Authors:

Carlos Giraldo, Latin American Reserve Fund, Bogotá, Colombia. – cgiraldo@flar.net

Iader Giraldo, Latin American Reserve Fund, Bogotá, Colombia. – igiraldo@flar.net

Cristian Huertas, National University of Colombia. – cfhuertasco@unal.edu.co

Juan Camilo Sánchez, National Directorate of Taxes and Customs – DIAN. – jsanchezd1@dian.gov.co

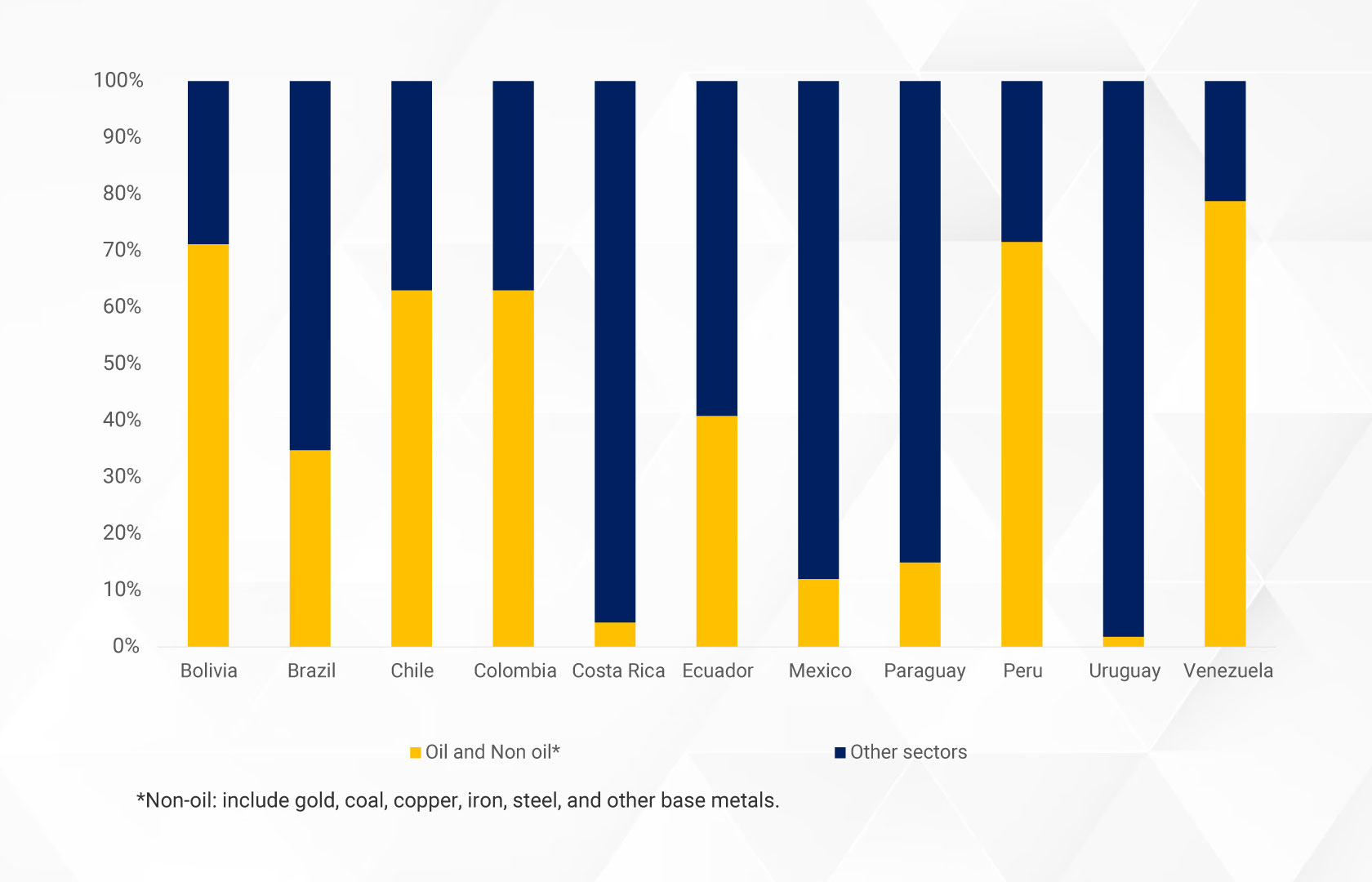

Figure 1: Exports by added sectors 2023 (% of total exports)

In this context, companies engaged in commodity production must navigate a landscape characterized by price volatility and uncertainty, compelling them to adopt hedging practices as a means to stabilize their cash flows and protect against adverse market conditions. This strategy has become increasingly vital following the sharp decline in commodity prices since 2014 Fricke and Süßmuth (2014). Furthermore, these hedging mechanisms are essential for ensuring that the revenue streams remain robust during periods of economic downturn, which have compounded the challenges faced by governments reliant on these sectors for tax income and public expenditure, particularly given the increased susceptibility of Latin American economies to external shocks due to their significant dependency on commodity exports (Campodónico et al., 2017; and Fricke and Süßmuth, 2014).

The significance of the extractive sector and its stability poses a substantial challenge for Latin American economies, as companies within this sector consistently face various risks, including commodity price risk, financial constraints risk, and exchange rate risk. Therefore, it is highly relevant to understand whether companies in the Latin American extractive sector employ hedging strategies to mitigate the different risks associated with their productive activities. With this backdrop, our recent paper, “Determinants of Financial Hedging Strategies among Commodity Producer Firms in Latin America,” aims analyze the key drivers behind the adoption of financial hedging strategies among Latin American commodity producers.

The paper identifies several factors that influence Latin American firms’ decisions to hedge. These determinants align with previous studies on developed countries but introduce new dimensions unique to emerging markets.

Firm Size and Leverage: Larger firms with significant debt are more likely to hedge. This is attributed to the fact that larger entities possess the resources and scale necessary to absorb the costs associated with implementing hedging strategies. Furthermore, firms with higher leverage ratios are found to hedge more extensively to manage the risks linked to their financial obligations, especially in commodity markets.

Commodity Prices and Volatility: As expected, the level of commodity prices and their volatility play a significant role in firms’ decisions to hedge. Firms frequently aim to secure favorable prices during periods of volatility or when prices are elevated to safeguard against potential downturns. This contrasts with some studies in developed markets, where price volatility sometimes does not play as significant a role.

Exchange Rate Exposure: Many countries in Latin America face exchange rate volatility. Firms that acquire debt in U.S. dollars are more likely to use hedging instruments to ensure a stable income.

Ownership Structure: State ownership also plays a role. State-owned companies, especially in the oil sector, are more likely to engage in hedging. Governments, which depend on revenue from these companies, often push for hedging strategies to stabilize public finances.

Access to International Markets: Credit ratings emerge as a critical determinant for Latin American firms. Rated firms have better access to international markets, which enables them to utilize derivatives and other hedging instruments more effectively. In contrast, unrated firms, often facing limited market access, struggle to implement the same level of financial protection. This is a stark difference from firms in developed countries, where access to derivatives is more readily available.

Degree of Multinationalism: Firms with a broader international presence tend to hedge more frequently. Companies operating across multiple countries benefit from wider access to financial instruments and greater financial flexibility, allowing them to pursue hedging strategies that align with their global operations.

An additional contribution of the study is the separation of the oil and non-oil sectors in the analysis. Both sectors show some commonalities in hedging behavior, but there are also notable differences:

Oil Firms: Oil companies, especially those that are state-owned, hedge more frequently. Their size, leverage, and dependence on international markets make them more vulnerable to price shocks, which drives their use of hedging strategies. The study finds that oil firms also hedge more aggressively during periods of high price volatility, confirming that price risk plays a more substantial role in their financial decisions.

Non-Oil Firms: Non-oil commodity firms also hedge, but their capital expenditures and international exposure influence their strategies. These firms are typically smaller and less likely to be state-owned, which reduces the influence of ownership structure on their hedging decisions. Interestingly, while oil firms hedge more in response to price volatility, non-oil firms hedge primarily to manage uncertainties surrounding large capital-intensive projects.

This recent research provides valuable insights into the factors influencing financial hedging in Latin America’s commodity-producing sector. It emphasizes the significance of foreign debt, ownership structure, and access to international markets in shaping hedging strategies. This paper represents an important step in understanding how Latin American firms manage the challenges of a volatile global market and offers practical insights for policymakers and business leaders aiming to improve risk management practices. Given the ongoing fluctuations in commodity prices and the vulnerability of Latin American economies to external shocks, hedging is likely to remain a crucial strategy for firms seeking financial stability.

References

Ayuk, E. T., and Klege, R. A. (2017). Extractive resources, global volatility and Africa’s growth prospects. Journal of Sustainable Development Law and Policy (The), 8(1), 259-287.

Campodónico, H., Carbonnier, G., and Vázquez, S. T. (2017). Alternative development narratives, policies and outcomes in the Andean Region. In Alternative Pathways to Sustainable Development: Lessons from Latin America (pp. 1-15). Brill Nijhoff.

Fricke, H., and Süssmuth, B. (2014). Growth and volatility of tax revenues in Latin America. World Development, 54, 114-138.