Carlos Giraldo – Chief Economist, FLAR.

Carlos Álvarez – Chief Risk Officer, FLAR.

As the world and particular regions continue to experience the effects of the pandemic and uncertainty about the containment of the pandemic persists, Latin America and the Caribbean require a robust financial safety net to support their sustained recovery over the coming years. For this purpose, having a Latin American Reserve Fund (FLAR) with regional scope to supplement the global activity of the International Monetary Fund (IMF) and other components of the global financial safety net, particularly central banks’ international reserves, is quite valuable. The new membership mechanism, approved by FLAR’s assembly by recommendation of the board of directors, points in that direction and enables an agile incorporation of the central banks of the region into the institution.

Economic recovery is underway, the number of infections and deaths have decreased throughout most of the region, and the exchange and financial markets have been relatively calm. However, the risks of macroeconomic and financial instability remain in place. If one or several of these risks materialize, recovery can suffer a setback, with higher social and economic costs than those already incurred. The risks include not only the possibility of the pandemic taking too long to be controlled but also the possibility of new episodes of volatility in capital flows, with direct and indirect effects for the entirety of Latin America. One of these episodes could arise from an unexpected change in international financing conditions associated, for instance, with changes in the Federal Reserve’s monetary policy. Alternatively, such an episode could also be the result of an eventual loss of confidence by international investors due to delays in the adoption of structural reforms in some countries or even because of the eventual effects a possible economic crisis in China.

In October 2019, the report of the working group on regional financial stability highlighted the need, convenience and urgency of forming a strong financial agreement with regional scope based on the current FLAR, which is an institution that already includes eight countries in the region (Bolivia, Colombia, Costa Rica, Ecuador, Paraguay, Peru, Uruguay and Venezuela). The effects of the pandemic have strengthened this recommendation further today.

The COVID-19 shock hit Latin America and the Caribbean at a time when these regions were already vulnerable, following five years of low economic growth. Despite the heterogeneity of prior conditions, countries in the region shared a high degree of informality and weak social security nets, while several had relatively high levels of public debt and fiscal deficits, inadequate levels of international reserves, and a limited countercyclical response capacity.

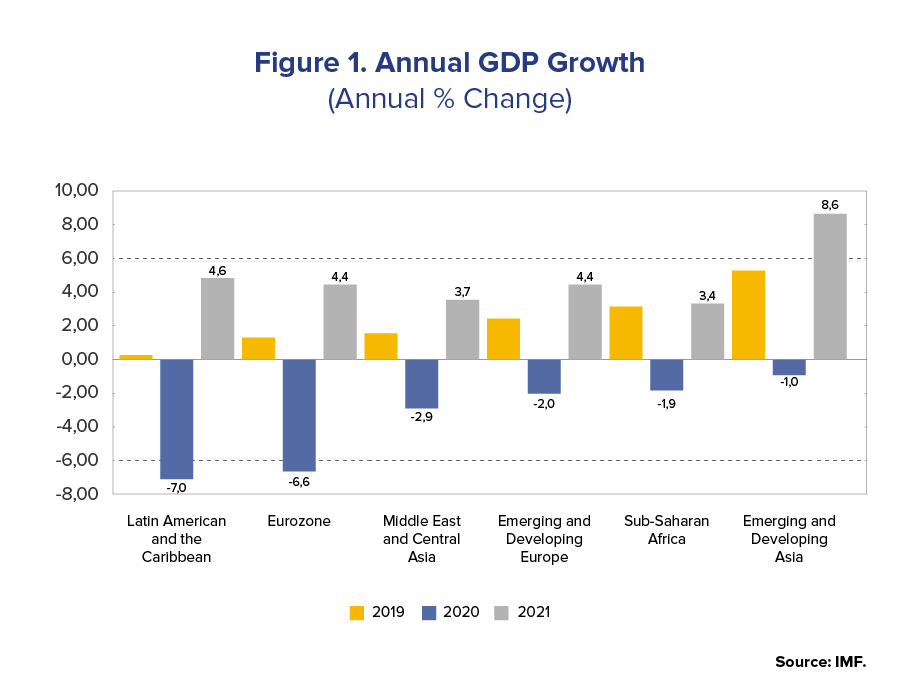

During the pandemic, Latin America and the Caribbean represented the emerging and developing regions that showed the worst economic performance (Figure 1), while several indicators for the region deteriorated. For instance, according to the IMF, while the average public debt of emerging economies stood at 64.0% in 2020, in Latin America, the average public debt reached 78.3% in the same year. Our region is not only more vulnerable than other regions in the world but also has a financial safety net with fewer components for coping with crisis episodes in its external accounts (Figure 2). The financial safety net for Latin America and the Caribbean is focused on international reserves and the IMF with respect to their national and global components, respectively. Although these two components of the net have certain advantages, they also have limitations that are offset by the existence of other components, particularly regional financing arrangements.

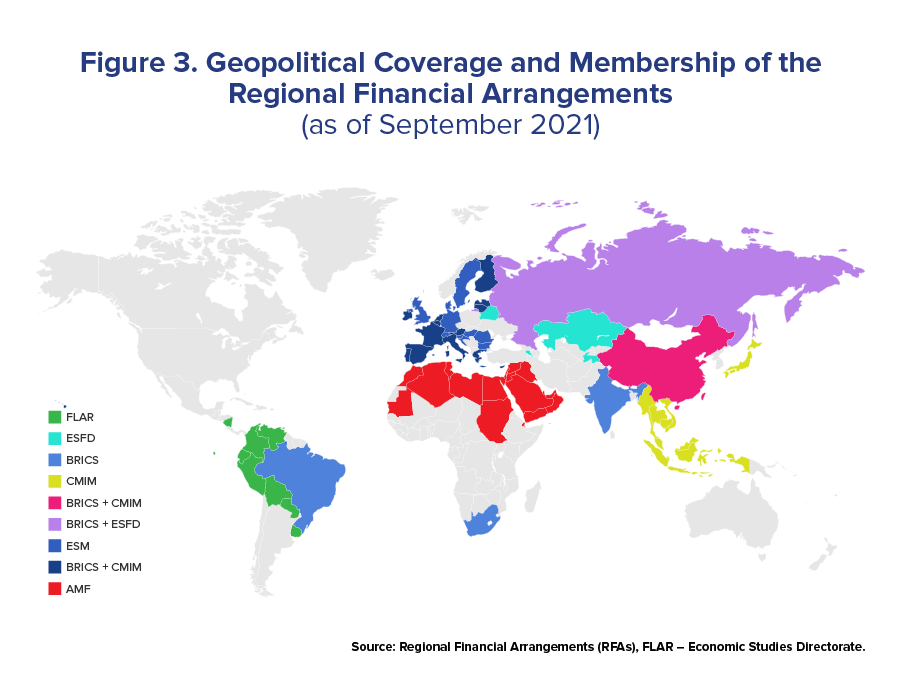

Compared to other components of the safety net, regional financing arrangements have the advantage of being able to act more quickly and are based on a greater knowledge of the region and its member countries; those arrangements do not have the stigma that the IMF has in certain countries in the region. However, FLAR’s current regional coverage limits its ability to act compared with other regional arrangements, such as the European Stability Mechanism (ESM) and the Chiang Mai Multilateralization Initiative (CMIM) (Figure 3). For this reason, an increase in FLAR membership would enhance its benefits for the macroeconomic and financial stability of the region.

Since its creation and until recently, only one process was in place for the accession of new member countries to FLAR. Considering the need to create a supplemental adhesion mechanism, FLAR’s assembly, following the recommendation of the board of directors, approved a new membership modality this past July, whereby the region’s central banks may directly join FLAR via contributions to the institution’s equity.

FLAR’s new membership mechanism is a step toward strengthening the financial safety net of Latin America and the Caribbean. In line with the recommendations of the report of the working group on regional financial stability, a strengthened FLAR could more effectively and efficiently contribute to strengthening macroeconomic and financial stability in this part of the world.

[*] The opinions and points of view expressed are the sole responsibility of the authors, and not of FLAR or its administrative bodies.

References

Report of the working group on regional financial stability (2019). Toward a FLAR with a regional outreach. October.