Authors1:

Christian Alcarraz, FLAR, Bogotá, Colombia. – calcarraz@flar.net

Daniel García, FLAR, Bogotá, Colombia. – dgarcia@flar.net

Carlos Giraldo, FLAR, Bogotá, Colombia. – cgiraldo@flar.net

Andrea Villarreal, FLAR, Bogotá, Colombia. – avillarreal@flar.net

Liz Villegas , FLAR, Bogotá, Colombia. – lvillegas@flar.net

In the past three months, Latin America has faced reduced external and domestic financing constraints, supported by lower interest rates driven by easing inflation in most countries. This context has enabled us to revise the region’s annual growth projection to 2.1% for 2024. However, inflation remains above target in several countries, and public debt continues to rise as a percentage of GDP, underscoring the need for greater fiscal consolidation efforts. These efforts, however, will need to be tailored to the diverse economic conditions across the region.

Reduced restrictions on access to external financing, combined with the continued strong performance of remittances, have helped mitigate the impact of deteriorating terms of trade on the region’s external accounts (see Graph 1). This deterioration has been driven by declining prices for key commodities, including oil, copper, and soybeans. In this context, central banks have accumulated international reserves over the past three months, achieving a quarterly increase of 5% in the average reserve balance.

Graph 1. External sector indicators

Latam includes Bolivia, Colombia, Costa Rica, Ecuador, Mexico, Peru, Paraguay and Uruguay. Aggregated by GDP in USD PPP. Chile is excluded because it is a large net remittances sender to the region. Main origins: Bol = Spain, Chile, USA and Argentina; Col = USA, Spain and Chile; Mex = USA; Par = Argentina, Spain and Brazil; CR = USA; Ecu = USA and Spain; Per = USA, Spain and Chile; and Uru: Argentina, Spain and USA.

Source: Central banks and own calculations and estimations.

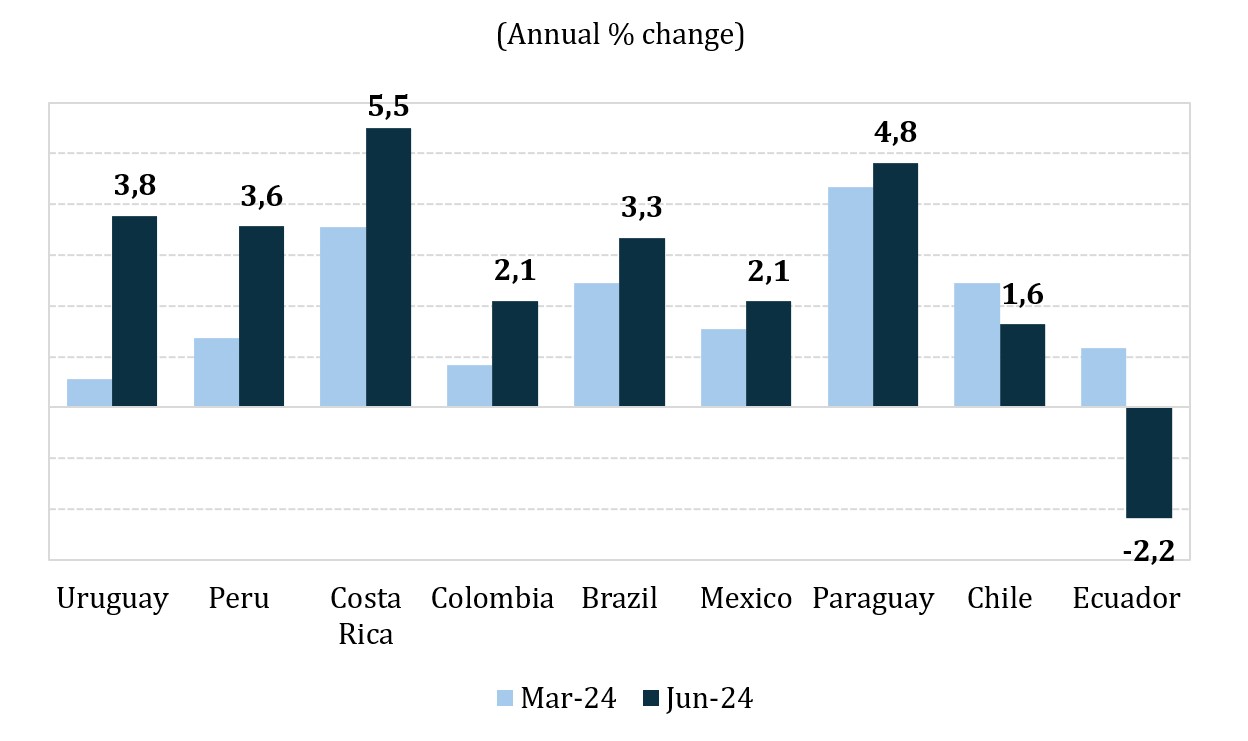

Graph 2. Quarterly real GDP growth

Data for the second quarter of 2024 is an estimate considering Brazil, Chile, Colombia, Costa Rica, Mexico, Peru, Paraguay and Uruguay. Aggregated by GDP in USD PPP.

Source: Own calculations based on information from central banks.

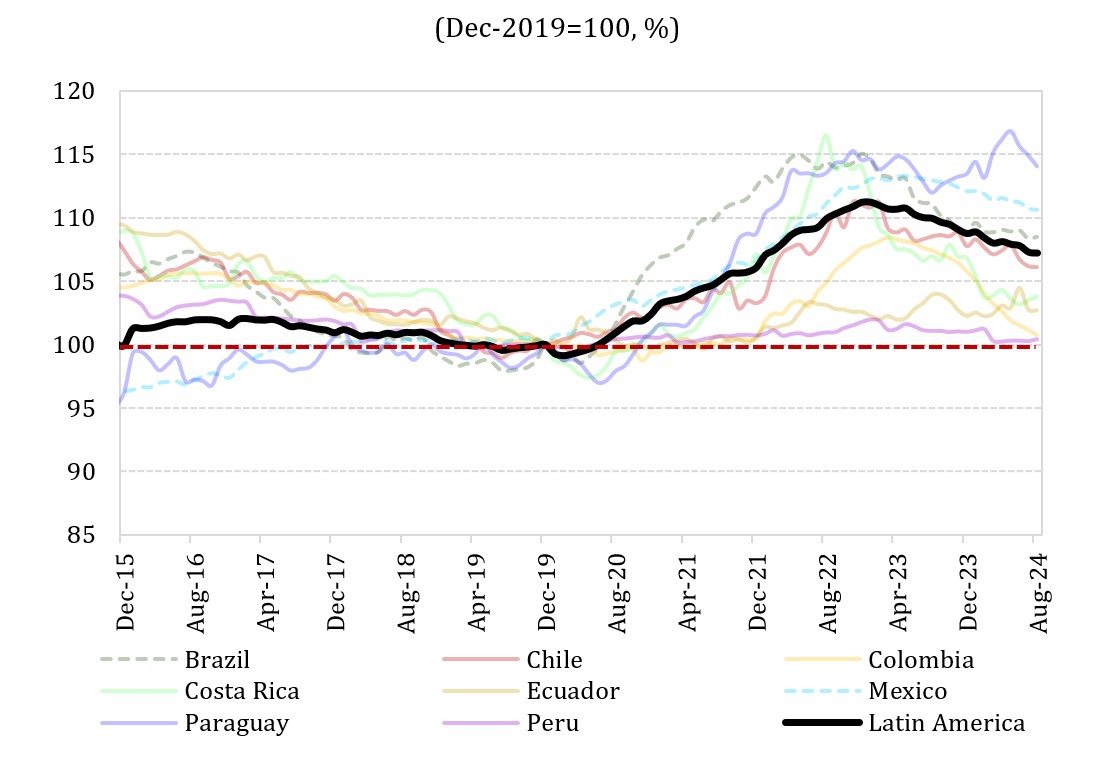

Graph 3. Ratio of the price of goods to the price of services in Latin America

Latin America includes Brazil, Chile, Colombia, Costa Rica, Ecuador, Mexico, Paraguay and Peru. Aggregated by GDP in USD PPP.

Source: Own calculations based on information from central banks.

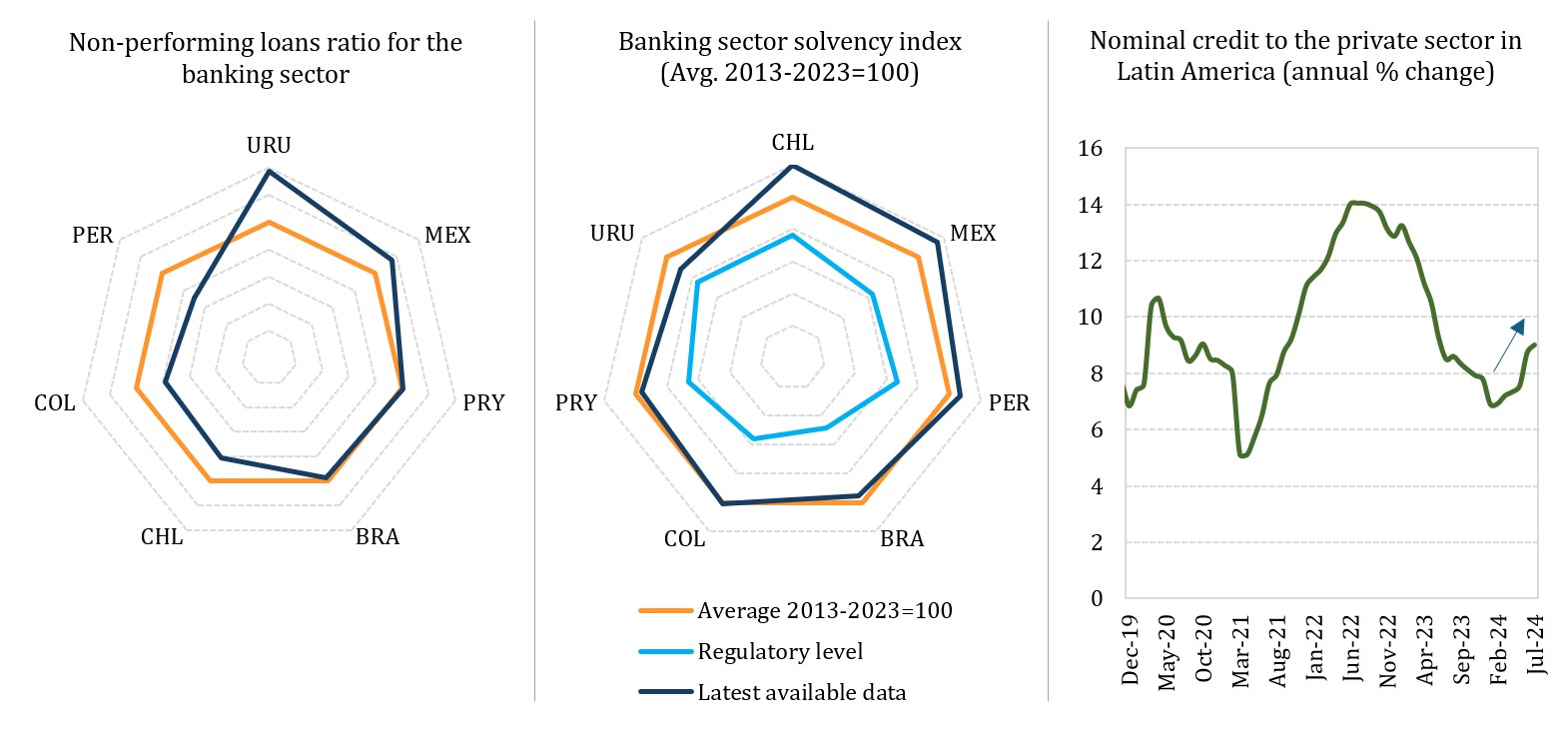

Graph 4. Financial sector indicators

Latin America Includes Bolivia, Brazil, Chile, Colombia, Costa Rica, Ecuador, Mexico, Peru, Paraguay and Uruguay. Aggregated by GDP in USD PPP.

Source: Own calculations based on information from central banks.

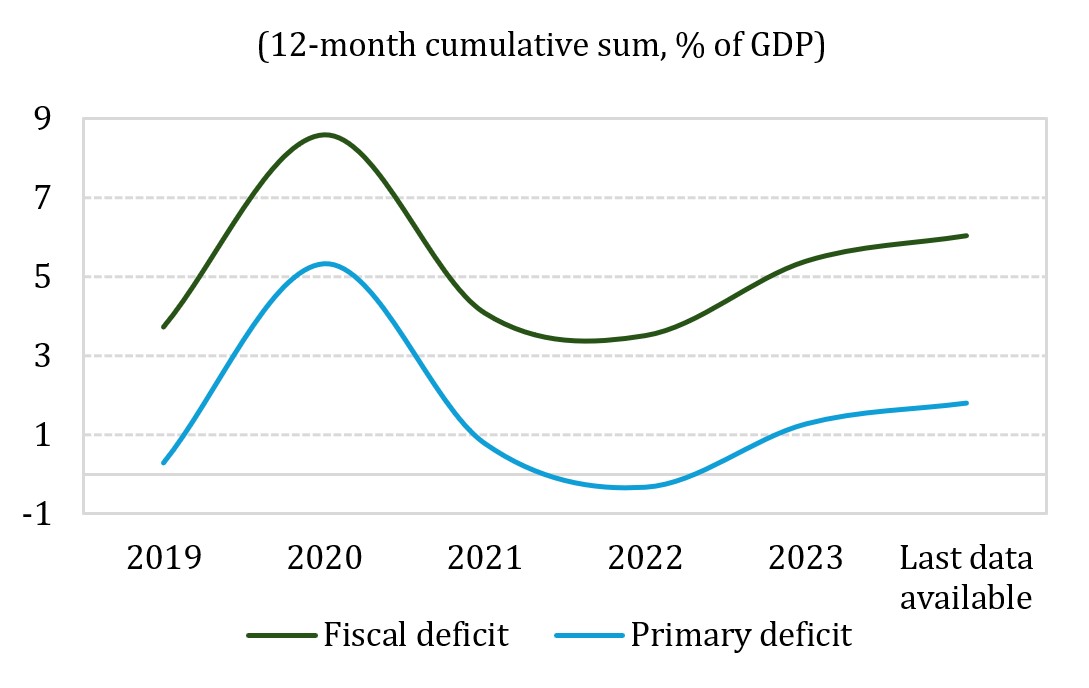

Graph 5. Primary and fiscal deficit in Latin America

Includes Bolivia, Brazil, Chile, Colombia, Costa Rica, Ecuador, Mexico, Peru, Paraguay and Uruguay. Aggregated by GDP in USD PPP.

Source: Own calculations based on information from ministries of finance.

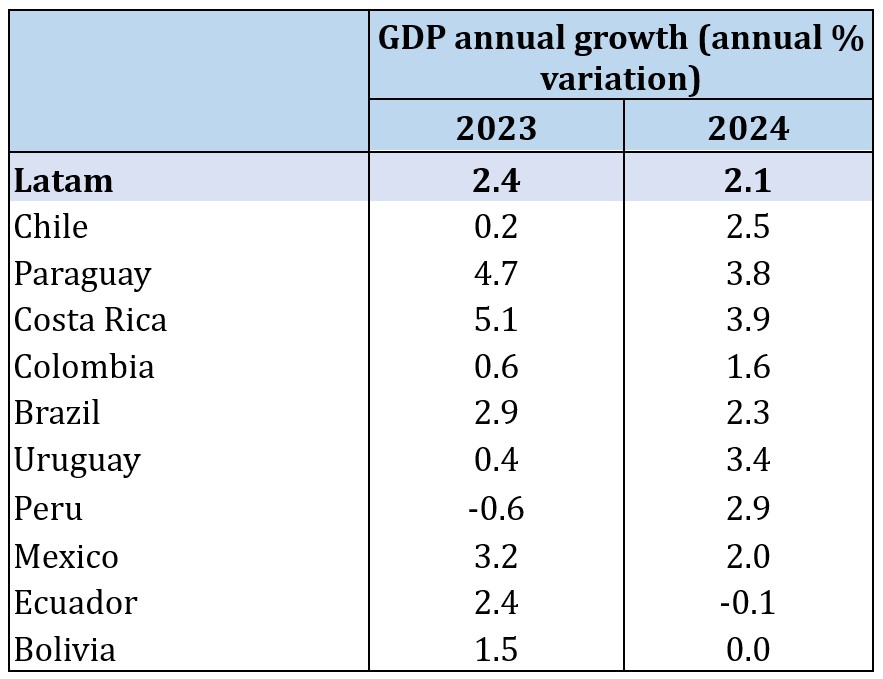

In the short term, the region’s GDP is projected to grow by 2.1% in 2024 (see Table 1), a 0.1 percentage point increase from our June forecast. Inflation is expected to continue its downward trend through the end of 2024 in most countries, although it will likely remain above target in many inflation-targeting economies.

On the external front, current account deficits as a percentage of GDP are anticipated to be below the decade’s average in most countries, suggesting a reduced vulnerability to sudden stops or reversals in capital flows.

Table 1. Estimates of real GDP growth in Latin America

Source: Aggregated by GDP in USD PPP. Calculations: Department of Economic Studies – FLAR.

Key risks to these projections include the possibility that inflation’s convergence toward target levels could stall or even reverse due to persistent price pressures on services and wages in several economies. This risk is further amplified by the recent upward trend in fiscal deficits. In such a scenario, central banks may need to raise policy rates or maintain them at elevated levels for an extended period to anchor inflation expectations. Additional inflationary pressures could arise from factors related to geoeconomic fragmentation or climate-related effects.

The combination of elevated inflation, interest rates, and fiscal deficits could activate several risk channels. Notably, there is the possibility of a large-scale sell-off of local public bonds held by foreign creditors. Additionally, the banking sector may face losses in the value of its investments in local public bonds, which represent over 10% of total assets in most countries.

In summary, a macroeconomic policy mix that promotes fiscal consolidation, curbs inflationary pressures, and continues to ease both domestic and external financial conditions is essential for maintaining macroeconomic and financial stability.