Authors:

Carlos Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – cgiraldo@flar.net

Iader Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – igiraldo@flar.net

Jose E. Gomez-Gonzalez, Department of Finance, Information Systems, and Economics, City University of New York – Lehman College, Bronx, NY, 10468, USA. Email: – jose.gomezgonzalez@lehman.cuny.edu

Jorge M. Uribe, Faculty of Economics and Business, Universitat Oberta de Catalunya, Barcelona, Spain, Email: – jorge.uribe@ub.edu

The post-pandemic resurgence of inflation has renewed attention on inflation persistence and the role of central banks in maintaining credibility. While conventional explanations emphasize fiscal discipline, exchange rate regimes, or inflation targeting, these factors do not fully explain why some countries return rapidly to price stability while others experience prolonged inflationary episodes. We argue that central bank transparency—the clarity of communication regarding objectives, policy decisions, and macroeconomic forecasts—is a key determinant of inflation persistence.

Central bank transparency is a pillar of accountability and a key determinant of central bank independence (e.g., De Haan et al. 2005, 2018). Consequently, it is unsurprising that a notable trend toward increased transparency has been observed across advanced, emerging, and low-income economies over the past few decades, particularly after the Asian financial crisis (Dincer et al., 2022; Acosta, 2023). Some authors have even referred to this phenomenon as a ‘transparency revolution’ in central banking (Dincer et al., 2022). This shift includes central banks adopting practices such as setting explicit inflation targets, announcing policy actions, providing forward guidance, and making forecasts publicly available.

In our recent study, we assessed the merits of central bank transparency from a totally novel perspective. Building on the literature that highlights the benefits of transparency for managing inflation expectations and aligning private forecasts with central bank targets (e.g., Crowe, 2010; Neuenkirch, 2011; Baranowski et al., 2021), we employ duration analysis, both parametric and non-parametric, and demonstrate that more transparent central banks are more effective in shortening episodes of ‘very high inflation’ compared to less transparent central banks.

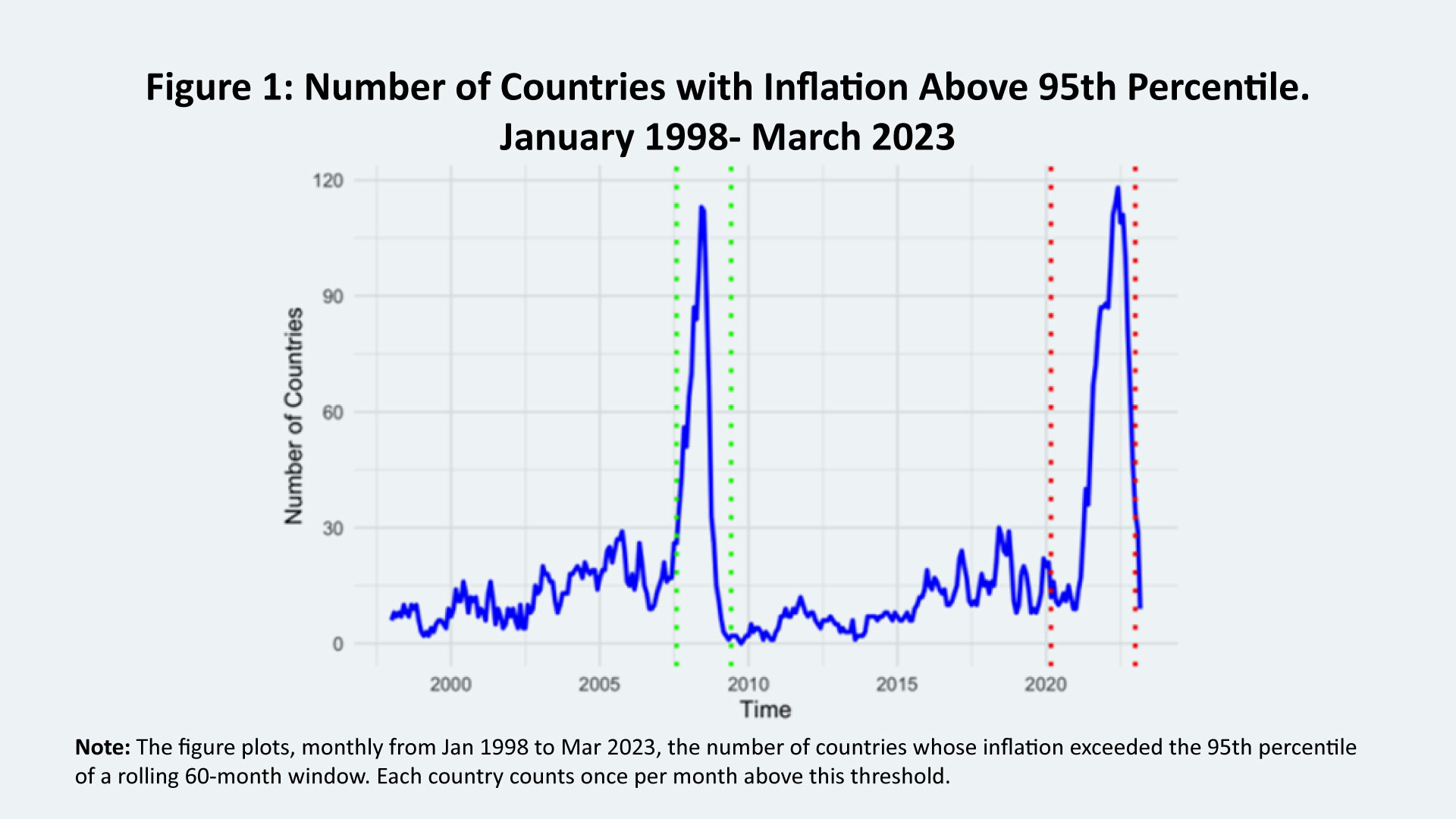

We define ‘very high inflation’ as periods where inflation surpasses a threshold relative to a country’s recent inflationary history. Specifically, year-over-year monthly inflation rates above the 95th percentile of YoY monthly inflation rates recorded over the previous five years are considered here as ‘very high’. This relative and data-driven approach is crucial for capturing the elusive and context-dependent nature of ‘high inflation,’ which naturally varies significantly across countries and over time, making fixed, absolute thresholds less effective. Our measure of very high inflation is distinct from hyperinflation, as it is inherently country-specific and unrelated to cross-country inflation levels. By dynamically adjusting to each economy’s recent experience, this definition allows for a more precise identification of episodes where central bank transparency plays a critical role in managing expectations and shortening inflationary spells. Whenever an economy is experiencing an episode of inflation above the 95th percentile of inflation rates in its recent history, we say it is experiencing very high inflation (Figure 1).

Our principal finding is that greater transparency is associated with significantly shorter episodes of high inflation. This relationship remains robust after controlling for traditional features of modern monetary frameworks, including inflation targeting, fiscal rules, financial integration, and different exchange rate regimes. These results suggest that credibility—strengthened through transparent communication—serves as a powerful complement to formal institutional arrangements in reducing inflation persistence.

The findings complement conventional wisdom in two key ways. First, once transparency is taken into account, fiscal discipline, economic openness, and exchange rate regimes appear to have limited effectiveness in reducing inflation persistence. Second, adopting an inflation-targeting framework alone does not guarantee shorter inflation episodes; it must be complemented by credibility rooted in transparency, which, for this particular aspect of inflation—its persistence in very high states—plays an important role complementing traditional formal policy design.

The implication for policymakers is clear and compelling: improving transparency by clearly communicating objectives, providing accurate forecasts, and offering thorough explanations of policies is essential to effectively reducing inflation persistence. This transparent communication not only builds public trust and stabilizes inflation expectations, but it also plays a crucial role in enabling a quicker recovery from inflationary shocks. In contrast, a lack of transparency tends to prolong and complicate economic adjustments.

References

Acosta, M. (2023). A new measure of central bank transparency and implications for the effectiveness of monetary policy. International Journal of Central Banking, 19(3), 49-97.

Baranowski, P., Bennani, H., & Doryń, W. (2021). Do the ECB’s introductory statements help predict monetary policy? Evidence from a tone analysis. European Journal of Political Economy, 66, 101964.

Crowe, C. (2010). Testing the transparency benefits of inflation targeting: Evidence from private sector forecasts. Journal of Monetary Economics, 57(2), 226-232.

De Haan, J., Bodea, C., Hicks, R., & Eijffinger, S. C. (2018). Central bank independence before and after the crisis. Comparative Economic Studies, 60(2), 183-202.

Dincer, N., Eichengreen, B., & Geraats, P. (2022). Trends in monetary policy transparency: Further updates. International Journal of Central Banking, 18(1), 331-348.

Neuenkirch, M. (2012). Managing financial market expectations: the role of central bank transparency and central bank communication. European Journal of Political Economy, 28(1), 1-13.