levels presented in 2023. The latter is linked to the resilience of global economic activity, particularly in the economies of the United States and China, which are growing at rates close to those observed during the second half of 2023.

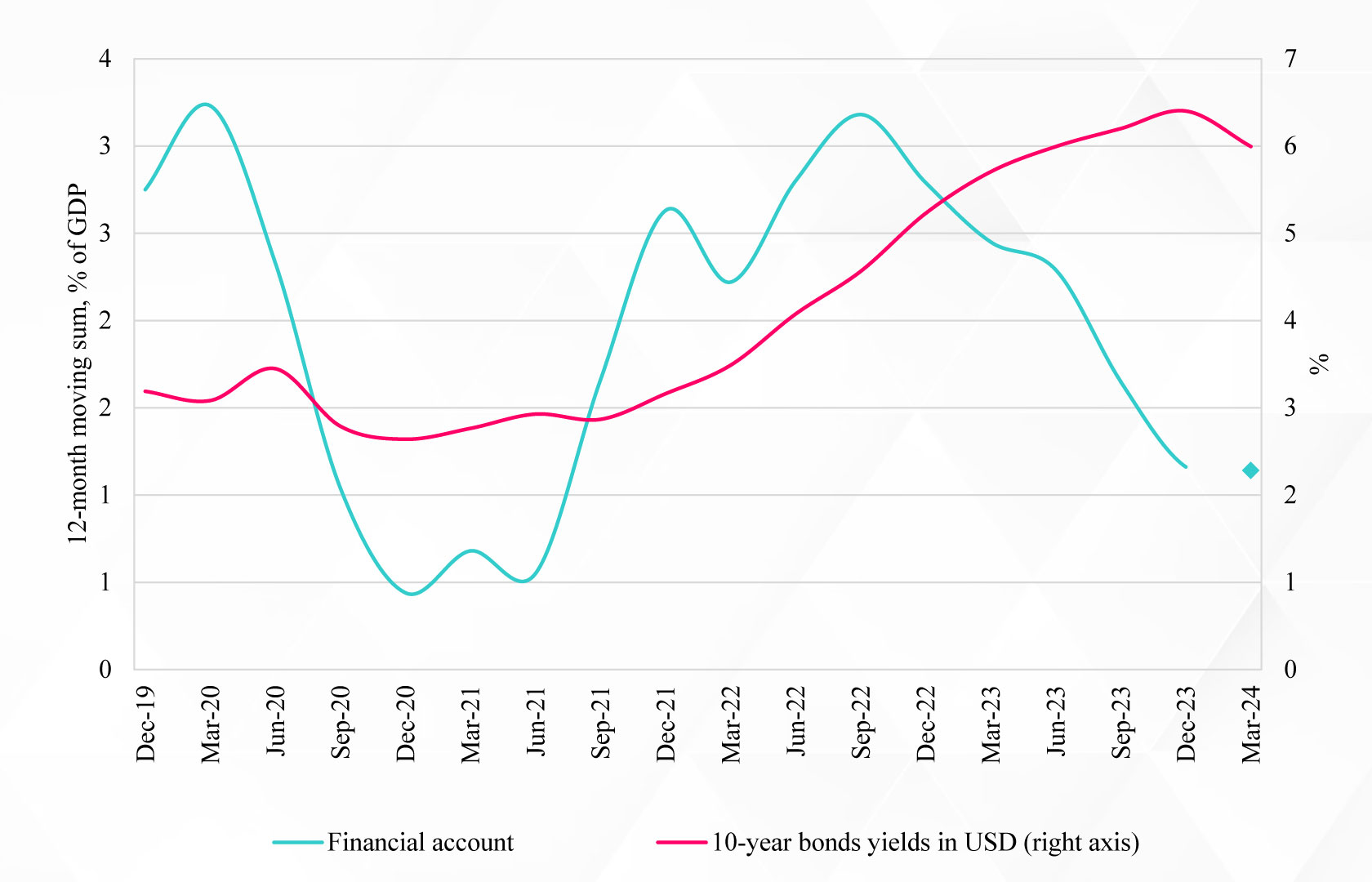

International financial conditions are tighter, resulting in higher costs and lower financing flows to the region, as indicated by the evolution of the financial account of the balance of payments (Figure 1). Similarly, the frequency of sovereign bond issuance is decreasing this year.

Chart 1: Financial account and yield on 10-year bonds1/ (%)

1/ Financial account grouped by GDP in USD PPP. With data as of Apr 24 for Brazil, Chile, Costa Rica, Mexico, Paraguay, and Uruguay.

Source: Own calculations based on information from central banks and Bloomberg.

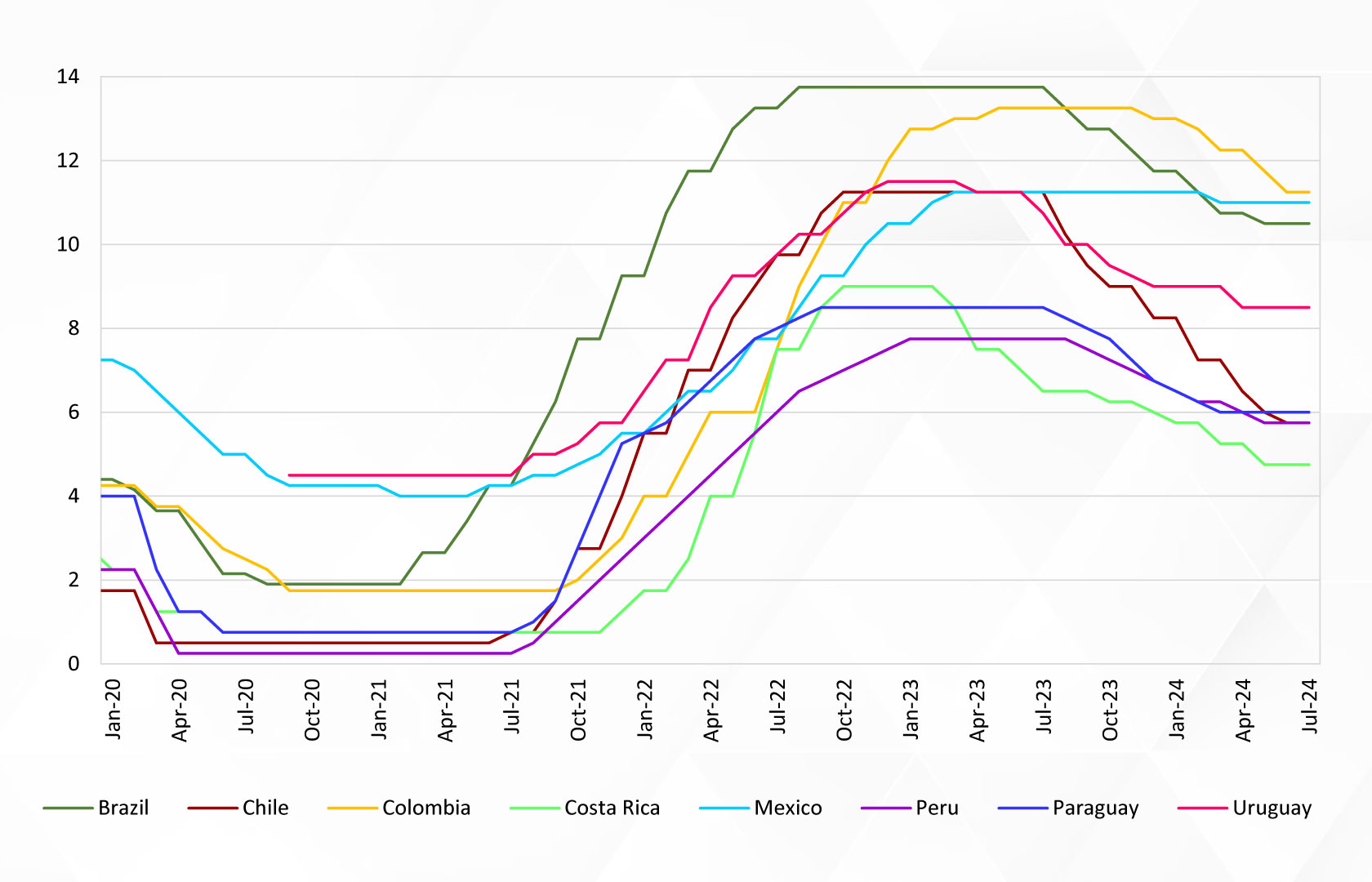

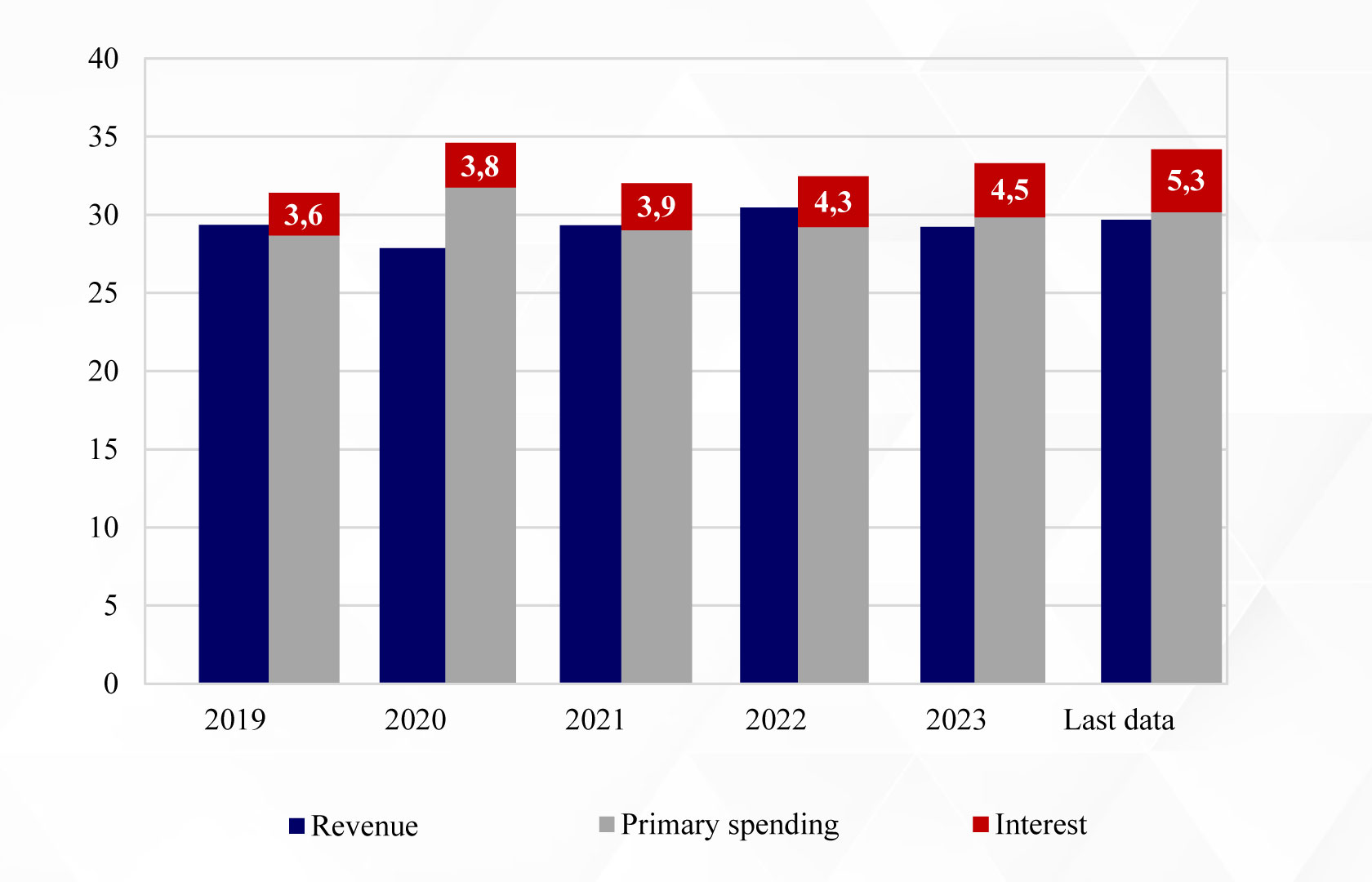

On the domestic side, several factors are contributing to the economic slowdown in the region, with different magnitudes, depending on the country analyzed. These factors include the high level of monetary policy rates, which is justified by the need to control inflation (Figure 2), and limited fiscal capacity. The latter is inherited from the response of governments to the pandemic and placed under pressure by the strong growth in interest payments (more than 5% of the GDP) (Figure 3). Public debt as a percentage of the GDP has maintained an upward trend and stands above 60%.

Graph 2: Monetary policy rate 1/ (%)

1/ The rates for July are those in force on 3 July.

Source: Own calculations based on information from central banks.

Graph 3: Fiscal revenues and expenditures1/ (12-month rolling sum, % of GDP)

1/ Consider Brazil, Bolivia, Chile, Colombia, Costa Rica, Ecuador, Mexico, Peru, Paraguay and Uruguay. They are grouped by GDP in USD PPP.

Source: Own calculations based on information from ministries of finance or finance.

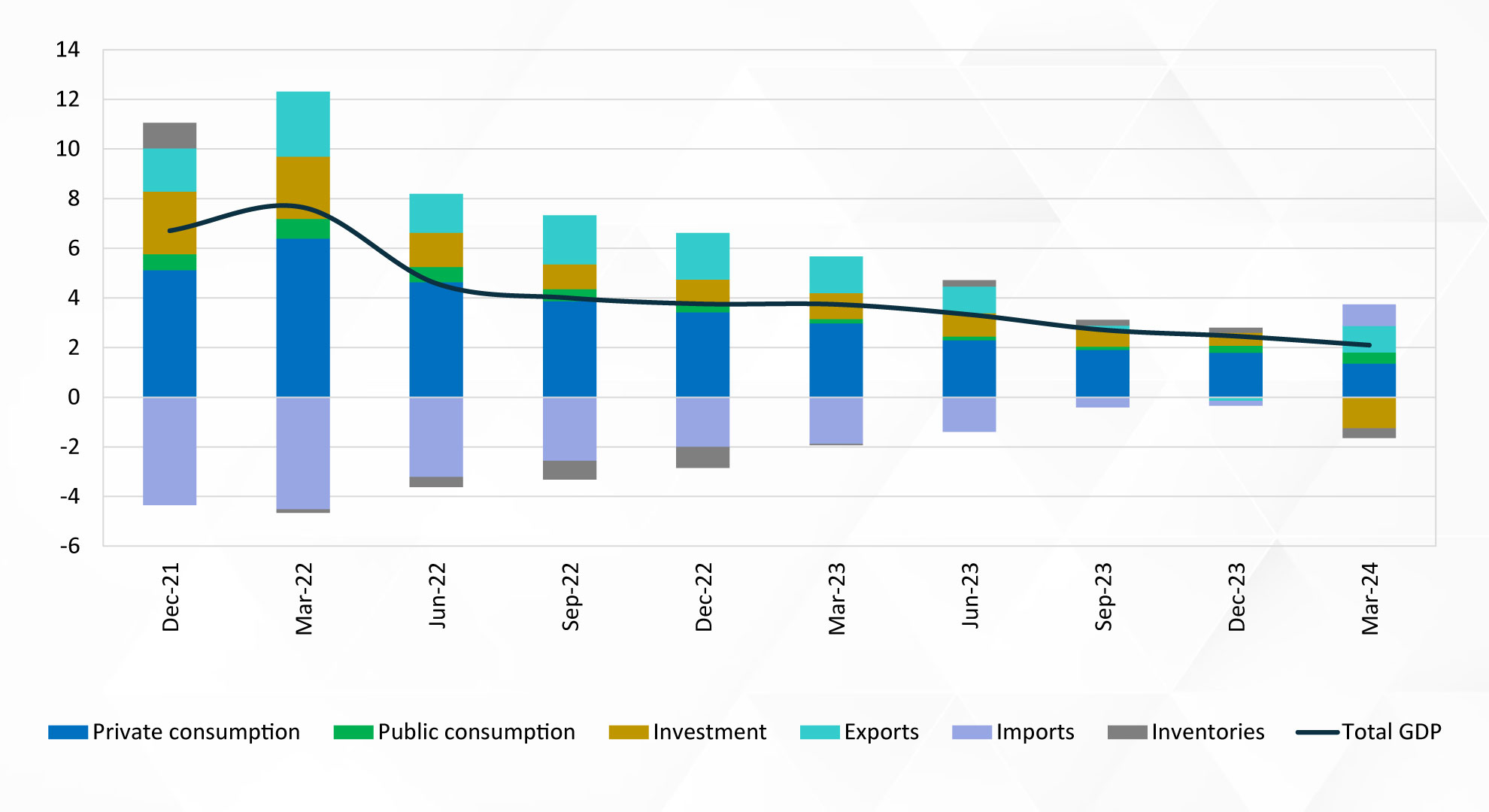

The region’s lower level of economic growth is characterized by a significant slowdown in investment (gross fixed capital formation—GFKF) (Figure 4), which has occurred in the context of high interest rates and political and economic uncertainty in several economies.

Figure 4: Contribution to GDP growth in Latin America1/ (Annual variance – year-to-date, percentage points)

1/ Consider Brazil, Bolivia, Chile, Colombia, Costa Rica, Ecuador, Mexico, Peru, Paraguay and Uruguay. Grouped by GDP in USD PPP.

Source: Own calculations based on information from central banks.

Consumer inflation has continued to decrease; however, it has not yet reached its target level or range in some countries (e.g., Colombia, Mexico, and Chile). The aggregate indicators of banking systems remain strong despite higher interest rates and a slowdown in credit. While portfolio nonperforming loans continue to increase in several economies, they do not currently present worrying levels.

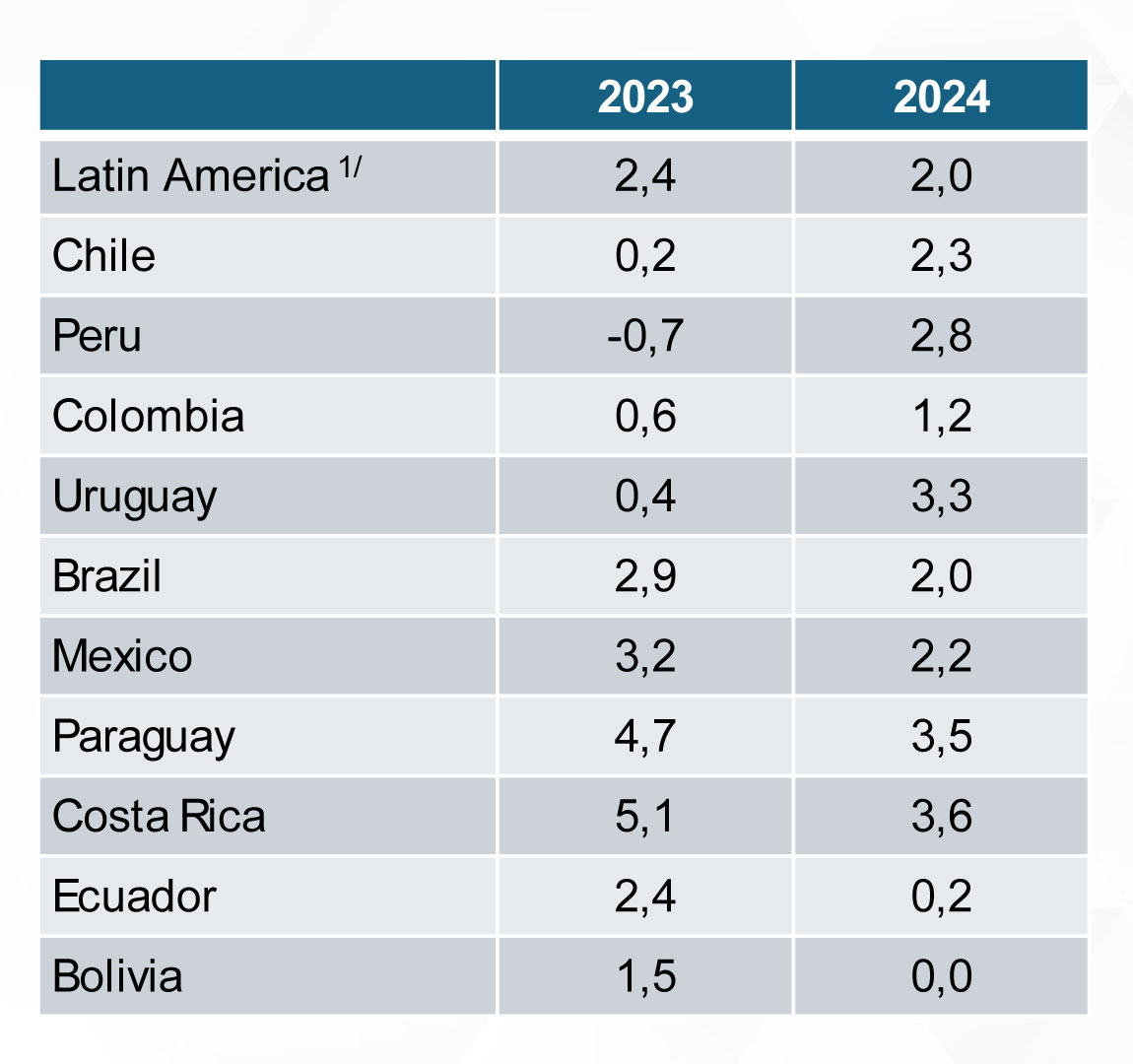

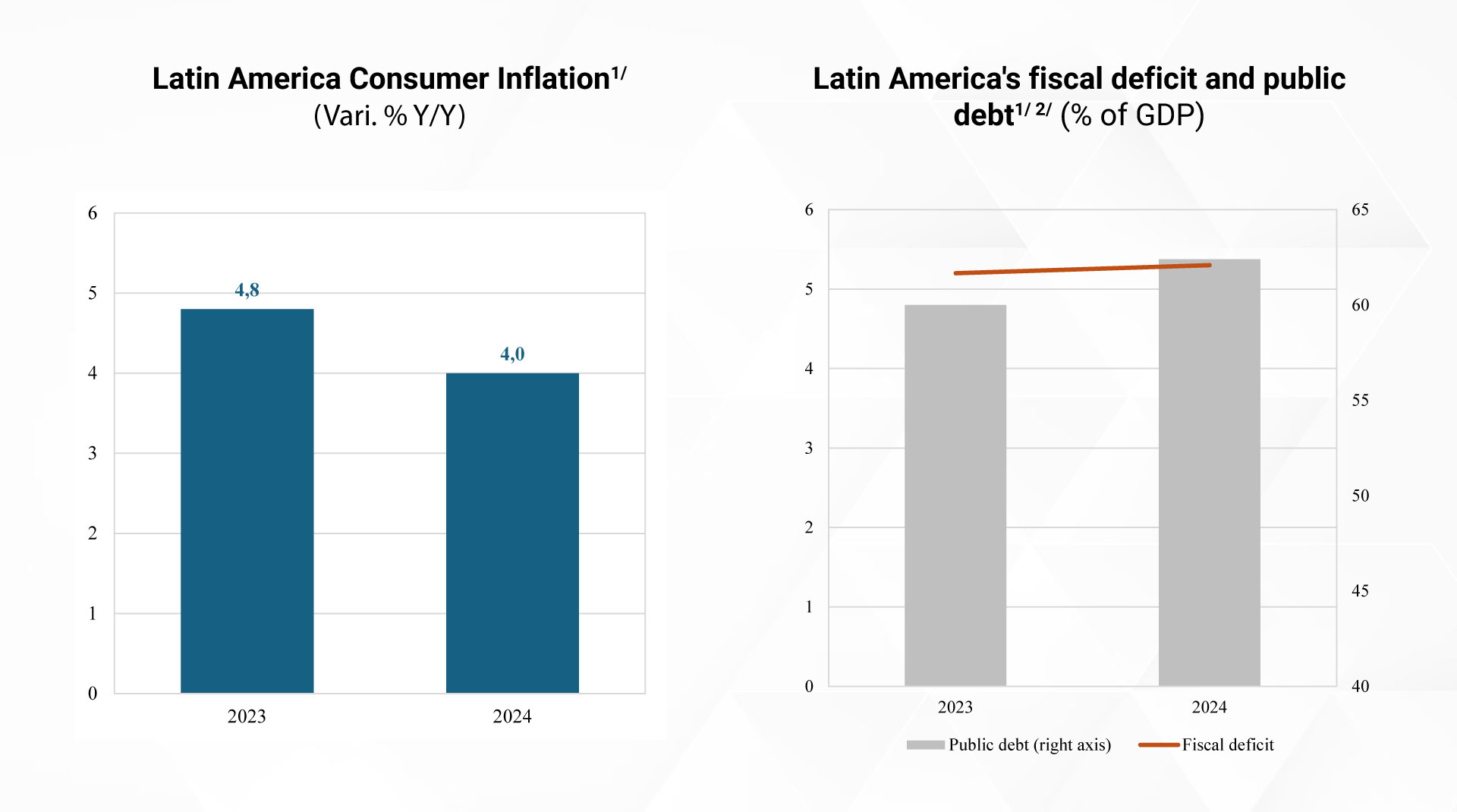

In the short term, the region is expected to continue its macroeconomic adjustment with a GDP growth of 2% (Table 1), although with heterogeneities evident between economies. Compared with their growth in 2023, Chile, Peru, Colombia, and Uruguay are expected to grow more in the current year. Inflation will continue to decline and come within the target range (or tolerance) for most central banks, reaching target inflation in the coming months (Figure 5).

Table 1: Estimates of real GDP growth in Latin America (% annual change)

Figure 5: Estimates of consumer inflation, fiscal deficit, and public debt in Latin America

1/ Latin America includes Bolivia, Brazil, Chile, Colombia, Costa Rica, Ecuador, Mexico, Peru, Paraguay, and Uruguay. It is grouped by GDP in USD PPP.

2/ Fiscal sector coverage by country: BO: NFPS; CH: central government; CO: national central government; CR: central government; CE: NFPS; PY: central administration; EP: NFPS; and UY: SPNM.

Source: Own calculations. Directorate of Economic Studies – FLAR.

The balance of risks is relatively stable. Upside risks include a higher level of resilience in global economic activity and an increase in investment and external financing flows to the region. On the other hand, a more prolonged tightening of global financial conditions and a deterioration in confidence in political, economic, and social sustainability in several key regional countries represent the main downside risks.

Among the priorities and challenges of short-term macroeconomic policy is determining the gradualness and magnitude of the reduction in interest rates to guarantee macroeconomic stability, i.e., keeping inflation under control and not generating capital outflows in the context of high interest rates from the Federal Reserve of the United States, while not creating problems in the financial stability of companies, households, or the government and maintaining confidence in political, economic, and social sustainability. For this purpose, it is essential to achieve or preserve fiscal sustainability.

In summary, the Latin American economy continues to evolve in its cyclical adjustment according to the particularities of each country. The moderate level of growth with lower current account deficits and inflation levels converging to their targets reflects the resilience of most of the region’s economies. However, risks persist, and economic authorities must continue with their efforts to contain inflation and consolidate public finances in various countries, as well as to monitor different variables to preserve macroeconomic and financial stability.

1 We appreciate the excellent assistance and support of Daniel García, consultant – FLAR.

2 Growth was led by South American exports, especially from Brazil, Chile, Ecuador, Mexico, Peru and Paraguay.