Authors:

Carlos Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – cgiraldo@flar.net

Iader Giraldo, Latin American Reserve Fund, Bogotá, Colombia. Email: – igiraldo@flar.net

Jose E. Gomez-Gonzalez, Department of Finance, Information Systems, and Economics, City University of New York – Lehman College, Bronx, NY, 10468, USA. Email: – jose.gomezgonzalez@lehman.cuny.edu

Jorge M. Uribe, Faculty of Economics and Business, Universitat Oberta de Catalunya, Barcelona, Spain, Email: – jorge.uribe@ub.edu

Our recent FLAR working paper, “Government Debt Expansion and Bank Capitalization: The Conditioning Role of Institutional Quality,” explores how banks’ capital ratios respond to government debt-to-GDP shocks and how this response varies with regulatory quality. Bank capital is a central element of financial stability, and its cyclical behavior has received considerable attention in the macroprudential literature. While earlier studies show that adjustments in capital buffers depend strongly on institutional strength and regulatory design, a parallel body of research examines the interplay between fiscal conditions and banking stability. Yet far fewer contributions investigate how public debt directly affects banks’ solvency through changes in their capital buffers, and even fewer consider how regulatory quality moderates this adjustment. Consequently, a key dimension of the sovereign–bank nexus remains insufficiently understood.

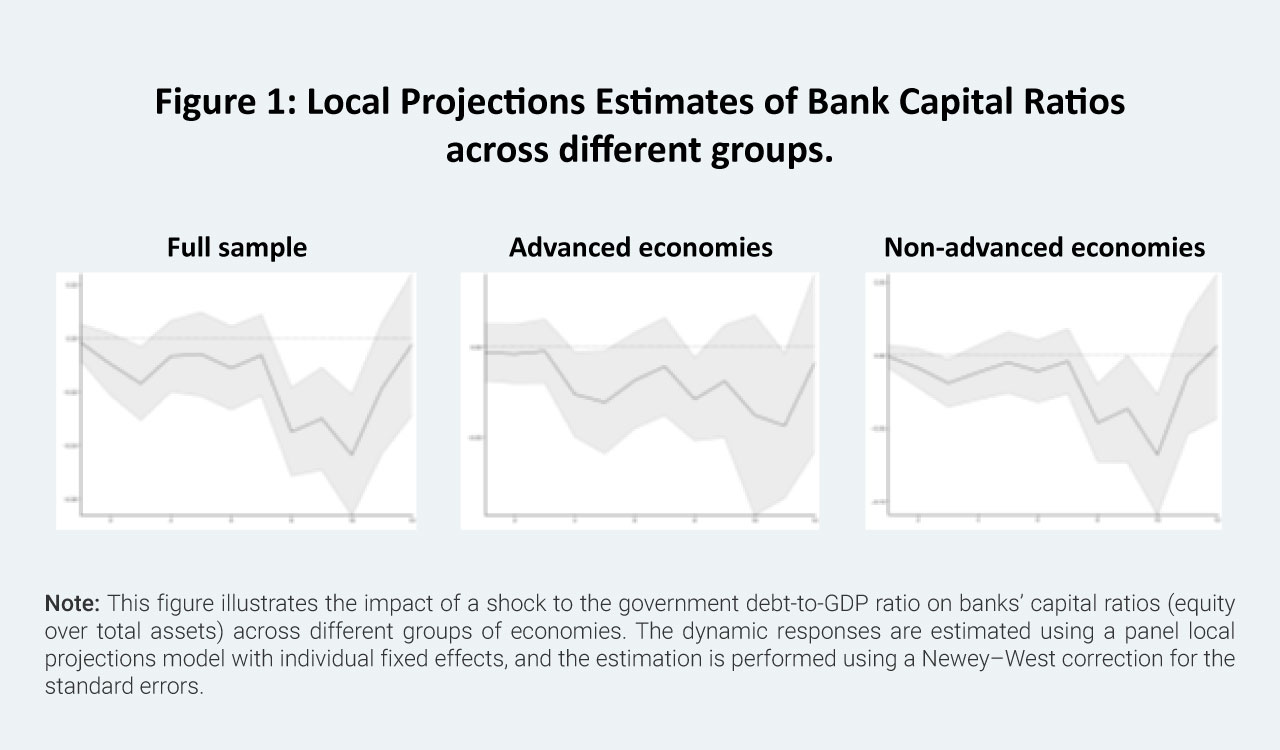

Our study addresses this gap by examining how banks adjust their capital ratios in response to increases in public debt and how these adjustments vary across institutional environments. Using a panel of banks from advanced and non-advanced economies within a local projections framework, we first document the average response of banks’ capital-to-assets ratios to debt-to-GDP shocks. We find that higher public debt reduces bank capital across both country groups—a pattern that aligns with channels highlighted in the sovereign–bank literature, including valuation losses on sovereign holdings, deteriorations in borrower quality, and tighter financial conditions that weaken banks’ balance sheets (Figure 1).

Our main findings reveal a pronounced state dependence in how capital adjusts to fiscal shocks. In countries with low regulatory quality, public debt increases lead to a rise in capital ratios in the medium term, as banks rebuild buffers gradually amid less effective supervision and delayed loss recognition. However, in economies with weaker institutions, this increase proves temporary and gives way to a decline, allowing sovereign stress to erode capital more sharply later. By contrast, in countries with high regulatory quality, banks reduce capital promptly after a debt shock, consistent with earlier loss recognition and closer supervisory oversight. In advanced economies, this early decline is followed by a gradual recovery.

These patterns directly relate to the sovereign–bank nexus literature, indicating that regulatory strength determines not only the magnitude of transmission from fiscal stress to banks but also the timing and direction of adjustment. They also extend the capital buffer literature by identifying fiscal conditions, specifically, increases in public debt, as underexplored but important determinants of capital dynamics. In doing so, our paper bridges these two strands of research, demonstrating that banks’ solvency responses to fiscal shocks depend crucially on institutional quality and that sovereign distress affects banks through channels not fully captured by risk-weighted capital measures.

These findings highlight the pivotal role of institutional quality in influencing the transmission of fiscal shocks to the banking sector. Strong supervisory systems allow losses associated with sovereign exposures to be recognized promptly, reducing the likelihood that vulnerabilities accumulate unchecked. In weaker regulatory environments, the initial behavior of capital may provide an incomplete picture of bank resilience, as delayed loss recognition and concentrated sovereign exposures can mask underlying fragilities for an extended period.

The results also highlight the importance of the capital measure used in policy analysis and surveillance. Because domestic sovereign securities often carry a zero-risk weight, risk-weighted capital ratios can remain largely unchanged during episodes of fiscal deterioration. In contrast, the capital-to-assets ratio responds directly to valuation changes and balance sheet adjustments, and therefore offers a more transparent indicator of the pressures generated by government debt. It also avoids the comparability issues that arise from differences in supervisory discretion and internal modeling practices across countries.

Differences between advanced and non-advanced economies point to additional policy considerations. Banks in emerging and developing economies typically hold a larger share of domestic sovereign debt and operate in institutional environments where supervisory capacity is more limited. Credible fiscal frameworks and improvements in oversight are therefore crucial for containing potential feedback between sovereign and banking sector risks. In advanced economies, where supervisory intervention is timelier, ensuring that banks rebuild capital once conditions improve is important for avoiding prolonged balance-sheet constraints and supporting the recovery of credit supply.

These findings underscore the critical importance of institutional quality in shaping the transmission of fiscal shocks to the banking sector. Policymakers must recognize that robust supervisory frameworks are essential for ensuring prompt loss recognition and preventing the accumulation of unchecked vulnerabilities, particularly given the limitations of risk-weighted capital measures in capturing sovereign exposure risks. For non-advanced economies, this implies a pressing need to strengthen supervisory capacity and establish credible fiscal frameworks to mitigate feedback loops between sovereign and banking sector risks. In advanced economies, while early intervention is possible, sustained attention is necessary to ensure that banks rebuild their capital effectively, thereby supporting credit supply and overall economic recovery. Addressing these interdependencies through targeted regulatory and fiscal policies is paramount for fostering financial stability across diverse economic landscapes.