Authors1:

Christian Alcarraz, FLAR, Bogotá, Colombia. – calcarraz@flar.net

Carlos Giraldo, FLAR, Bogotá, Colombia. – cgiraldo@flar.net

Andrea Villarreal, FLAR, Bogotá, Colombia. – avillarreal@flar.net

Liz Villegas , FLAR, Bogotá, Colombia. – lvillegas@flar.net

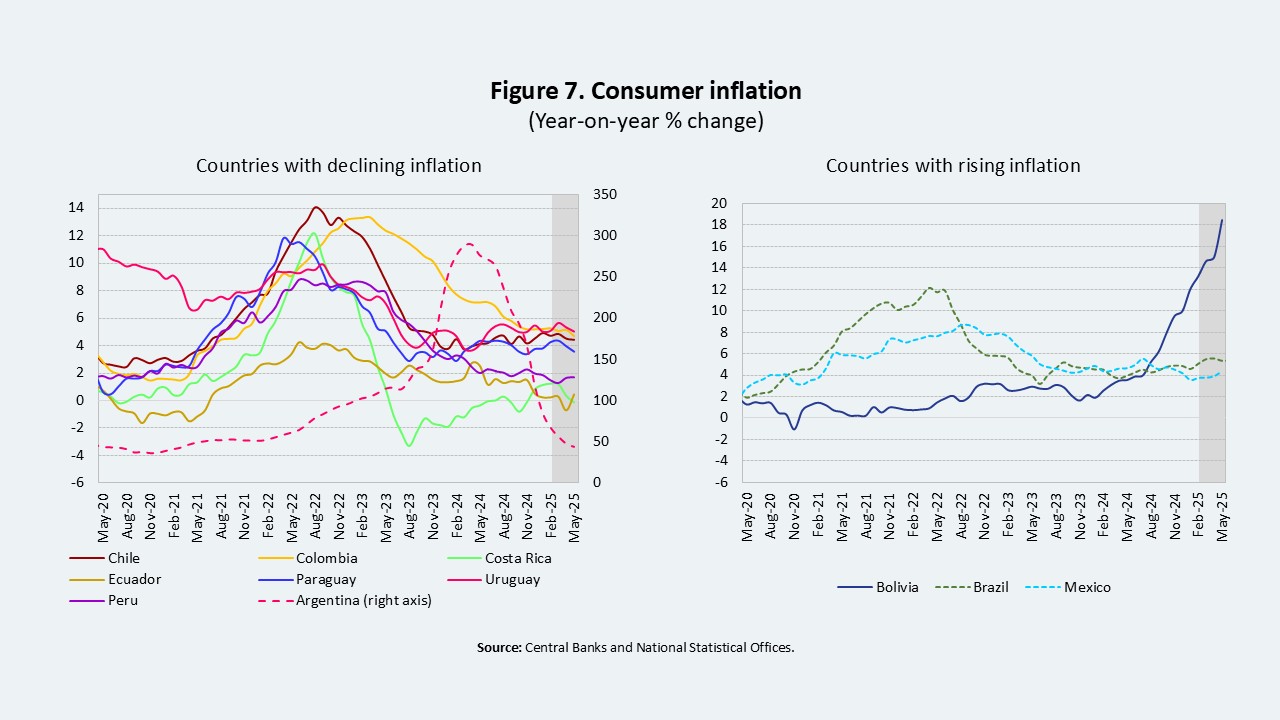

In the early months of the year, most economies in the region have shown resilience despite a highly uncertain international environment, characterized by falling commodity prices and rising geopolitical and trade risks. Several economies have experienced a slowdown in real GDP growth and a continuation of the disinflation process, with significant differences across countries. In this context, external financing flows to the region have remained stable.

Looking ahead, countries face different economic risks shaped by a highly uncertain global environment and by their varying capacities for monetary and fiscal policy responses.

Recent External Shocks: Uncertainty, Commodity Prices, and Financing Flows

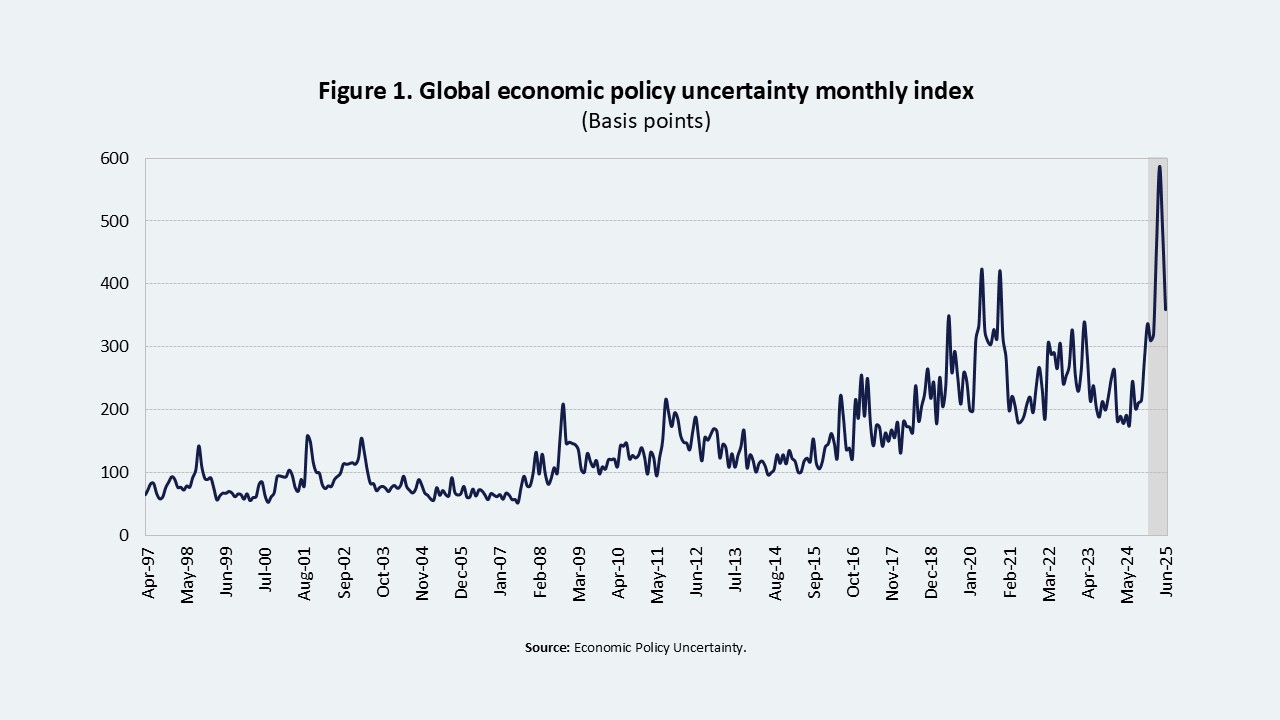

Global economic policy uncertainty has risen to historical levels due to increasing trade tensions (Figure 1). Although the peak in uncertainty was recorded following the announcement of broad-based tariff measures by the administration of Donald Trump (Liberation Day), its subsequent decline has been slow, remaining at elevated levels compared with 2024.

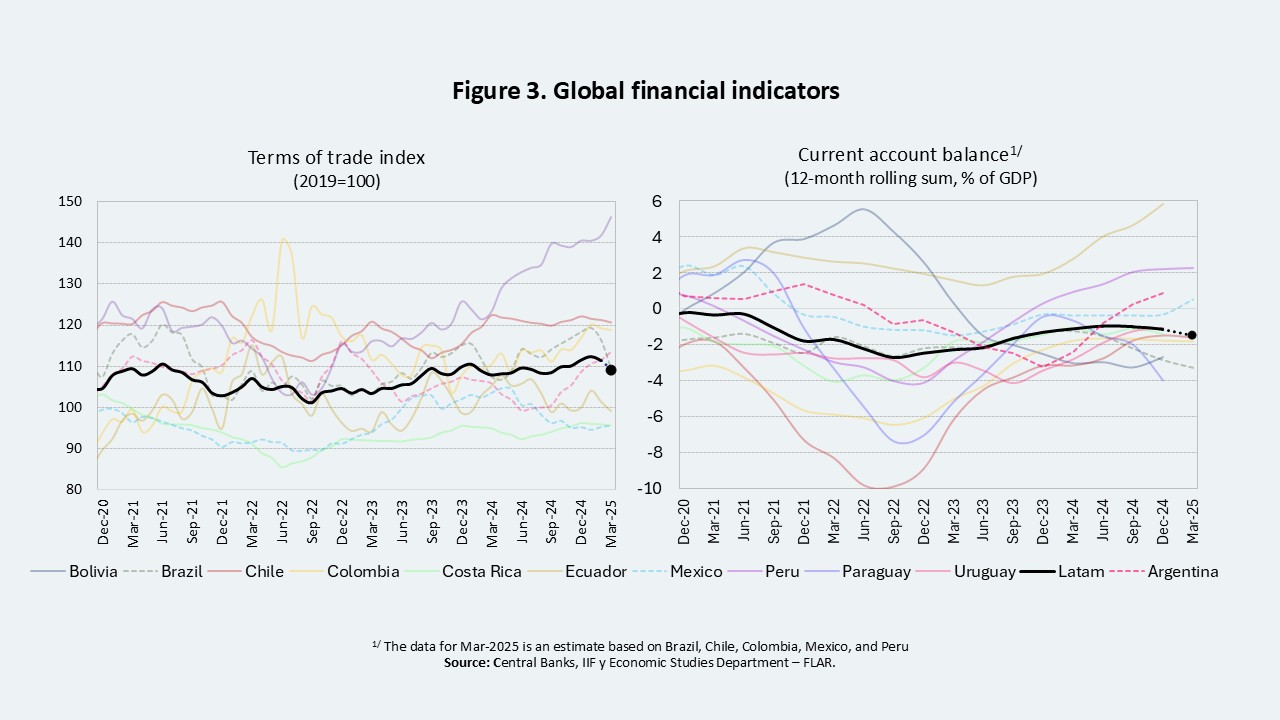

Given the prevailing global conditions, preliminary balance of payments data for the first quarter of 2025 suggest that capital flows to Latin America have remained relatively stable and may even have increased as a share of GDP in several economies.

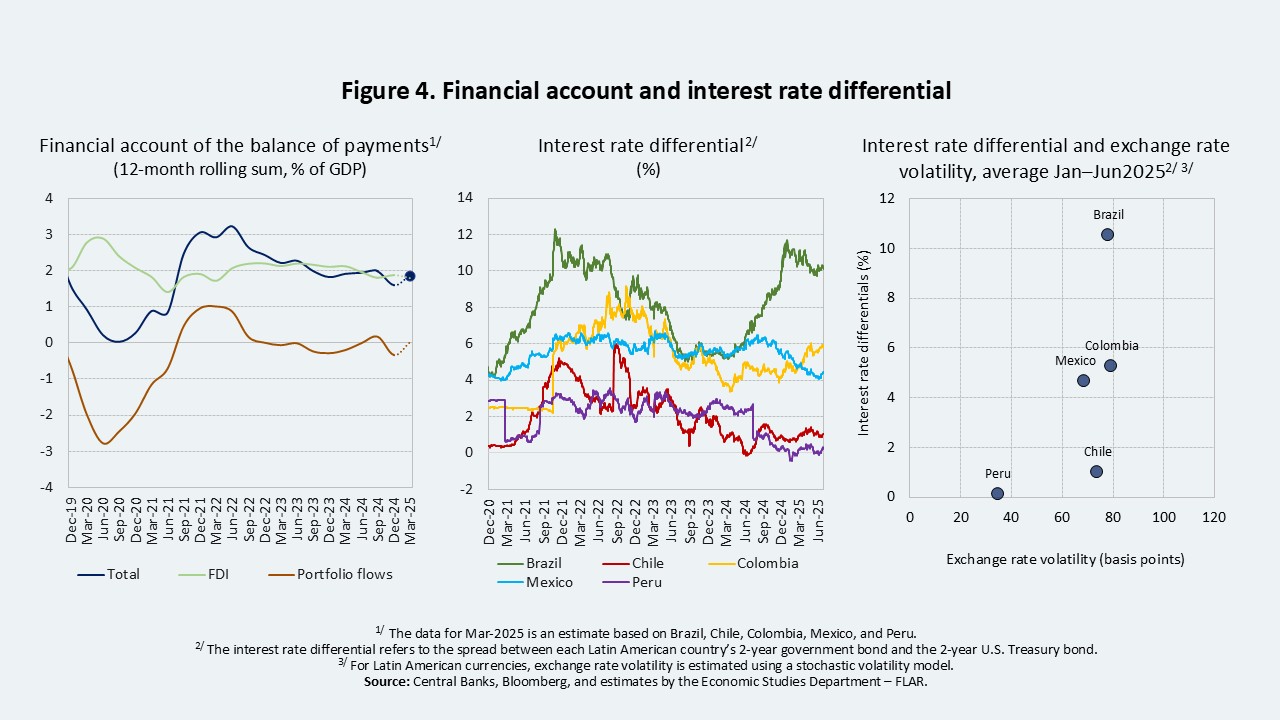

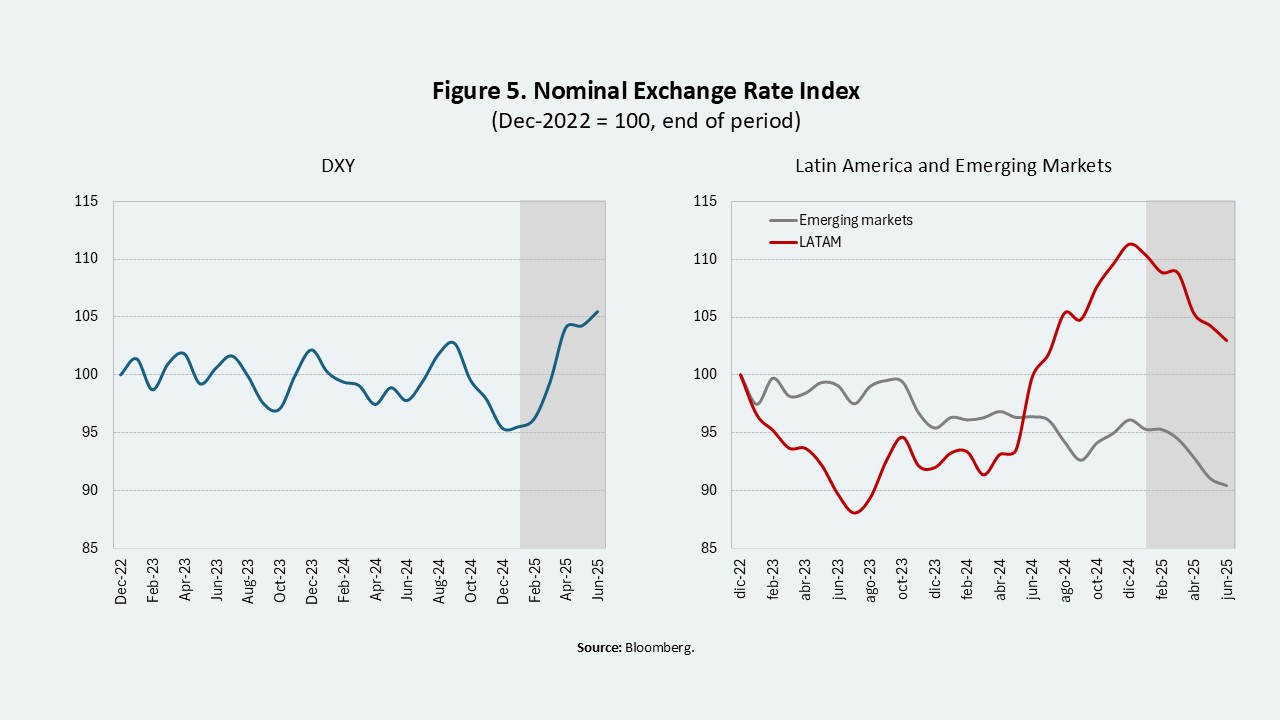

Capital inflows have been predominantly driven by portfolio flows. On the one hand, this may reflect the fact that the interest rate differential relative to dollar,. partly because interest rate differentials relative to dollar-denominated investments remains attractive for carry trade operations, particularly in countries such as Brazil and Colombia (Figure 4). At the same time, the United States has become the epicenter of global uncertainty—due to the trade war and widening fiscal imbalances—weakening the dollar and encouraging investors to diversify into emerging markets, including those in Latin America. This has contributed to the appreciation of most regional currencies (Figure 5).

Growth shaped by external and domestic factors, a gradual disinflation path, and heterogeneous monetary policy responses

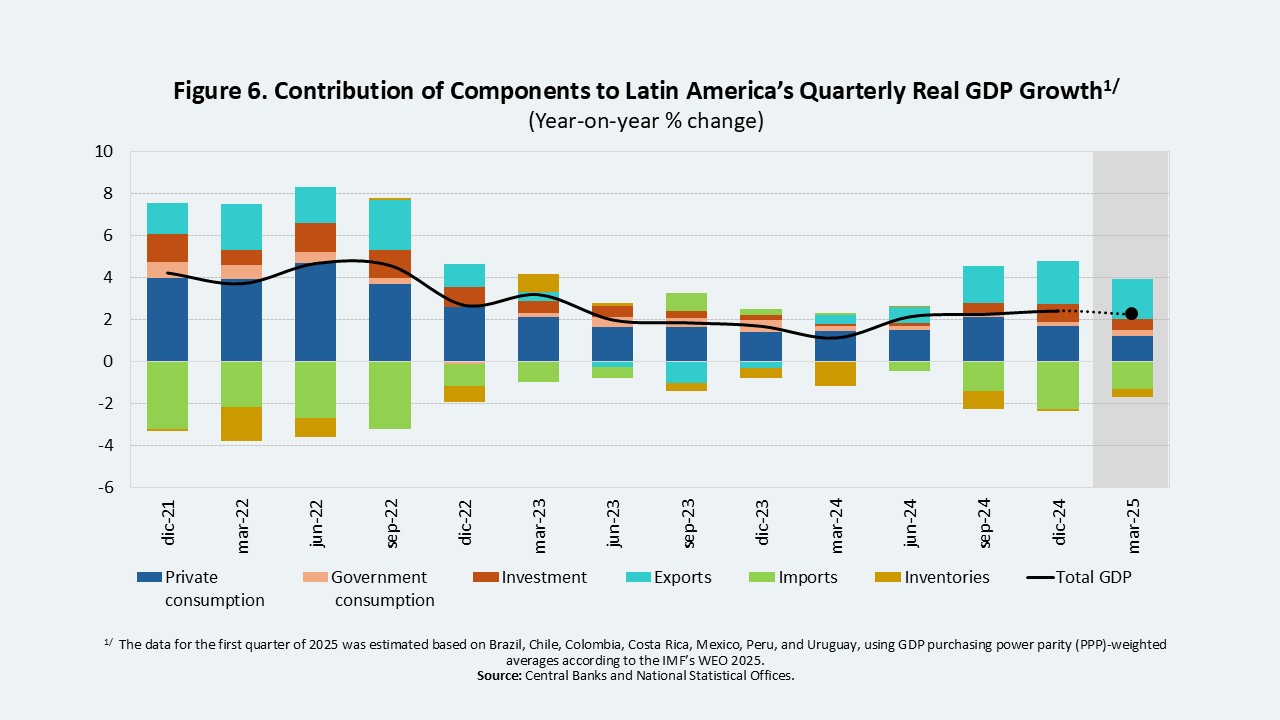

Preliminary real sector data point to lower GDP growth compared with the end of last year for most countries. This has been the result of both external and domestic factors (Figure 6). Export volumes have declined along with weaker external demand and deterioration in terms of trade, while household consumption and private investment have been affected by country-specific factors. These include domestic economic or political uncertainty, low consumer and investor confidence, high household debt, weaker public investment, and elevated interest rates.

High public debt levels and pressure on fiscal balances

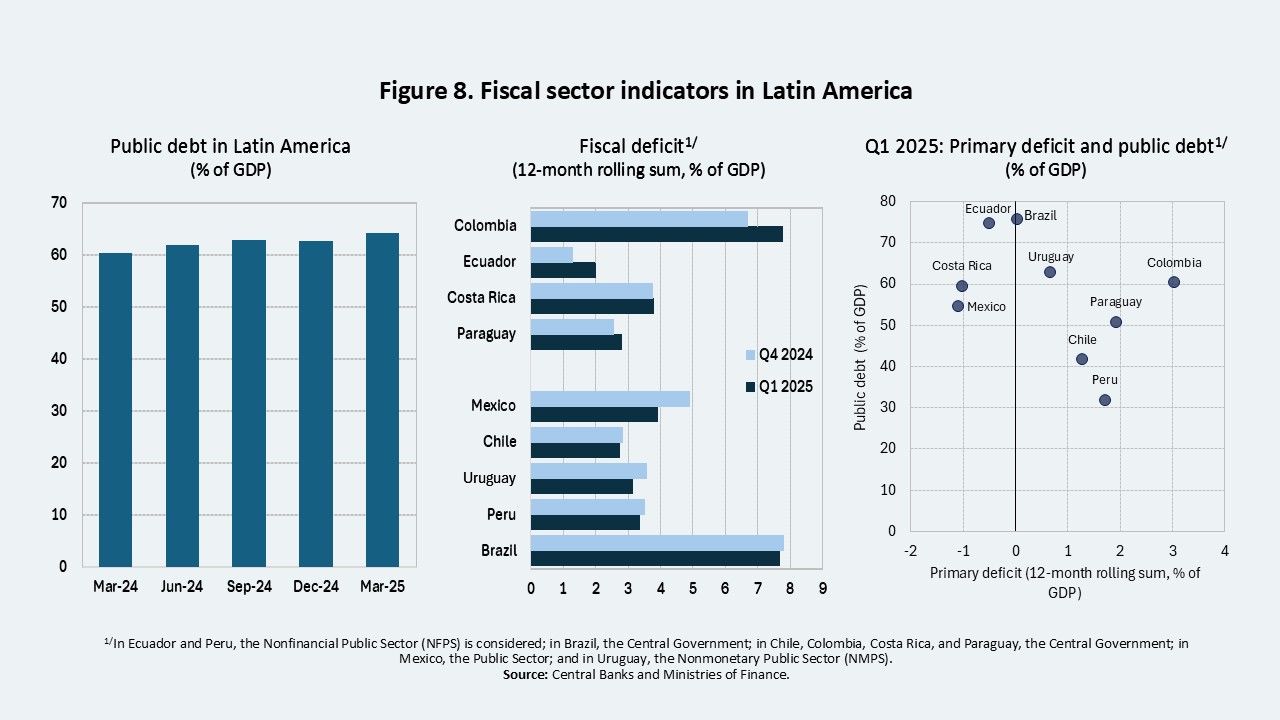

Fiscal conditions are heterogeneous across countries in the region, but concerns persist in several economies due to high and rising public debt levels as a share of GDP (Figure 8). Fiscal deficits are not low enough to stabilize or reduce this ratio. This dynamic reflects both higher primary spending and increased interest payments, the magnitude of which varies by country.

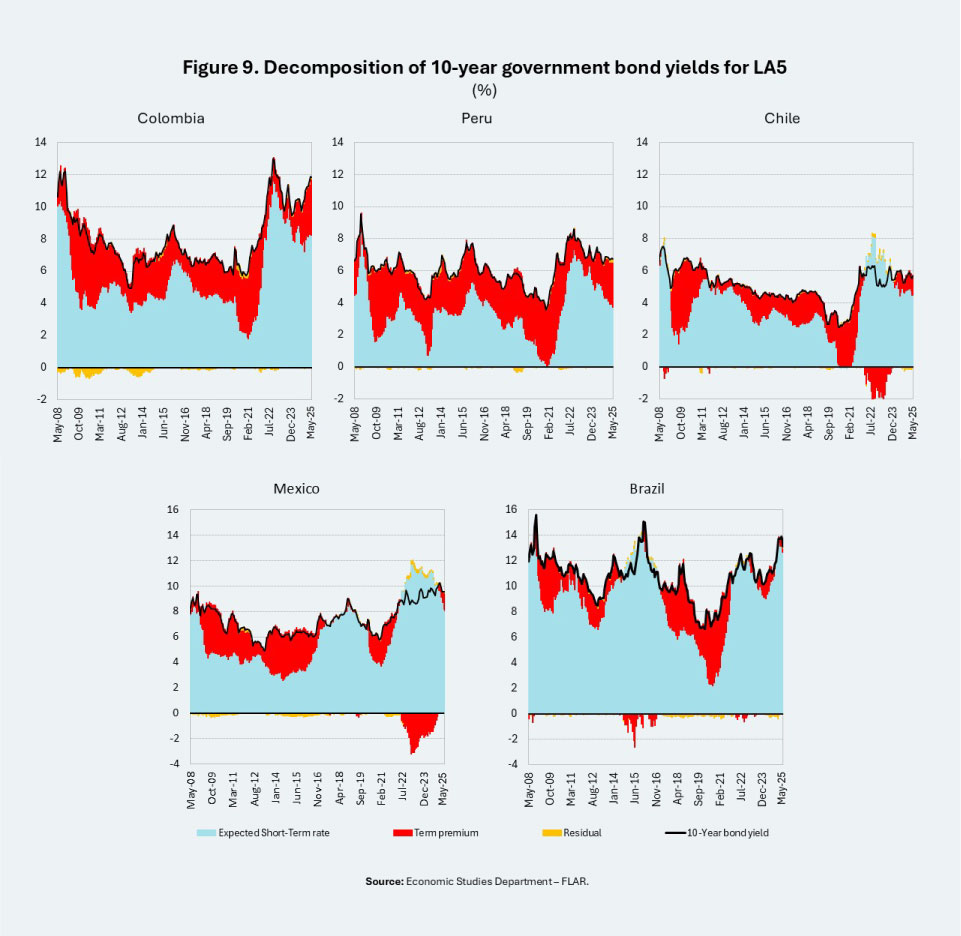

Given the relevance of sovereign financing costs and their impact on the fiscal trajectory, we assessed their structure for five regional economies based on public debt market information across the yield curve. For this purpose, we apply the ACM model (Adrian, Crump, & Moench, 2013), which decomposes long-term interest rates into two components: (i) the expected average of the short-term rate and (ii) the term premium. The first component reflects the expected path of short-term rates, and the second incorporates various risk factors, such as the fiscal deficit, the U.S. term premium, and exchange rate volatility (see Methodological Box).

The results indicate that the term premium has played an important role in long-term rates in countries such as Colombia, Peru, and Chile, and to a lesser extent in Mexico and Brazil (Figure 9). In the latter countries, short-term rates account for most of the behavior of long-term rates.

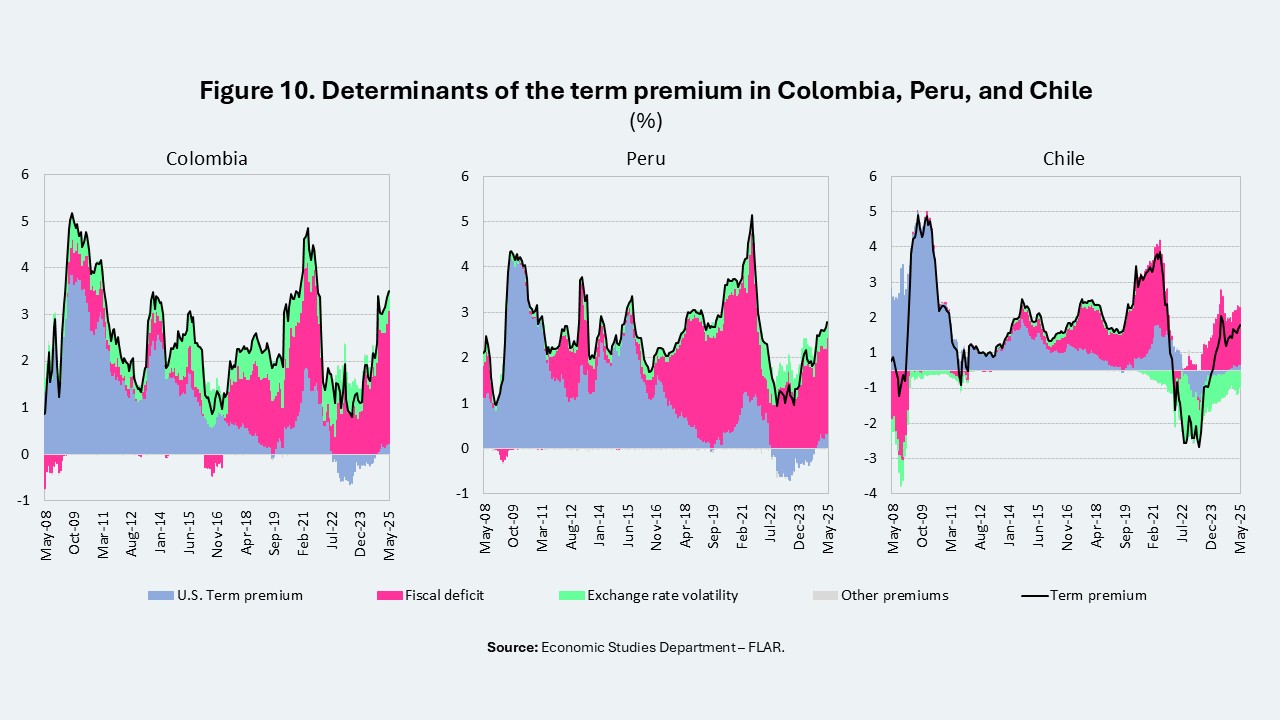

In addition, we estimated the determinants of the term premium for Colombia, Peru, and Chile (see Methodological Box). The results show that the fiscal deficit is the factor that most influences its evolution, particularly in the case of Colombia (Figure 10).

Short-term outlook and risks

For the remainder of the year, Latin America is expected to continue facing a challenging external and domestic environment, consistent with the trends observed so far.

On the external front, GDP growth in the United States and China is expected to be weaker than projected at the beginning of the year. Furthermore, inflation in the United States is expected to remain persistent, in contrast to the Euro Area and China, where weak domestic demand has contributed to its moderation. In the case of the United States, inflation expectations remain above the Federal Reserve’s target.

Given this scenario, the Fed is expected to maintain its current policy rate. This would imply that external financing costs would remain elevated for Latin America (see FlarBlog: “U.S. Economic Outlook in 2025 Q1 and Latin America’s External Financing Conditions”).

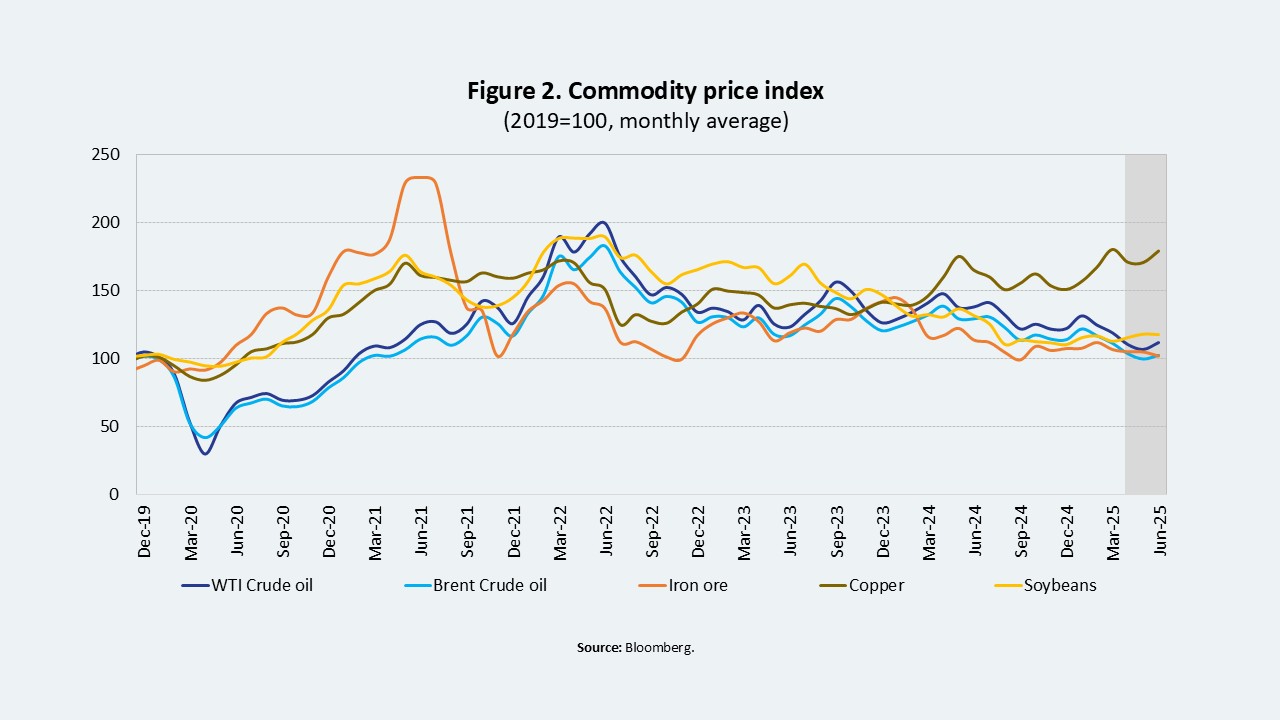

A broad-based decline in commodity prices relevant to the region’s exporters is also projected. This reflects weak global demand and, in some cases, increases in supply (e.g., oil and soybeans).

In addition to the weaker external dynamics, factors related to domestic demand are expected to contribute to slower regional growth. Aggregate demand will remain weak reflecting the elements discussed above, which will continue to constrain both consumption and private investment. In this context, the region—excluding Argentina—is projected to grow by 1.6% 2025, which is below the 2.4% recorded in 2024. However, including Argentina, regional growth would reach 2.0%.

From a fiscal perspective, the region’s aggregate deficit is expected to remain around 6% of GDP. Public debt is projected to reach 62.8% of GDP in 2025, which is above the 60% observed the previous year.

Finally, several short-term risks have been identified, notably: (i) further fiscal deterioration in some countries, with potential implications for macroeconomic stability, (ii) external shocks arising from an escalation of geopolitical and trade tensions, and (iii) a sharper slowdown in external demand, particularly from China.

Methodological Box: Term Structure of Interest Rates and Determinants of the Term Premium in the LA5 Economies

- \(\alpha_0\): Level of the yield curve, associated with the long-term component of interest rates. In other words, it reflects the level to which the yield curve converges as \(n \to \infty\)

- \(\alpha_1\): Slope factor, capturing the sensitivity of yields to short-term movements. It primarily affects the short end of the maturity spectrum.

- \(\alpha_2\): Curvature factor (first curvature), associated with the medium-term component. It allows for an adjustment of the convexity of the yield curve at intermediate maturities.

- \(\alpha_3\): Second curvature factor, associated with an additional curvature component. It allows for further adjustments to the convexity of the yield curve at very short or very long maturities, providing greater flexibility to capture complex dynamics in specific segments of the curve.

- \(\lambda_1\): Decay parameter of the first curvature, governing the speed at which the influence of the first curvature factor declines across maturities.

- \(\lambda_2\): Decay parameter of the second curvature, governing the speed at which the influence of the second curvature factor diminishes across maturities.

Bond Valuation under No-Arbitrage

Where \(\delta_0\) and \(\delta_1’\) represent the sensitivity vectors.

Furthermore, following Duffee (2002), the market price of risk \((\lambda_t)\) is defined as:

Where \(\lambda_0\) and \(\lambda_1\) represent the sensitivity vectors.

Once bond prices are obtained, the corresponding yields \(y_t^{(n)}\) can be derived through the following relationship:

\beta_t^{(n-1)’} = Cov_t \left( rx_{t+1}^{(n-1)}, v_{t+1}’ \right) \Sigma^{-1}

\)

E_t \left[ rx_{t+1}^{(n-1)} \right] = \beta_t^{(n-1)’} \left( \lambda_0 + \lambda_1 X_t \right) – \frac{1}{2} Var_t \left( rx_{t+1}^{(n-1)} \right)

\)

rx = \beta'(\lambda_0 \mathbf{1}_T’ + \lambda_1 X_-) – \frac{1}{2} \left( B^* \, {vec}(\Sigma) + \sigma^2 \mathbf{1}_N \right) \mathbf{1}_T’ + \beta’ V + E

\)

Stage I: Principal Component Analysis (PCA) is applied to obtain the vector of risk factors \(X_t\) . A \(VAR(1)\) model is then estimated to derive \(\hat{\mu}\), \(\hat{\Phi}\), \(\hat{V}\) and the variance–covariance matrix \(\hat{\Sigma} = \frac{1}{T} \hat{V} \hat{V}^{\prime}\)

Stage II: Using Ordinary Least Squares (OLS), the excess returns equation is estimated

rx = a \mathbf{1}_T^{\prime} + \beta^{\prime} \hat{V} + c X_{t} + E

\)

Stage III: The market price of risk is obtained from the following equations.

Stage IV: Ordinary Least Squares (OLS) is used to estimate the short-rate equation, yielding \(\hat{\delta}_0\) and \(\hat{\delta}_1^{\prime}\)

Stage V: Using the previously estimated coefficients, the risk-neutral yield curve and the term premia are then constructed.

- Yield Curve

- Risk-Neutral Expectations Curve

Let the time varying coefficient vector be \(\beta_t = \left[ \beta_t^{(US)},\, \beta_t^{(D)},\, \beta_t^{(Vol)} \right]^{\prime}\) and the regressors \(X_t = \left[ TP_t^{(US)},\, D_t,\, Vol_t \right]\). Here, \(TP_t^{(US)}\) denotes the U.S. term premium, \(D_t\) denotes the fiscal deficit as a percentage of GDP for a Latin American country, and \(Vol_t\) denotes the stochastic volatility of that country’s exchange rate (see FLAR Blog box, “Latin America in 2024: Macroeconomic stability in a mixed and shifting global context”). The model can be represented in Gaussian state space form.

where \(\nu_t\) denotes the state disturbance.

The errors are independent, so \(\operatorname{cov}(u_t, \nu_t) = 0\). Finally, the system is estimated using the Kalman filter.

References

Ceballos, L., Naudon, A., & Romero, D. (2015, febrero). Nominal term structure and term premia: Evidence from Chile (Documento de Trabajo N.° 752). Banco Central de Chile.

Lutz, F.A. 1940. The structure of interest rates, the quarterly journal of economics.

Dai, Q. and Singleton, K. J. (2000). Specification Analysis of A_ne Term Structure Models. Journal of Finance, 55(5):1943_1978.

Joslin, S., Singleton, K. J., and Zhu, H. (2011). A New Perspective on Gaussian Dynamic Term Structure Models. Review of Financial Studies, 24(3):926-970.

Duffee, G. (2002). Term Premia and Interest Rate Forecasts in Affine Models. Journal of Finance, 57:405-433.

Campbell, J. Y., & Shiller, R. J. (1991). Yield Spreads and Interest Rate Movements: A Bird’s Eye View. The Review of Economic Studies, 58(3), 495-514.

Adrian, T., Crump, R. K., & Moench, E. (2013). Pricing the Term Structure with Linear Regressions. Journal of Financial Economics, 110(1), 110-138.

Litterman, R. B. and Scheinkman, J. (1991). Common Factors Afecting Bond Returns. Journal of Fixed Income, 1(1):54-61.

Fama, Eugene and Bliss, Robert R., 1987, The Information in Long-Maturity Forward Rates, American Economic Review, 1987, vol. 77, issue 4, 680 – 92.

Cochrane, John, H., and Monika Piazzesi. 2005. Bond Risk Premia. American Economic Review 95 (1): 138–160.

Dybvig, P. H., and S. A. Ross. (1987). Arbitrage. In J. Eatwell, M. Milgate and P. Newman (eds.), The New Palgrave: A Dictionary of Economics. Palgrave Macmillan, pp.100-106.

Centro de Estudios Monetarios Latinoamericanos. (s.f.). Term premium estimates. Recuperado el 5 de julio de 2025, de https://www.cemla.org/DatosSelectosMacroeconomicos/Term%20premium%20estimates%20eng.html#estimates

Muth, J. F. (1961). Rational Expectations and the Theory of Price Movements. Econometrica, 29(3), 315-335.

Diebold, F. X., & Li, C. (2006). Forecasting the term structure of government bond yields. Journal of Econometrics, 130(2), 337–364.

Diebold, F. X., Rudebusch, G. D., & Aruoba, S. B. (2004). The Macroeconomy and the Yield Curve: A Dynamic Latent Factor Approach. (FRBSF Working Paper 2003 18). Federal Reserve Bank of San Francisco.

Svensson, L. E. O. (1995). Estimating Forward Interest Rates with the Extended Nelson & Siegel Method. Sveriges Riksbank Quarterly Review, 3(1):13-26.

Cook, T, and Hahn, T 1990. Interest Rate Expectations and the Slope of the Money Market Yield Curve. Federal Reserve Bank of Richmond Economic Review 76(5): 3–26.

Vasicek, O. (1977). An Equilibrium Characterization of the Term Structure. Journal of Financial Economics, 5(2):177-188.

Aguilar-Argaez, A., Diego-Fernández, M., Elizondo, R., & Roldán-Peña, J. (2020). Dinámica de la prima por plazo y sus determinantes: El caso mexicano. Documento de investigación No. 2020-18, Banco de México.