Authors:

Carlos Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – cgiraldo@flar.net

Iader Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – igiraldo@flar.net

Jose E. Gomez-Gonzalez, Department of Finance, Information Systems, and Economics, City University of New York – Lehman College, Bronx, NY, 10468, USA. Email: – jose.gomezgonzalez@lehman.cuny.edu

Jorge M. Uribe, Faculty of Economics and Business, Universitat Oberta de Catalunya, Barcelona, Spain, Email: – jorge.uribe@ub.edu

While the domestic bank lending channel has been well studied, its international dimension—i.e., how monetary policy is transmitted across borders via banks—has received less attention. Recent research has begun to explore how U.S. monetary policy, particularly through globally active banks, affects credit abroad. Lee et al. (2022) showed that large U.S. banks transmit monetary shocks through their international operations. Albrizio et al. (2020) reported that U.S. monetary tightening reduces cross-border lending. In contrast, Denderski and Paczos (2021) reported that in countries with a strong foreign bank presence, domestic banks adjust lending after U.S. shocks, unlike foreign-owned banks.

Global banks are recognized for their significant role in channeling capital to developing nations, though existing research primarily examines economies with a substantial U.S. banking presence. The impact of U.S. monetary shocks on countries with minimal direct exposure, such as many small, open, and financially fragile Latin American economies, remains less understood. Nevertheless, recent studies, including those by De Simone (2024) and Cao et al. (2023), indicate that U.S. policies do influence output and long-term interest rates in these regions.

In a study of five Latin American countries with limited international bank penetration, Giraldo et al. (2025) identified an international lending channel. They found that local banks adjust their credit in response to U.S. monetary shocks, with the degree of adjustment depending on their balance sheet conditions. This suggests that domestic lending can indeed be affected by external shocks, even in the absence of direct ties to U.S. banks.

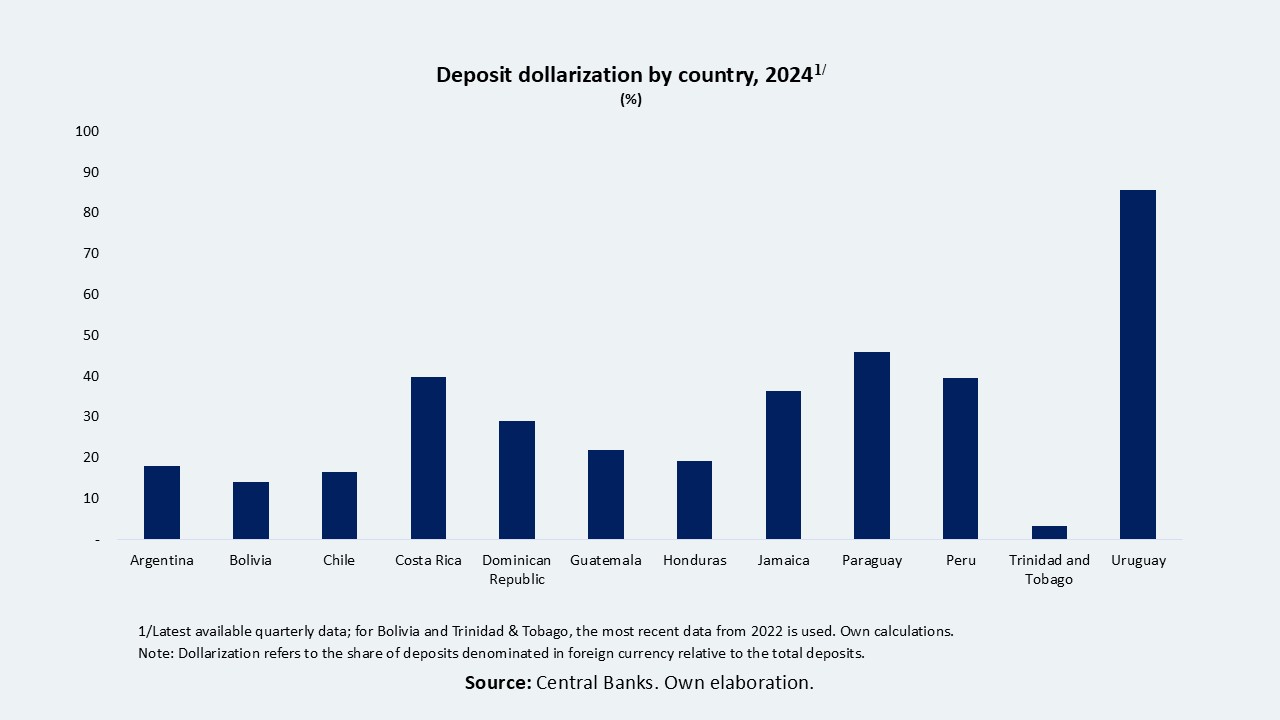

Our recent research (Working paper) expands upon this by analyzing quarterly data from 118 banks across 12 Latin American countries between 2000 and 2020. All included countries exhibit some degree of financial dollarization, offering a valuable variation to explore two key questions: Firstly, does an international lending channel operate within dollarized Latin American economies? Secondly, how does the level of dollarization influence the strength of this transmission mechanism? To our knowledge, this study is the first to investigate the impact of financial dollarization on the transmission of U.S. monetary shocks to bank lending across a diverse range of emerging markets.

The most critical findings concern the impact of U.S. monetary policy and its interplay with financial dollarization. The data reveal a statistically significant positive association between U.S. monetary policy shocks and loan growth in Latin American banks. While seemingly counterintuitive, this trend reflects broader global economic dynamics where U.S. rate hikes often coincide with global or regional economic upswings, thereby supporting credit expansion in emerging markets. Factors such as robust external demand, elevated commodity prices, or increased investor confidence can foster more favorable domestic credit conditions, even when global borrowing costs slightly increase.

However, this generalized effect conceals significant country-specific variations. The interaction between U.S. monetary policy shocks and the extent of deposit dollarization is negative and statistically significant, underscoring that the ramifications of U.S. interest rate adjustments are heavily contingent on a country’s banking system’s exposure to foreign currency liabilities. U.S. monetary tightening might not substantially impact credit markets in nations with minimal dollarization and could even align with accelerated loan growth. Conversely, in more dollarized economies, escalating U.S. interest rates tend to dampen credit expansion.

This outcome aligns with the notion that financial dollarization heightens the susceptibility of banking systems to external shocks. When banks depend on U.S. dollar funding, whether through domestic dollar deposits or international borrowing, a rise in U.S. rates inevitably increases their funding expenses. If banks lend in local currency while borrowing in dollars, a tightening of U.S. monetary policy can also create balance sheet mismatches, particularly if accompanied by exchange rate depreciation, leading banks to adopt a more conservative stance on extending new credit. The risks are especially pronounced in countries with limited capacity to absorb shocks through monetary policy or foreign exchange interventions, where dollarization curtails the central bank’s operational flexibility.

These findings highlight a significant asymmetry in how global financial conditions are transmitted to domestic credit markets. While U.S. monetary policy might yield expansionary or neutral outcomes in certain scenarios, it can exert contractionary effects in countries experiencing higher degrees of financial dollarization. This asymmetry is academically significant as it provides the first empirical evidence of an international credit channel influenced by the banking system’s dollarization level. Furthermore, this asymmetry poses practical challenges for policymakers in nations with persistently dollarized financial systems. In such environments, U.S. policy shifts can tighten domestic financial conditions even without domestic macroeconomic imbalances. Strategies to mitigate these risks include strengthening local currency funding markets, enhancing foreign exchange risk management, and reinforcing macroprudential frameworks.

References

Albrizio, S., Choi, S., Furceri, D., & Yoon, C. (2020). International bank lending channel of monetary policy. Journal of International Money and Finance, 102, 102124.

Cao, J., Dinger, V., Gómez, T., Gric, Z., Hodula, M., Jara, A., … & Terajima, Y. (2023). Monetary policy spillover to small open economies: Is the transmission different under low interest rates? Journal of Financial Stability, 65, 101116.

De Simone, F. N. (2024). The transmission of US monetary policy to small open economies. Journal of International Money and Finance, 142, 103038.

Giraldo, C., Giraldo, I., Gomez-Gonzalez, J., & Uribe, J. (2024). US monetary policy shocks and bank lending in Latin America: evidence of an international bank lending channel. Applied Economics Letters, 32(13), 1946 – 1950.

Lee, S. J., Liu, L. Q., & Stebunovs, V. (2022). Risk-taking spillovers of US monetary policy in the global market for US dollar corporate loans. Journal of Banking & Finance, 138, 105550.